Key Takeaways

- Debt collection management software helps B2B finance teams collect overdue invoices systematically, not aggressively, and without involving a collection agency.

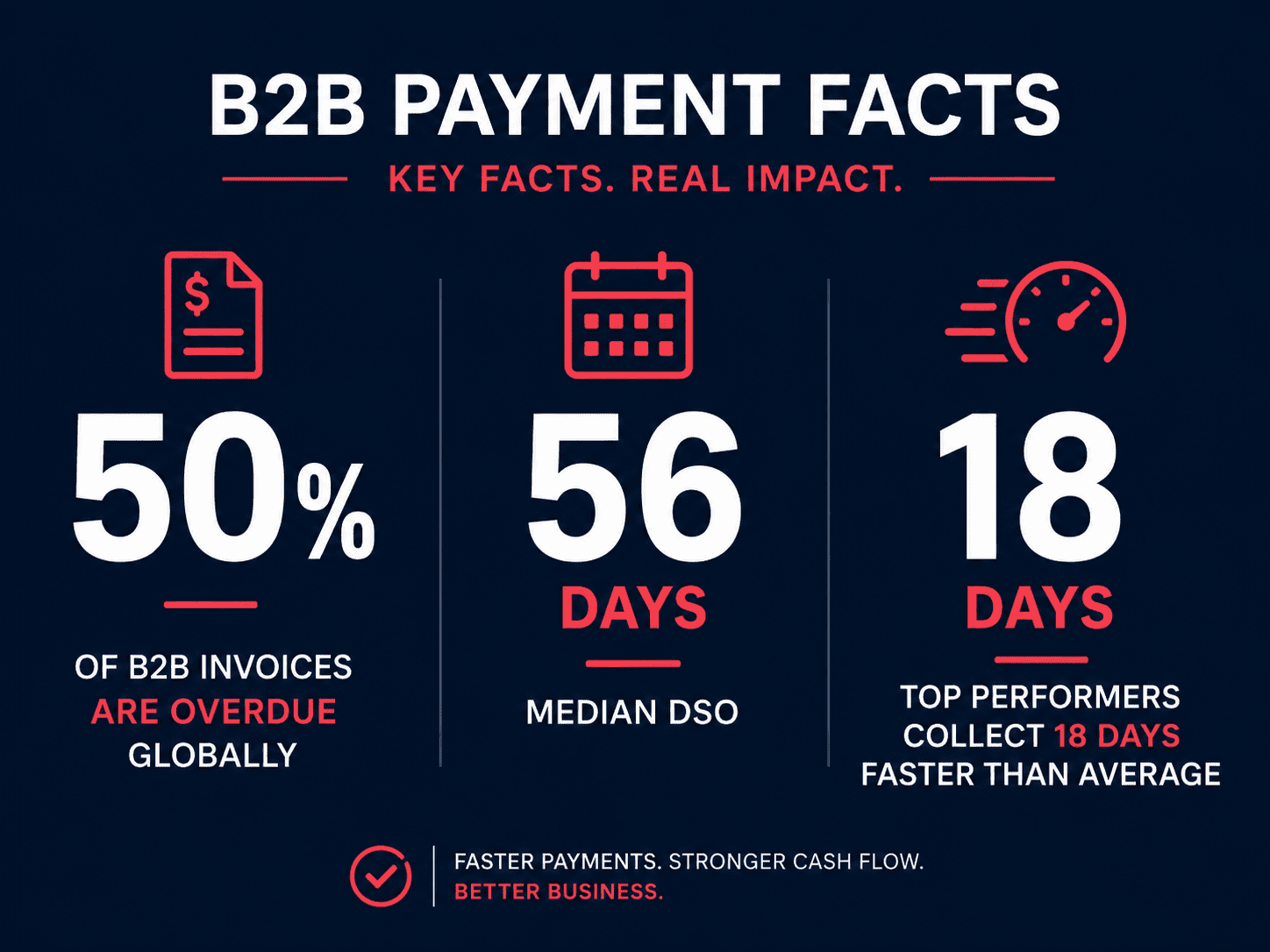

- Half of all B2B invoices globally are currently overdue, with a median DSO of 56 days, and that is a working capital problem software directly solves.

- AI-powered collections software predicts payment risk up to 21 days before an invoice goes overdue, enabling proactive action instead of reactive chasing.

- For Indian B2B companies, integrations with Tally, BUSY, WhatsApp, and UPI make this category uniquely relevant given local ERP and payment ecosystems.

- OptimAR by Ainfinite AI is an AI-powered collections copilot purpose-built for Indian and global mid-market B2B finance teams.

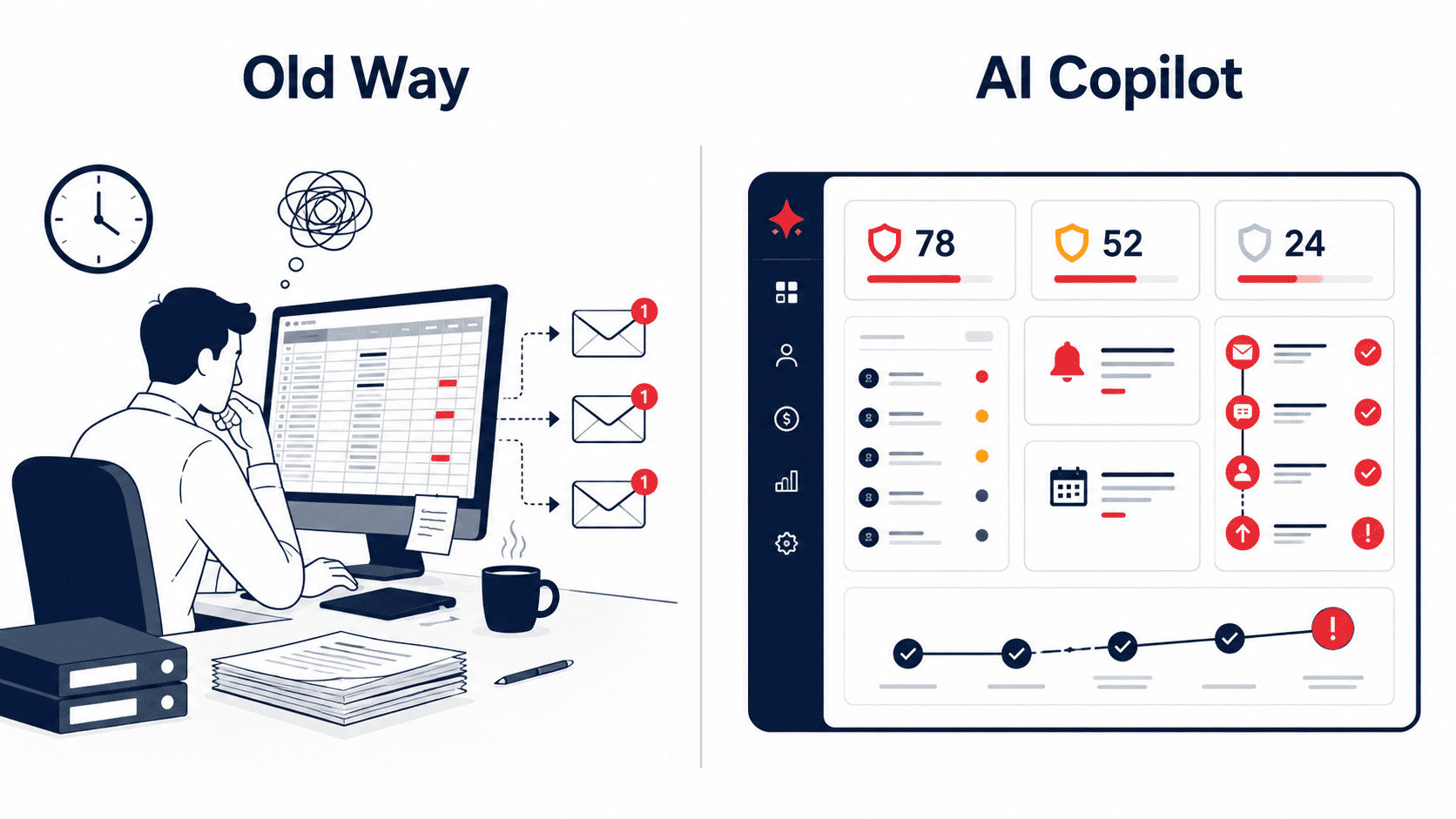

Your AR team is sending follow-up emails. Calls are being made. Reminders are going out. Yet cash keeps arriving late, DSO keeps rising, and you still do not know which customers are most likely to default next month. If this sounds familiar, you are not alone. The problem is not effort. It is the absence of the right system. That is precisely where debt collection management software makes its impact.

Unlike collection agencies that take 25–30% of every invoice they recover, or ERP systems that show you aging reports but do nothing with them, purpose-built debt collection software automates follow-ups, scores customer risk, tracks every promise-to-pay, and gives finance leaders real-time visibility into incoming cash. This guide covers everything you need to know, from core features and AI capabilities to implementation, integrations, and a detailed look at how OptimAR solves this for B2B finance teams.

Debt collection management software helps B2B finance teams track overdue invoices, automate multi-channel payment follow-ups, prioritize at-risk accounts, manage escalation workflows, and reduce Days Sales Outstanding (DSO). Unlike collection agencies, it keeps collections in-house, protects customer relationships, and gives CFOs real-time visibility into cash flow and receivables risk.

What Is Debt Collection Management Software?

