Executive Summary: Why Finance Teams Are Rethinking How Receivables Actually Get Managed

Your accounts receivable team closes another month with a queue of unapplied cash on the books. Order to Cash automation addresses this directly – acting as an intelligent coordination layer above your existing ERP, connecting bank feeds, remittance inboxes, lockbox data, and customer portal signals into one operating environment.

The problem is not a shortage of finance talent. It is a structural mismatch between the volume and fragmentation of incoming payment data and the finite capacity of the AR team. Cash applicationThe process of matching incoming payments to the correct open invoices in the accounts receivable ledger remains heavily manual in most organisations because remittances arrive late, references are inconsistent, and exceptions require judgment that standard ERP tools cannot provide.

Modern AI order to cash automation changes the equation. Rules engines handle policy-controlled decisions. Machine learning ranks uncertain matches by confidence. Human reviewers focus on deductions, disputes, and high-value exceptions where commercial judgment genuinely matters. The result is a finance team spending its time on work that requires its expertise – not on predictable matching tasks that an automated system handles more consistently.

For controllers, AR managers, and CFOs evaluating an end-to-end order to cash automation solution, this guide explains the technology honestly – including where it performs well and where human oversight remains essential.

1. Why Does the Order-to-Cash Process Keep Breaking Down at Scale?

The order-to-cash process breaks at scale because payments and remittances arrive fragmented, late, and often incomplete – faster than manual teams can reconcile them.

In practice, organisations deploying this type of system typically encounter a challenging early reality: the exception volume is far larger than initial estimates suggested. Remittance quality varies dramatically across the customer base. Some accounts send structured EDI files. Others attach a vague single-page PDF. A significant portion provides no remittance beyond a bank reference number. Each gap requires a human to investigate before any posting can occur.

Context: The Finance Operations Environment Where This Problem Lives

Finance operations teams in B2B businesses – manufacturing, distribution, SaaS, healthcare, and business services – typically manage hundreds or thousands of active customer accounts. Each carries its own invoicing requirements, payment terms, deduction policies, and portal submission rules. Orders flow from sales systems into the ERP. Invoices go out through email, EDI, and AP portal submissions. Payments arrive through bank transfers, checks, ACH, and card transactions – while remittance advice arrives separately, sometimes days later, sometimes never.