In straightforward terms, debt collection management software is a tool that sits on top of your ERP or accounting system, monitors every overdue invoice, and helps your team collect payments in a structured, consistent way. Think of it as a traffic controller for your receivables. Many vendors call this a debt collection platform, and the name fits. Instead of your collectors deciding who to chase today based on memory or a spreadsheet, the system tells them, ranked by risk, value, and urgency, and then automates the routine outreach while they handle the complex cases.

At its core, this is overdue invoice management software. It automates payment reminders across email, SMS, and WhatsApp, organizes invoices by aging buckets, scores customer payment risk, tracks every promise-to-pay, manages escalation workflows, and gives your AR team a prioritized daily worklist. For CFOs, it provides real-time dashboards on DSO trends, aging summaries, at-risk customers, and expected cash inflows.

What It Is NOT

Before diving deeper, it helps to be clear about what this category is not, because these three things are often confused:

| Category | What It Is | Why It Is Different |

|---|---|---|

| Debt Collection Agency | A third party that chases debt on your behalf | Charges 25–30% of the invoice amount. Damages customer relationships. Used as a last resort, not a daily tool. |

| ERP / Accounting Software | Records invoices, maintains a ledger, produces static aging reports | Record-keeping, not process execution. Cannot automate dunning, track promises-to-pay, score risk, or manage escalations. |

| Consumer Debt Recovery Software | Built for banks, NBFCs, and lenders recovering consumer loans | Designed for enforcement, legal compliance (FDCPA, SARFAESI), and field agents. B2B invoice collections are fundamentally different. |

Where It Fits in Your Order-to-Cash Cycle

The order-to-cash (O2C) cycle covers everything from credit approval to payment reconciliation. Debt collection management software sits between invoice delivery and cash application. It is the execution layer that drives consistent follow-up, ensuring every overdue invoice moves through a defined process rather than sitting in someone’s inbox waiting to be remembered.

Why B2B Finance Teams Are Actively Searching for This

The numbers explain the urgency. According to Atradius research, half of all B2B invoices globally are currently overdue. The Upflow data from their State of B2B Payments 2024 report puts the median DSO across industries at 56 days. And the Hackett Group‘s 2025 Working Capital Survey found an 18-day DSO gap between top and median performers. That represents a $600 billion working capital opportunity sitting uncaptured.

In India, the scale is even more striking. The Delayed Payments 3.0 report by GAME, FISME, and C2FO found that ₹7.34 lakh crore was locked in delayed MSME receivables as of March 2024, affecting 6.4 crore MSMEs. For context, that is roughly the GDP of a mid-sized state, sitting idle in unpaid invoices.

The root cause is rarely customers refusing to pay. More often it is a combination of three things: inconsistent follow-up (reminders stop when collectors get busy), poor prioritization (all accounts treated the same regardless of risk), and zero early warning (CFOs learn about cash flow problems after they have already arrived, not before).

“DSO is a trailing indicator. By the time it rises, the risk that caused the rise is already months old.” Source: Credit Pulse

Collections management software is the structural answer to these problems. It does not just send more reminders. It replaces reactive, memory-dependent processes with a systematic, AI-informed approach to getting paid.

Who Needs Debt Collection Management Software?

For CFOs and Finance Heads

Your primary concern is cash. Specifically: how much is coming in, when, and from which customers. Today, that answer requires pulling aging reports, cross-referencing with collection notes, and making assumptions about who will pay this week. Debt collection software replaces that process with real-time dashboards showing DSO trends, aging buckets, at-risk customer scores, and forecasted cash inflows. You get the early warning system your current ERP cannot provide.

For AR Managers and Collections Teams

Your team spends 30–40% of the day sorting emails, preparing for calls, and figuring out who to chase next. They have not contacted a single customer yet. A purpose-built system gives collectors a daily prioritized worklist, automates routine follow-ups across email and WhatsApp, and tracks every interaction and commitment in one place. When a promise-to-pay is made, the system pauses reminders automatically and resumes if the payment does not arrive.

For Finance Controllers and Credit Controllers

Credit decisions and collection outcomes are directly connected: a customer’s payment history should inform their credit limit, and vice versa. Dedicated collections software gives you behavioral scoring for each customer, dispute tracking so nothing falls through the cracks, and escalation workflows that trigger automatically when an account crosses a risk threshold. You gain the data to make informed credit decisions, not just reactive ones.

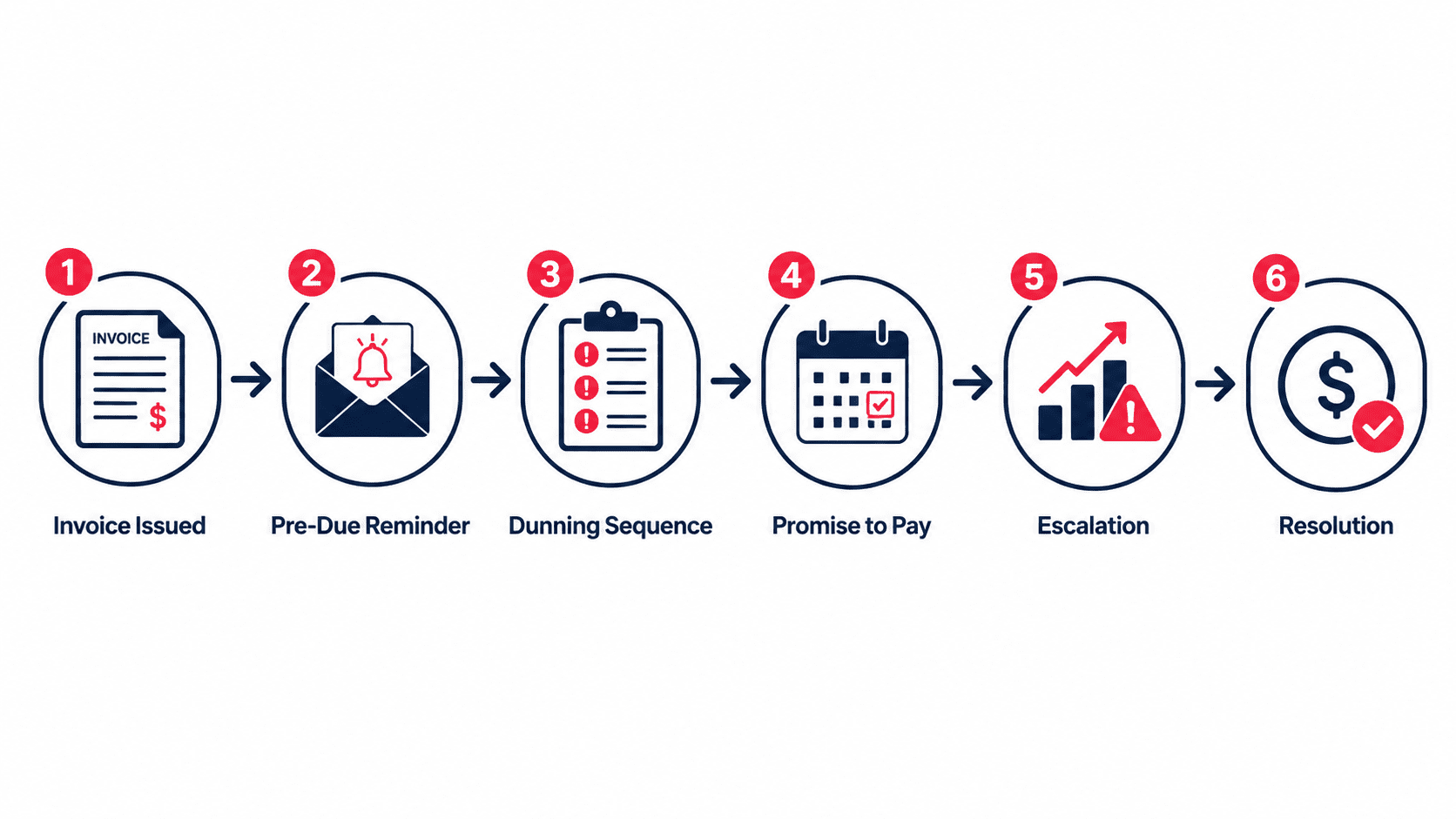

The B2B Collections Lifecycle: 6 Stages

Most finance teams think of collections as “send a reminder.” The reality is a six-stage process, and failure at any stage extends your DSO. Understanding this lifecycle is what separates companies with 35-day DSO from those stuck at 65 days.

Invoice Issued

Invoice is created and delivered. Accuracy here prevents disputes downstream. Errors in PO numbers, pricing, or payment terms account for around 61% of late payments.

Pre-Due Reminder

3–7 days before the due date, a soft reminder goes out automatically. Most customers pay at this stage if reminded. No software means this step gets skipped when teams are busy.

Dunning Sequence

After the due date passes, automated reminders escalate in tone: polite on Day 1, firmer on Day 7, urgent on Day 15. Multi-channel: email, SMS, WhatsApp, customer portal.

Promise-to-Pay

Customer commits to a payment date. Software captures the commitment, pauses reminders, and automatically alerts the collector if the promise is broken.

Escalation

High-value or high-risk accounts escalate from automated reminders to direct collector calls, then manager review, then credit hold. Triggers are behavior-driven, not time-based alone.

Resolution or Write-Off

Invoice is either resolved through payment, a dispute settlement, or a formal write-off decision. Data from this stage feeds risk scoring for future credit decisions.

Without software, this process depends entirely on individual memory and Excel. When a key collector leaves, the history of promises, disputes, and payment patterns disappears with them. The right system makes the entire lifecycle independent of any single person.

Key Features of Debt Collection Management Software

Not all debt collection management software is built the same. The features that matter vary depending on your role. Here is a breakdown of the core debt collection software features, organized by what each buyer persona actually cares about:

| Feature | What the CFO Cares About | What the AR Manager Cares About | What the Collections Head Cares About |

|---|---|---|---|

| Invoice Aging & AR Tracking | Real-time view of total exposure by aging bucket | Which invoices are overdue today and by how long | Which accounts have not been touched this week |

| Automated Dunning / Reminders | Consistency: reminders go out whether the team is busy or not | Multi-channel sequences (email, WhatsApp, SMS) without manual effort | Cadence control: how many touches before escalation |

| Risk Scoring & Prioritization | Early warning: which customers are most likely to delay or default | Daily prioritized worklist so time is spent on highest-impact accounts | Portfolio-level risk view across the entire AR book |

| Promise-to-Pay Tracking | Forecast reliability: promised payments included in cash flow projection | Automatic pausing of reminders when a commitment is recorded | Broken promise alerts with immediate escalation triggers |

| Escalation Workflows | Visibility into accounts where automated follow-up has failed | Clear handoff: when automation stops and human intervention starts | Structured escalation paths with audit trail for every decision |

| Dispute Management | Understanding how much AR is tied up in disputes vs. genuine payment delay | Centralised dispute log so nothing gets lost across email threads | Resolution SLAs so disputes are closed, not parked indefinitely |

| Customer Payment Portal | Fewer calls to the AR team; self-service reduces collection cost | Customers can view invoices, raise disputes, and pay online without a call | UPI and payment link embedding directly into reminder messages |

| DSO Dashboards & Cash Flow Analytics | Weekly DSO trend, forecast vs actual cash collection, bad debt risk | Collector productivity: how many accounts touched, promises received, payments collected | Team performance reports without manual data pulling |

A well-built automated payment reminder software does far more than send emails on a schedule. Beyond this list, one feature deserves extra attention: bidirectional ERP sync. If your collections software pulls invoice data from your ERP but does not sync payments back in real time, collectors end up chasing invoices that have already been paid. This is one of the most common and damaging errors in manual and poorly integrated setups. Always verify that the sync is bidirectional and real-time, not batch-processed overnight.

How AI Is Transforming Debt Collection

AI debt collection is the fastest-moving shift in finance operations today. Old automated debt collection software sent reminders. New AI-powered systems decide which reminder to send, to whom, at what time, on which channel, in what tone, and then learn from the customer’s response to make the next interaction more effective. That shift from rule-based to predictive is the defining upgrade in 2025–2026.

Predictive Risk Scoring

Forrester’s report from March 2025 on AI use cases in AR automation identified collection management as the highest-impact application, specifically the ability to flag accounts likely to go past due 14 to 21 days before they actually do. This window is everything. It gives your team time to intervene with a relationship-preserving conversation rather than a debt-chasing email.

Next-Best-Action Recommendations

Instead of giving collectors a generic list, AI surfaces the next best action for every account. Should this customer receive an email or a WhatsApp message? Is this the right moment for a call from their dedicated account manager, or should the system send a self-service payment link? These micro-decisions, made consistently across hundreds of accounts, compound into significantly faster cash collection.

Agentic AI in Collections

The frontier of this category is agentic AI, meaning systems that do not just recommend actions, but take them autonomously. According to Gartner reports, 57% of finance teams are already implementing or planning to implement agentic AI. Deloitte’s CFO survey from Q4 2025 found that 54% of CFOs are prioritising AI agent integration as a transformation goal, and 87% say AI will be critical to finance operations in 2026.

AI and Customer Relationships

A common concern is that AI will make collections feel cold or aggressive. The opposite is true when configured correctly. AI enables personalization at scale, tone adapts to payment history, channel preference, and relationship status. A long-term customer who has always paid on time receives a very different message than a new account with a first-time overdue invoice. This precision preserves relationships that manual collections cannot protect.

How Debt Collection Management Software Reduces DSO

What DSO Is and How to Calculate It

Days Sales Outstanding (DSO) measures how long it takes your business to collect payment after a sale on credit. The formula is straightforward:

DSO = (Average Accounts Receivable ÷ Net Credit Sales) × Number of Days

The lower your DSO, the faster you are converting invoices into cash. Per Upflow data, the global median DSO across industries is 56 days. The top-performing companies run 18 days below that median. According to the Hackett Group‘s 2025 survey, that 18-day gap represents $600 billion in uncaptured working capital for the 1,000 largest US public companies alone.

Industry DSO Benchmarks

| Industry | Average DSO | Top Performer DSO | Value of Closing the Gap |

|---|---|---|---|

| Manufacturing | 55–65 days | 35–40 days | 20–25 days of cash freed per cycle |

| Distribution / Wholesale | 50–60 days | 30–38 days | Faster inventory reinvestment |

| Professional Services | 45–60 days | 28–35 days | Lower borrowing cost, stronger liquidity |

| Logistics | 50–65 days | 35–42 days | Reduced working capital pressure |

| FMCG Distribution | 45–55 days | 25–35 days | Better credit cycle management |

6 Ways Collection Software Reduces DSO

- Pre-due reminders catch slow payers before the invoice is even overdue, eliminating the first delay entirely.

- Risk-based prioritization ensures collectors focus on high-value, high-risk accounts first, not whoever comes up next on a spreadsheet.

- Promise-to-pay tracking converts verbal commitments into forecasted cash, and ensures follow-up when a promise breaks.

- Dispute management closes invoice disputes faster, removing one of the biggest reasons for delayed payment in B2B.

- Accurate cash application stops collectors from chasing invoices that have already been paid, eliminating duplicate effort and customer frustration.

- Early escalation moves high-risk accounts into human hands before they become uncollectable, reducing bad debt write-offs.

Debt Collection Software vs. Hiring a Collection Agency

Many finance teams consider bringing in a collection agency when overdue invoices pile up. The comparison below shows why in-house debt collection and recovery software almost always delivers a better outcome for B2B companies with ongoing customer relationships.

| Factor | Collection Agency | Debt Collection Software |

|---|---|---|

| Cost | 25–30% of every invoice recovered | Flat monthly or annual fee regardless of recovery volume |

| Control | No control over how the agency approaches your customers | Full control over tone, timing, channel, and escalation rules |

| Customer Relationship | High risk of permanent damage; customers may churn | Relationship-preserving; outreach stays professional and personalised |

| Speed | Agency involvement signals the relationship is in crisis | Proactive follow-up starts before invoices go significantly overdue |

| Data Visibility | Little to no reporting back on customer behaviour or payment patterns | Full analytics: DSO, aging, risk scores, collector productivity |

| Best Use Case | Last resort for severely delinquent or charged-off accounts | Day-to-day management of all overdue invoices across your AR book |

The practical recommendation: use debt collection software for your entire active AR. Reserve agencies, if ever, for accounts that have gone completely silent after all internal escalation paths have been exhausted.

How Is This Different from Your ERP?

The most common objection to buying dedicated accounts receivable collection software is: “Our ERP already handles AR.” It does not, not in the way a business that relies on trade credit actually needs it to.

| Capability | ERP AR Module | Dedicated Collections Software |

|---|---|---|

| Invoice aging reports | Yes: static, pull on demand | Yes: dynamic, real-time, action-triggered |

| Automated dunning sequences | Rarely, and very basic | Core feature: multi-step, multi-channel, configurable |

| Promise-to-pay tracking | No | Yes: with automatic reminders on breach |

| Risk scoring & prioritization | No | Yes: AI-powered, behaviour-based |

| Collector worklist | No | Yes, prioritized daily task queue per collector |

| Customer payment portal | No | Yes, self-service, with invoice copies and payment links |

| Cash flow forecasting from AR | No | Yes, based on payment predictions and PTP data |

| Escalation workflow management | No | Yes: rules-based or AI-triggered |

As PYMNTS reported in 2026, finance teams are rapidly discovering that ERP-native AR modules “assume stable data inputs, predictable customer behaviour, and limited exception handling”, none of which describe a real B2B collections environment. The ERP records what happened. Dedicated software actively drives what happens next.

Which Industries Need Debt Collection Management Software Most?

Any B2B company extending trade credit can benefit. However, the industries where the pain is sharpest, and the ROI fastest, share three characteristics: high invoice volume, extended payment terms (net-30 to net-90), and large numbers of customer accounts to manage simultaneously.

- Manufacturing: Complex distributor networks, multi-level credit terms, and disputed short-pays make collections genuinely difficult. Over half of manufacturing suppliers report late payments averaging close to two months past due.

- Distribution and Wholesale: High invoice frequency, thin margins, and dealer/retailer relationships mean late payments compound fast. A single distributor paying 30 days late can unlock or block an entire month’s restocking cycle.

- FMCG Distribution: India-specific, FMCG distributors often operate on 60–90 day credit cycles with hundreds of small retailers. WhatsApp-native reminders embedded in payment links cut credit cycles dramatically.

- Gems and Jewellery / Textiles: High-value, relationship-sensitive industries where aggressive collections are not an option. Automated, professional follow-ups allow consistent collections without risking long-standing trade relationships.

- Logistics and Freight: Messy multi-format billing, freight disputes, and proof-of-delivery dependencies create built-in collection delays that software helps systematise and resolve.

- Professional Services and IT Services: Milestone-based billing creates irregular invoice timing, making manual tracking unreliable. Dedicated AR software keeps every milestone invoice in a structured follow-up flow regardless of the billing pattern.

Integrations That Make Debt Collection Software Work

A collections platform is only as strong as its data connections. Most modern cloud based debt collection software connects to your ERP and payment systems via API, making setup faster and sync more reliable. Here are the integrations that matter most, with particular attention to what Indian B2B companies need:

| Integration Type | Key Platforms | Why It Matters |

|---|---|---|

| ERP / Accounting | SAP, Oracle NetSuite, Tally, BUSY, Zoho Books, QuickBooks, Xero, Microsoft Dynamics | Bidirectional sync keeps invoice data accurate. Payments auto-close in the collections workflow. |

| Gmail, Microsoft Outlook | Reminders sent from your own domain, not a generic system, maintaining trust with customers. | |

| WhatsApp Business API | 98% open rate in India. Payment links embedded directly in WhatsApp messages cut days off collection cycles. | |

| Payment Gateways / Rails | Razorpay, PayU, Stripe, UPI, NACH, NEFT, IMPS | Customers can pay directly from the reminder message. No manual bank transfer tracking needed. |

| CRM | Salesforce, HubSpot | Keeps sales teams informed about collection issues on key accounts before they become relationship problems. |

One more thing worth knowing: always demand a live integration demo with your actual ERP data, not a generic sandbox. A broken sync is one of the most common implementation failures, and it results in collectors chasing invoices that have already been paid, exactly the problem you are trying to solve.

Debt Collection Software India: What Is Different for B2B Teams

The global B2B collections software market was valued between USD 3.44 billion and USD 4.79 billion in 2025, depending on the analyst. Asia-Pacific is the fastest-growing region, with India at the centre of that growth. However, the Indian B2B collections context has specific characteristics that generic global software often misses entirely.

Tally and BUSY Integration

The vast majority of Indian SMEs and mid-market companies run Tally or BUSY as their primary accounting system. Most global AR platforms do not integrate with these at all, or offer only one-way exports. Any debt collection management software evaluated for an Indian company must offer a genuine, bidirectional Tally or BUSY integration, ideally through a cloud-sync connector rather than a manual data export.

WhatsApp as a Primary Collection Channel

In India, WhatsApp is not an add-on feature, it is often the primary way business communication happens between sellers and buyers. Payment collection software that supports the WhatsApp Business API enables you to send payment reminders, invoice copies, and UPI payment links through the same channel your customer already checks dozens of times a day. This alone can reduce average collection time significantly in Indian market contexts.

Section 43B(h) and the MSME Payment Rule

Effective from assessment year 2024–25, Section 43B(h) of the Income Tax Act disallows a buyer’s tax deduction if payment to a registered micro or small enterprise is not made within 15 days (without a written agreement) or 45 days (with an agreement). This gives B2B sellers from the MSME segment a powerful financial incentive for buyers to pay on time, and makes systematic collections tracking legally relevant, not just operationally useful.

MSME Samadhaan and TReDS

The government’s MSME Samadhaan portal provides an online dispute resolution mechanism for MSME payment disputes, now mandatory from October 2025. Separately, TReDS (Trade Receivables Discounting System) allows MSME suppliers to discount approved invoices for early liquidity. Both mechanisms work better when your internal AR data is clean, current, and systematically managed, which is exactly what collections software enables.

For Indian B2B finance teams, the combination of regulatory pressure, WhatsApp-native collections, Tally/BUSY integration requirements, and UPI payment rail support makes the India market context genuinely distinct from the global norm. Explore AP/AR automation solutions purpose-built for this context, and largely underserved by mainstream global AR platforms.

Ready to Discuss Your Accounts Receivable Requirements?

Our team works with B2B finance leaders across manufacturing, distribution, and professional services to design collections systems that reduce DSO and improve cash flow visibility.

Talk to Softlabs GroupMeet OptimAR: AI-Powered Collections Copilot for B2B Finance Teams

Built by Ainfinite AI (Softlabs Group) specifically for mid-market B2B companies managing overdue invoices at scale.

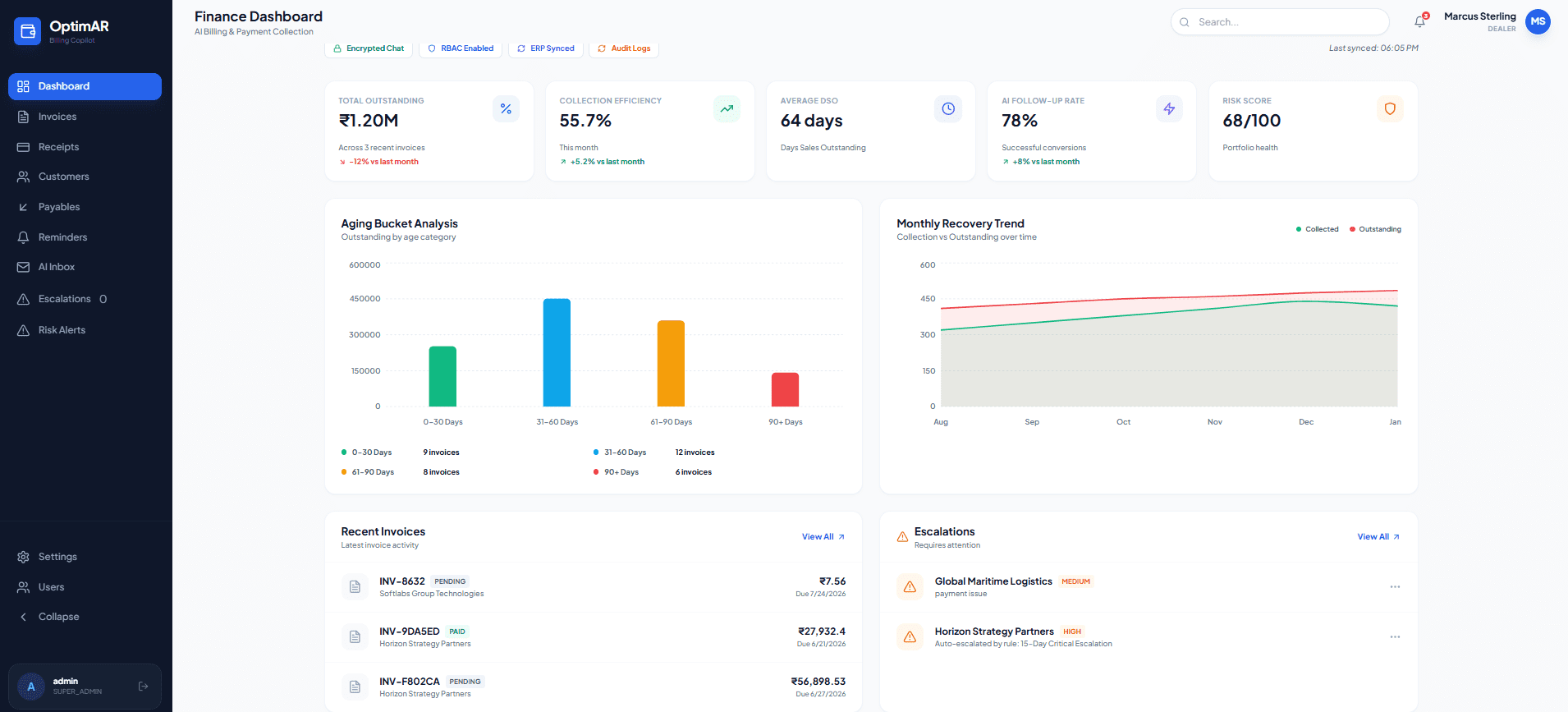

Full AR Dashboard: Everything in One View

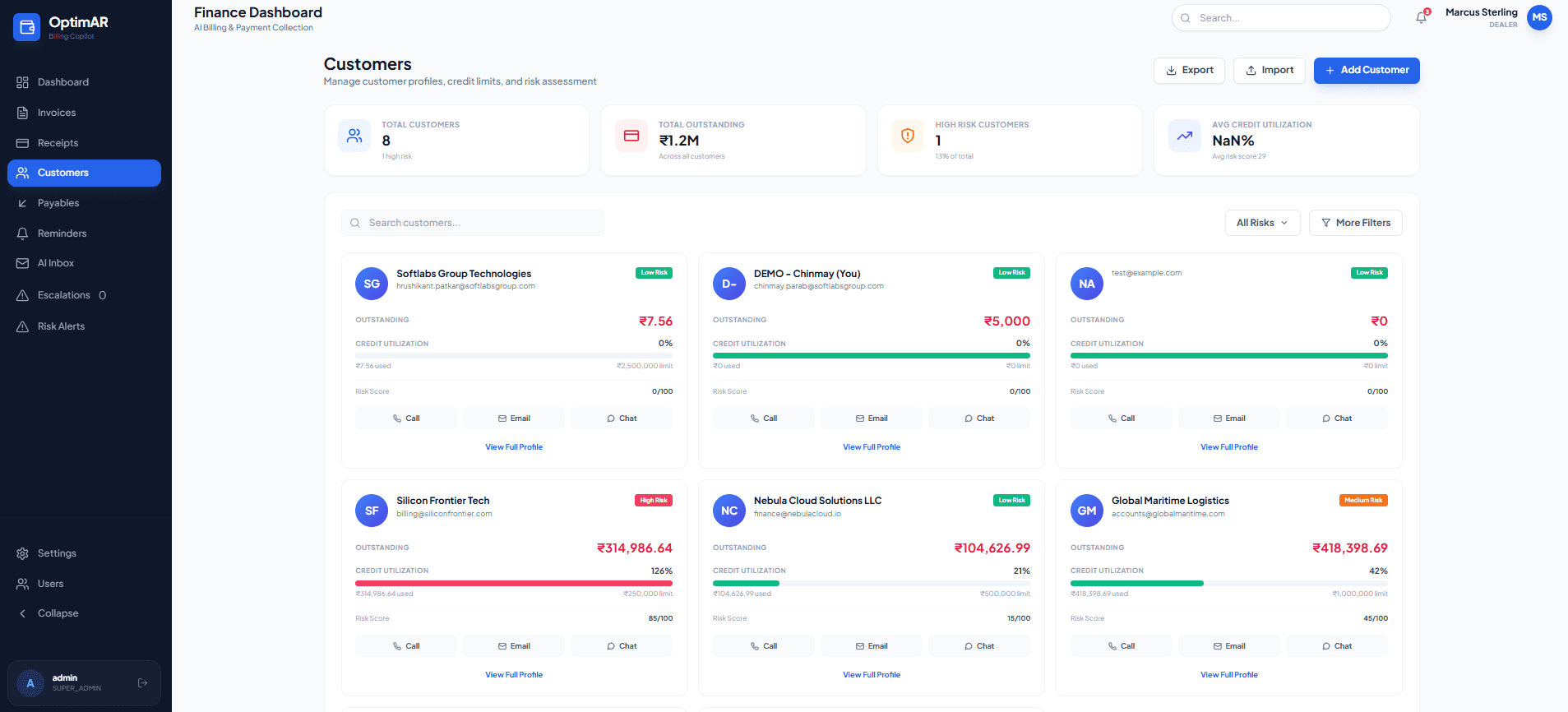

OptimAR’s central dashboard gives your CFO and finance head a real-time view of total outstanding receivables, aging buckets, DSO trend, top overdue accounts, and collection team performance, without opening a single spreadsheet. Every metric updates as payments come in and reminders go out.

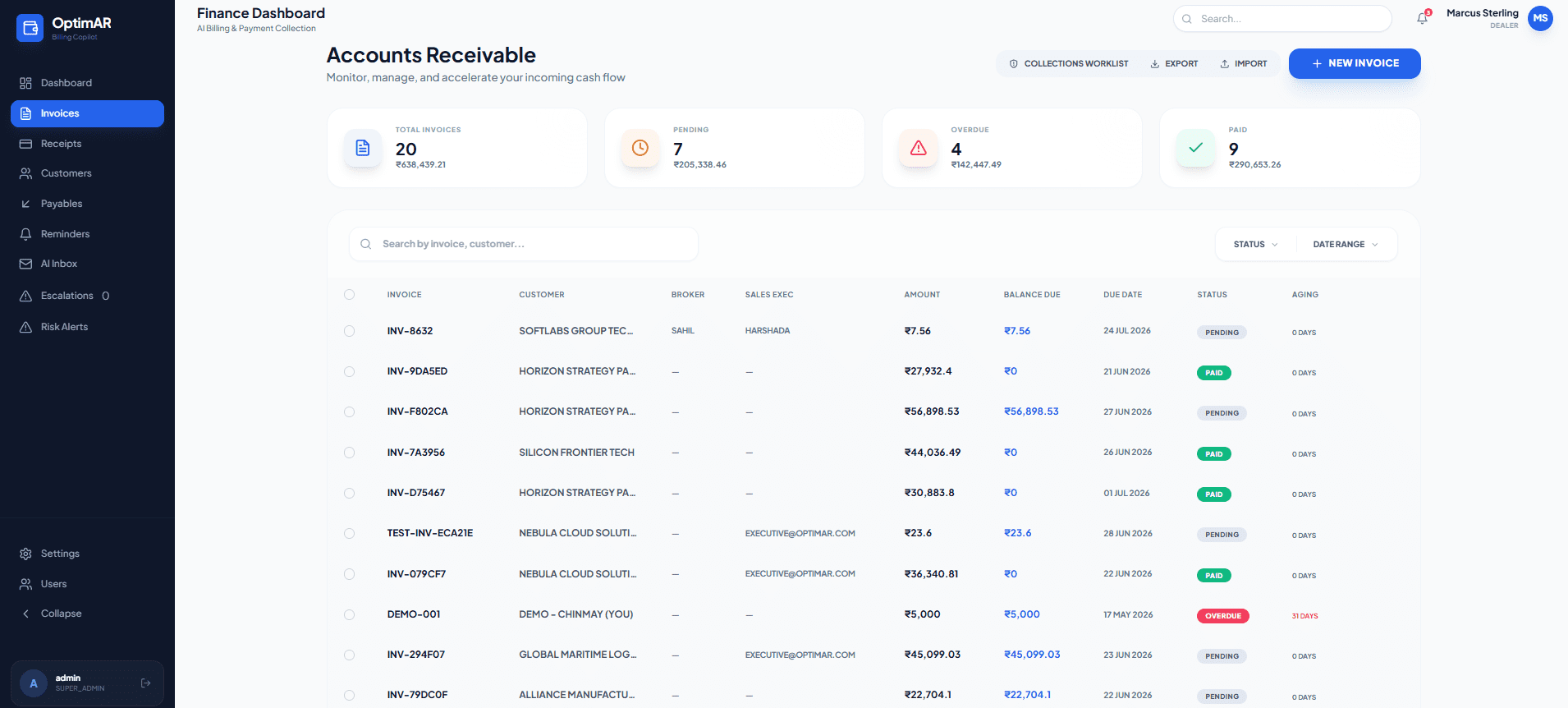

Overdue Invoice Tracking: Nothing Slips Through

Every overdue invoice is captured, classified by aging bucket, and tagged with its collection status. OptimAR syncs bidirectionally with your ERP or accounting system, Tally, Zoho Books, SAP, QuickBooks, so invoice data is always current. When a customer pays, the invoice closes automatically. No more chasing already-settled accounts.

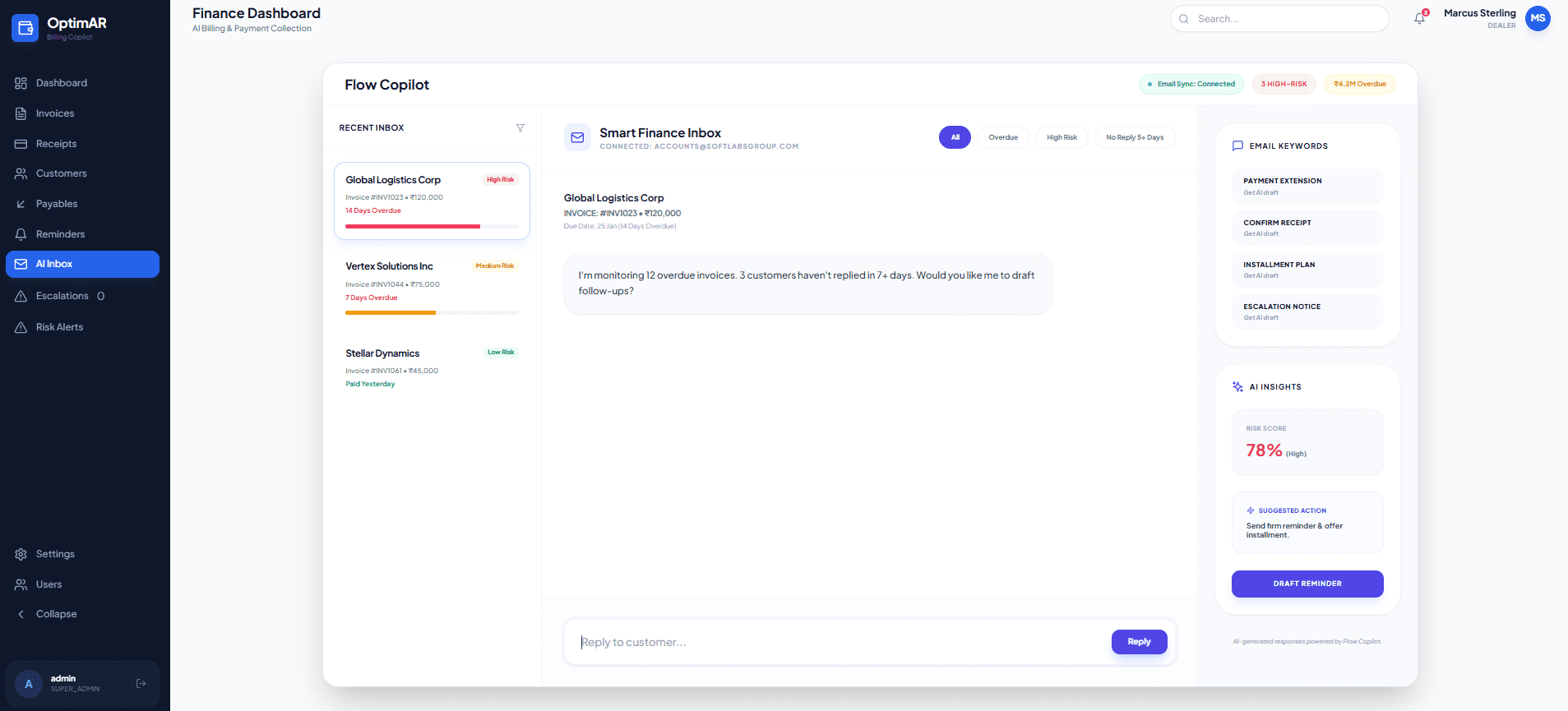

ProfitPilot: Your AI Collections Inbox

ProfitPilot is OptimAR’s AI-powered collections inbox that reads inbound customer replies and classifies them automatically: payment promise, dispute, document request, or payment received. Your collectors see only what needs a human response. Routine confirmations and payment acknowledgements are handled by the AI, freeing your team for the conversations that actually require judgment.

Customer Risk Scoring: Know Who Will Pay Late Before They Do

OptimAR’s AI engine scores every customer based on payment history, invoice aging patterns, promise-to-pay behaviour, and account value. High-risk customers are flagged before their invoices go overdue, giving your team the 14–21 day window to intervene proactively rather than reactively. Credit limit recommendations update automatically as risk profiles change.

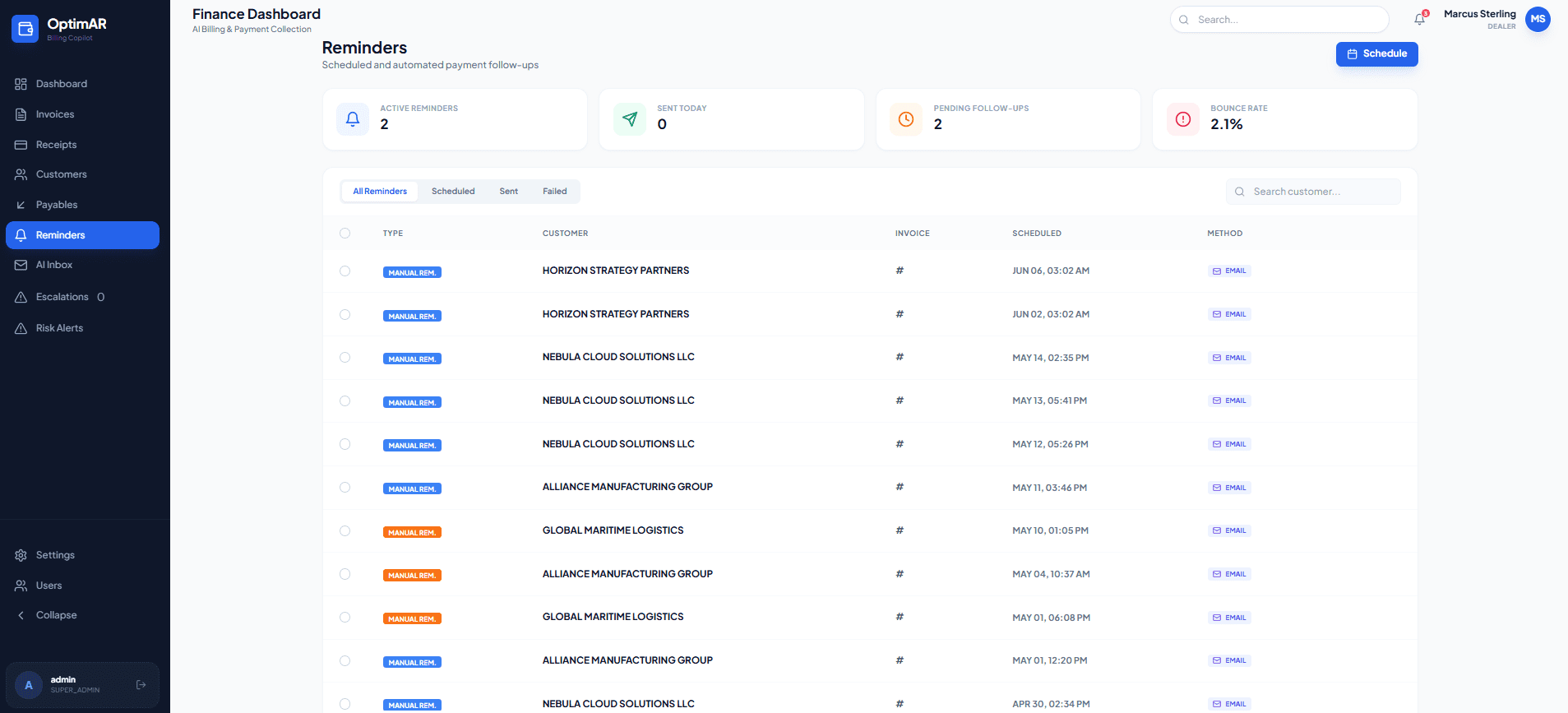

Automated Payment Reminders: Multi-Channel, Always On

OptimAR sends pre-due, due-date, and post-due reminders across email, SMS, and WhatsApp, with UPI payment links embedded directly in the message. Tone adapts automatically: polite for a first reminder, firmer for a 15-day overdue invoice. Reminders pause when a promise-to-pay is captured and resume if the payment does not arrive. No manual intervention needed for routine accounts.

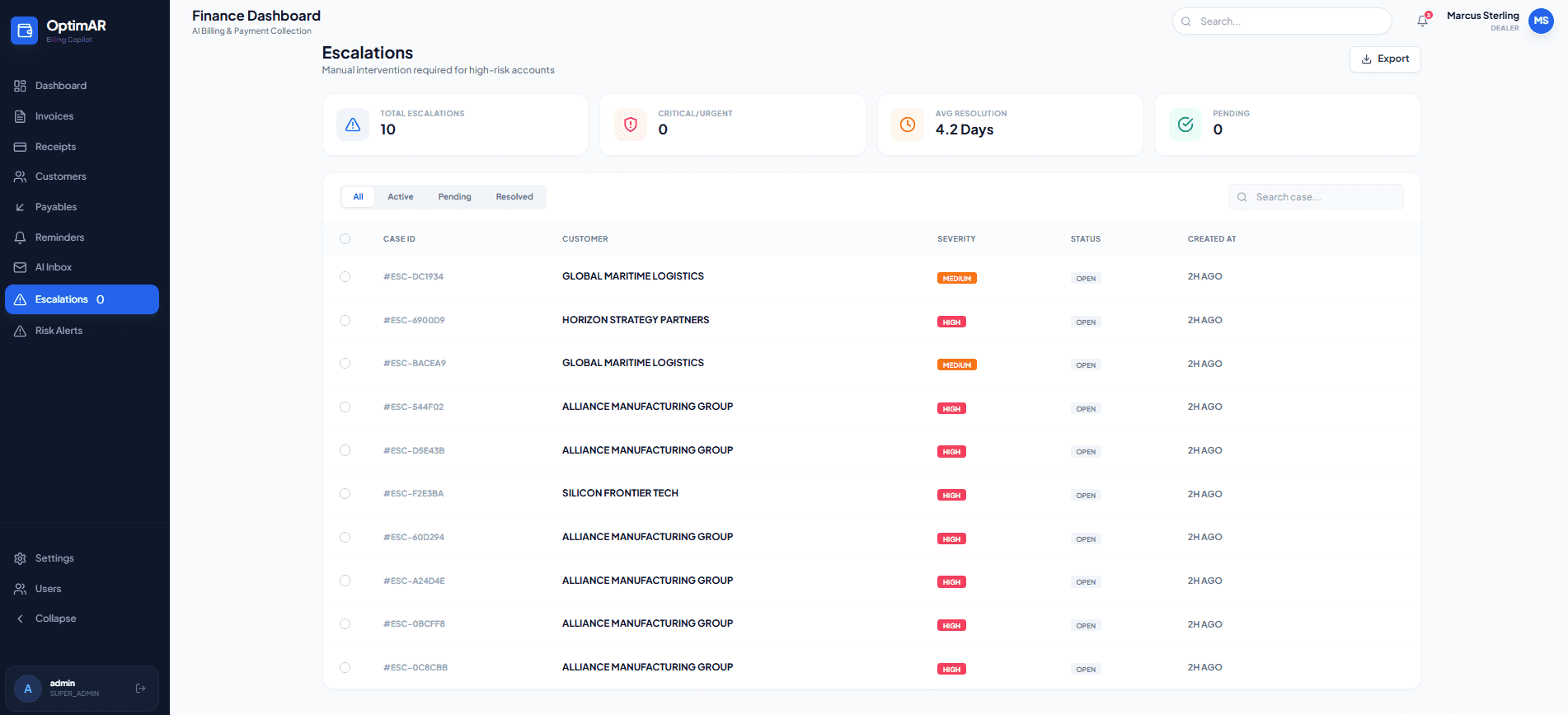

Escalation Management: The Right Account Reaches the Right Person

When automated reminders have run their course and a customer still has not paid, OptimAR triggers a structured escalation: collector call, account manager review, manager approval for credit hold. Every escalation step is logged with a full audit trail. Nothing falls through based on someone’s memory or judgment about when to escalate.

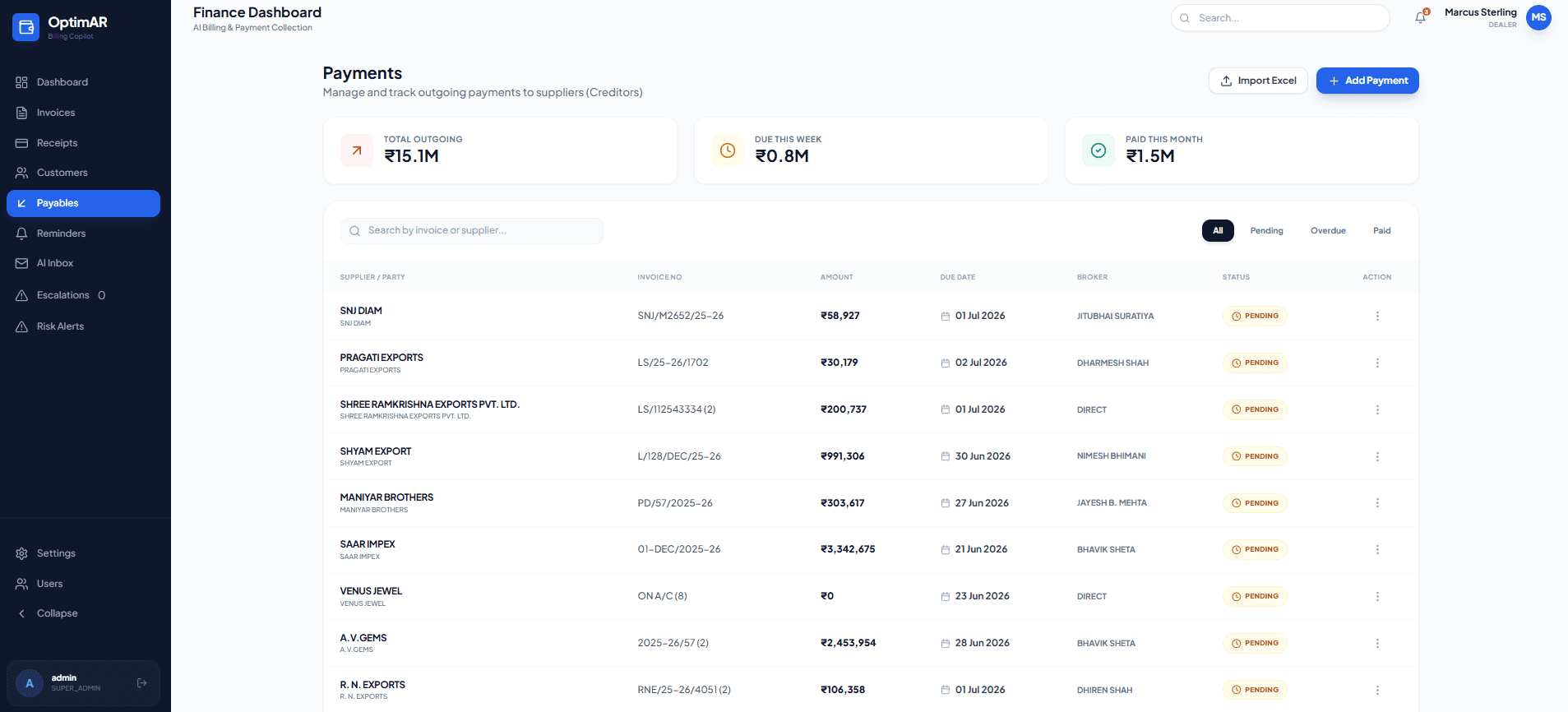

Payables and Receipts Visibility: The Full Cash Picture

OptimAR gives your finance team a unified view of both what is owed to you and what is coming in, combining accounts receivable with payables context so CFOs can make working capital decisions with complete information. Receipts are auto-matched to open invoices, reducing the manual reconciliation burden on your accounting team.

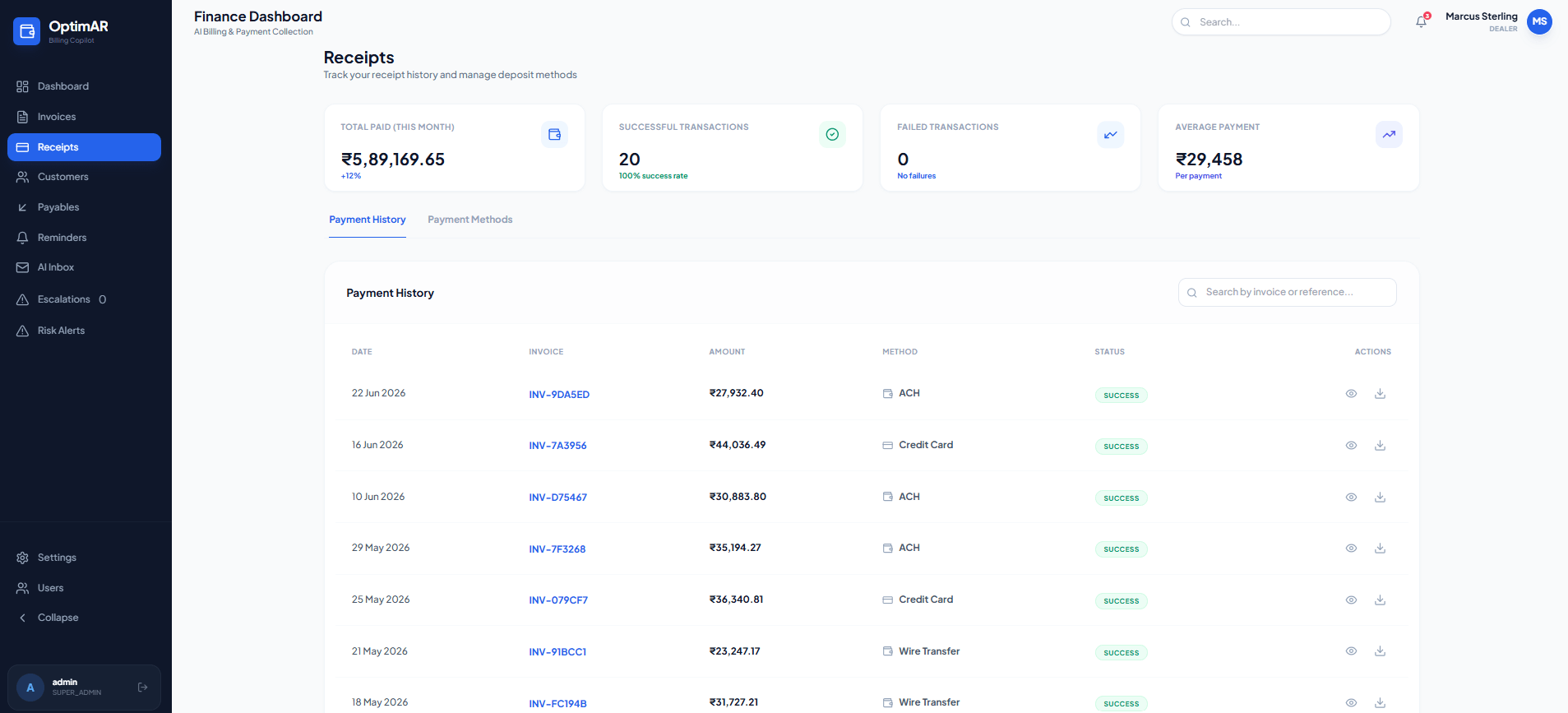

Receipt Tracking and Auto-Reconciliation

Every payment received is captured in OptimAR, matched to its corresponding invoices, and reflected across dashboards and collector worklists in real time. This eliminates the most damaging error in manual collections: chasing a customer who has already paid, which damages relationships and wastes team time on work that has already been done.

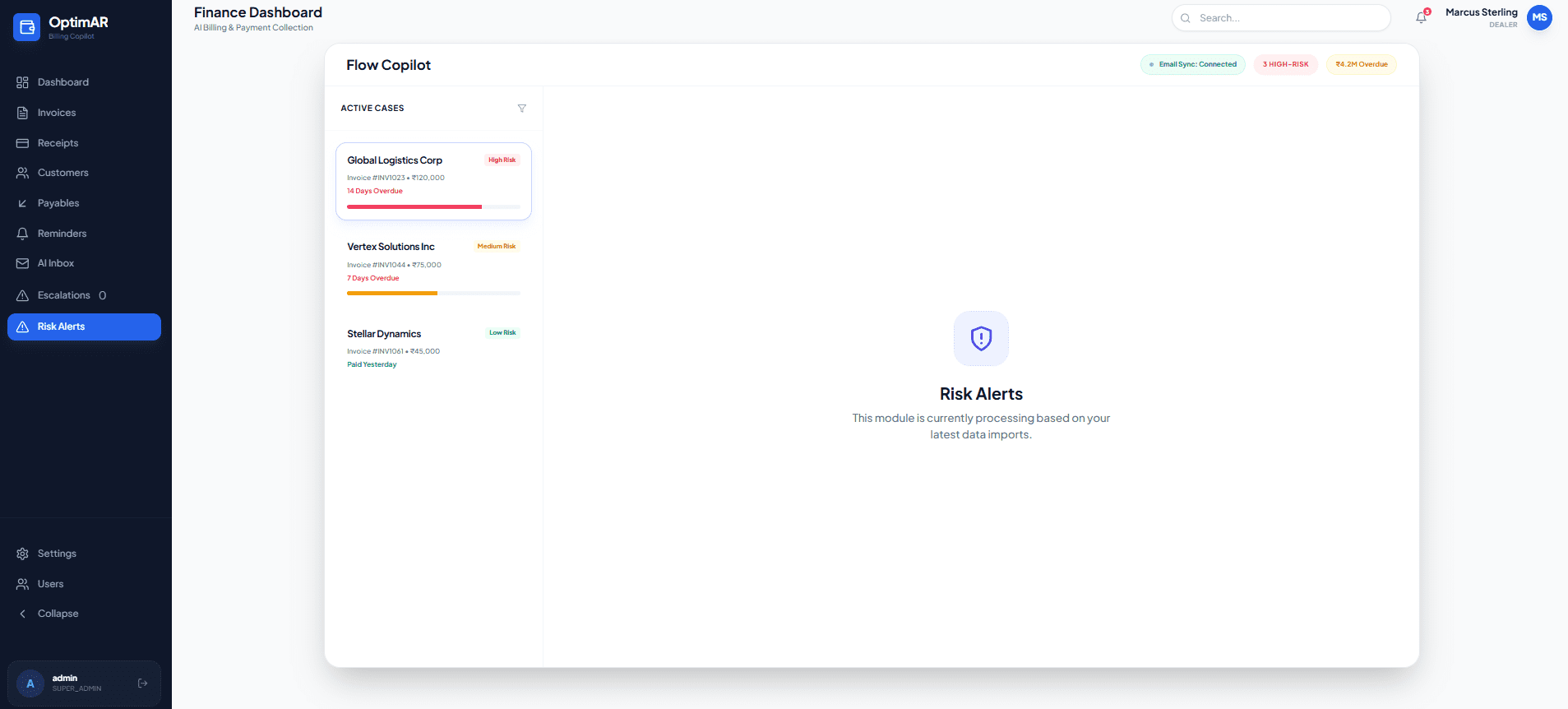

Risk Alerts: Early Warning for CFOs

OptimAR continuously monitors your AR portfolio and surfaces risk alerts when an account shows early warning signals: a change in payment behaviour, a sudden spike in overdue amount, or a broken promise-to-pay pattern. CFOs receive proactive alerts before a cash flow problem arrives, not a DSO report after it has already happened.

How to Choose the Right Debt Collection Management Software

Choosing the wrong tool, or buying for features rather than fit, is one of the most common and costly mistakes in this category. Here is the checklist that matters:

- ERP integration depth: Does it connect bidirectionally with your specific ERP (Tally, SAP, Zoho, QuickBooks)? Demand a live demo with your actual data, not a generic sandbox.

- Automation configurability: Can you set different dunning sequences for different customer segments, invoice values, or overdue thresholds? One-size-fits-all cadences underperform.

- AI and predictive capability: Does the software score customer payment risk proactively, or just report what has already happened? Look for predictive insights, not just historical dashboards.

- Promise-to-pay and escalation tracking: Are PTP commitments captured automatically? Do escalations trigger on behaviour, or do collectors have to remember to escalate manually?

- Multi-channel outreach: Does it support WhatsApp with payment link embedding, not just email? For Indian B2B companies, this is non-negotiable.

- Usability and adoption: If your collectors do not use it, it does not work. Steep learning curves are the most common reason collections software fails to deliver ROI. Ask for references from teams of similar size.

- Security and compliance: Look for SOC 2 Type II certification, data encryption, and access controls. If you operate across geographies, verify GDPR and local data residency compliance.

- Pricing transparency: Avoid tools with hidden per-transaction fees, user seat penalties, or integration surcharges that make the total cost far higher than the headline price.

What Does Implementation Look Like?

Most finance teams overestimate implementation complexity and underestimate the importance of data quality at the start. Here is what a typical rollout looks like:

- Assess your current state: Baseline your DSO, aging distribution, error rate, and team capacity. Identify the single biggest pain, is it follow-up consistency, prioritization, or cash flow visibility?

- Choose an ERP-aligned vendor: Integration with your existing accounting system is the foundation. Everything else depends on this connection being reliable and bidirectional.

- Clean your AR data: The software is only as accurate as the data it receives. Deduplicate customers, verify payment terms, and resolve any open discrepancies before go-live.

- Design your workflows: Configure dunning sequences, escalation rules, customer segments, and PTP conventions. This is the most important configuration step, do not rush it.

- Pilot on one segment: Launch with one customer segment or region first. Measure DSO change, collector feedback, and payment response before scaling to the full AR book.

- Measure, refine, and scale: Review DSO trends, bad debt reduction, and team productivity monthly for the first quarter. Adjust workflows based on real data, then roll out fully.

Timeline expectations: lightweight SaaS tools with native integrations can go live in 1–2 weeks. Mid-market ERP-connected deployments typically take 6–10 weeks. Enterprise-level rollouts with complex multi-entity setups run 3–6 months. Rushing implementation without clean data and workflow design is the most common reason companies do not see the DSO reduction they expected.

Common Mistakes Finance Teams Make with Collections

Whether managing collections manually or choosing the wrong tool, these are the mistakes that consistently cost companies time, cash, and customer relationships.

When managing collections manually:

- Treating all invoices the same, no risk-based prioritization means the highest-value, highest-risk accounts get the same attention as a small, low-risk invoice.

- Relying on spreadsheets and individual memory, when a collector leaves, every relationship history, dispute note, and payment pattern leaves with them.

- Not chasing before the due date, most software users report that pre-due reminders alone recover 20–30% of invoices without any post-due outreach.

- Chasing invoices that are already paid, this happens when cash application does not sync with collections in real time.

- Keeping sales teams out of the loop, when a key account has a dispute or long overdue balance, the account manager often learns last, damaging the relationship further.

When choosing collections management software:

- Buying on price or feature list without testing the ERP integration live with your own data.

- Choosing point solutions that cover only reminders but leave cash application and dispute management still manual.

- Ignoring user adoption risk, a complex system the team does not use delivers zero DSO improvement.

- Not asking for references from companies of similar size and ERP setup.

- Skipping the pilot phase and going full-scale immediately, which makes it harder to identify configuration issues early.

Build Your Collections System with Softlabs Group

OptimAR is AI-powered accounts receivable and collections software built for B2B finance teams, with deep Tally, Zoho, and SAP integrations, WhatsApp-native reminders, and real-time cash flow visibility for CFOs. Talk to our team to see how it fits your current AR workflow.

Frequently Asked Questions

What is debt collection management software?

Debt collection management software is a tool that helps B2B finance teams systematically manage overdue invoices from their business customers. It automates payment reminders, tracks invoice aging, scores customer payment risk, manages escalation workflows, and gives CFOs real-time visibility into cash flow and DSO. It is designed for in-house finance and AR teams, not for third-party collection agencies or consumer debt recovery.

How is this different from hiring a debt collection agency?

A collection agency is a third party that pursues debt on your behalf, typically charging 25–30% of every invoice they recover. Dedicated collections software keeps the process in-house, at a flat monthly cost, with full control over tone, timing, and escalation. For B2B companies with ongoing customer relationships, software almost always delivers a better financial and relationship outcome than agency involvement, which is best reserved for severely delinquent accounts as a last resort.

How is this different from AR automation software?

The terms are often used interchangeably, but there is a distinction. AR automation covers the full order-to-cash cycle: invoicing, cash application, credit management, and collections. This type of software specifically refers to the collections execution layer, managing overdue invoices, dunning sequences, and escalation workflows. Most AR automation platforms include a collections module, and dedicated collections tools often cover most of the same ground for practical purposes.

What is DSO and how does collection software reduce it?

DSO (Days Sales Outstanding) measures how long it takes to collect payment after a credit sale. The formula is: (Average AR ÷ Net Credit Sales) × Number of Days. The global median DSO is 56 days. Collections software reduces it through consistent pre-due reminders, risk-based prioritization, promise-to-pay tracking, faster dispute resolution, and accurate cash application, each of which removes a specific cause of delayed payment. Top-performing companies run 18 days below the median DSO, per Hackett Group 2025 data.

How does AI improve debt collection?

AI transforms collections from rule-based reminders to predictive, adaptive workflows. It scores customer payment risk before invoices go overdue, flags accounts that are likely to delay 14–21 days in advance, recommends the right next action for each account (call, WhatsApp, payment link), and in advanced implementations handles inbound reply classification automatically. According to Forrester’s 2025 report, collection management is the highest-impact AI use case in accounts receivable automation.

What features should collections software have?

The core feature set should include: invoice aging and AR tracking, automated multi-channel dunning (email, SMS, WhatsApp), risk scoring and collector prioritization worklists, promise-to-pay tracking with automatic follow-up on breach, escalation workflow management, dispute and deduction management, a customer self-service payment portal, cash application and payment matching, and DSO dashboards with cash flow analytics. For Indian companies, Tally or BUSY integration and UPI payment link embedding are additional requirements.

Does this software integrate with Tally, SAP, or Zoho Books?

The best platforms do, though the quality of integration varies significantly. For Indian companies using Tally or BUSY, look specifically for bidirectional sync, not just a one-way data export. When evaluating any tool, request a live demo using your actual ERP data. A reliable bidirectional sync means payments posted in your ERP auto-close in the collections workflow, preventing the common mistake of chasing already-paid invoices.

What is promise-to-pay tracking and why does it matter?

Promise-to-pay (PTP) tracking captures a customer’s commitment to pay on a specific date. When a PTP is recorded, automated reminders pause automatically until that date arrives. If the payment does not come through, the system alerts the collector immediately and resumes the dunning sequence. Without this feature, broken promises get lost in email threads and the collection cycle extends unnecessarily. As one operations guide puts it: you cannot enforce what you do not track.

What is the difference between B2B and consumer debt collection?

B2B collections involves commercial invoices between businesses, typically larger amounts, ongoing relationships, and disputes driven by operational issues like pricing errors or missing PO numbers rather than inability to pay. Consumer debt collection involves personal loans, credit cards, or utility bills, enforcement-led, regulated by laws like FDCPA in the US or RBI guidelines in India, and often adversarial in nature. The two require fundamentally different software, strategies, and buyer personas.

How much does collections management software cost?

Pricing varies by company size and feature set. Lightweight SaaS tools for SMBs typically start at $50–$200 per user per month. Mid-market platforms with full ERP integration and AI features range from $200–$1,000 per month as a flat fee. Enterprise platforms like HighRadius use outcome-based or custom pricing. The real cost comparison is not software fee vs. no software, it is software fee vs. DSO reduction value. A 10-day DSO improvement on ₹10 crore in monthly credit sales frees approximately ₹33 lakh in working capital.

How long does implementation take?

Lightweight SaaS tools with native accounting integrations can be live in 1–2 weeks. Mid-market platforms connected to Tally, SAP, or Zoho Books typically take 6–10 weeks for a full rollout, including workflow configuration and team training. Enterprise implementations with multi-entity setups run 3–6 months. The most important pre-implementation step is data quality: clean customer records, accurate payment terms, and no open discrepancies in your ERP will shorten implementation time and improve outcomes significantly.

What is Section 43B(h) and how does it affect B2B collections in India?

Section 43B(h) of the Income Tax Act, effective from AY 2024–25, disallows a buyer’s tax deduction for expenses owed to registered micro or small enterprises if not paid within 15 days (without a written agreement) or 45 days (with one). This creates a direct financial incentive for buyers to pay MSME suppliers on time, and gives suppliers a stronger basis for structured follow-up. Finance teams at MSME-registered companies should document their follow-up activity systematically, which is exactly what collections software enables.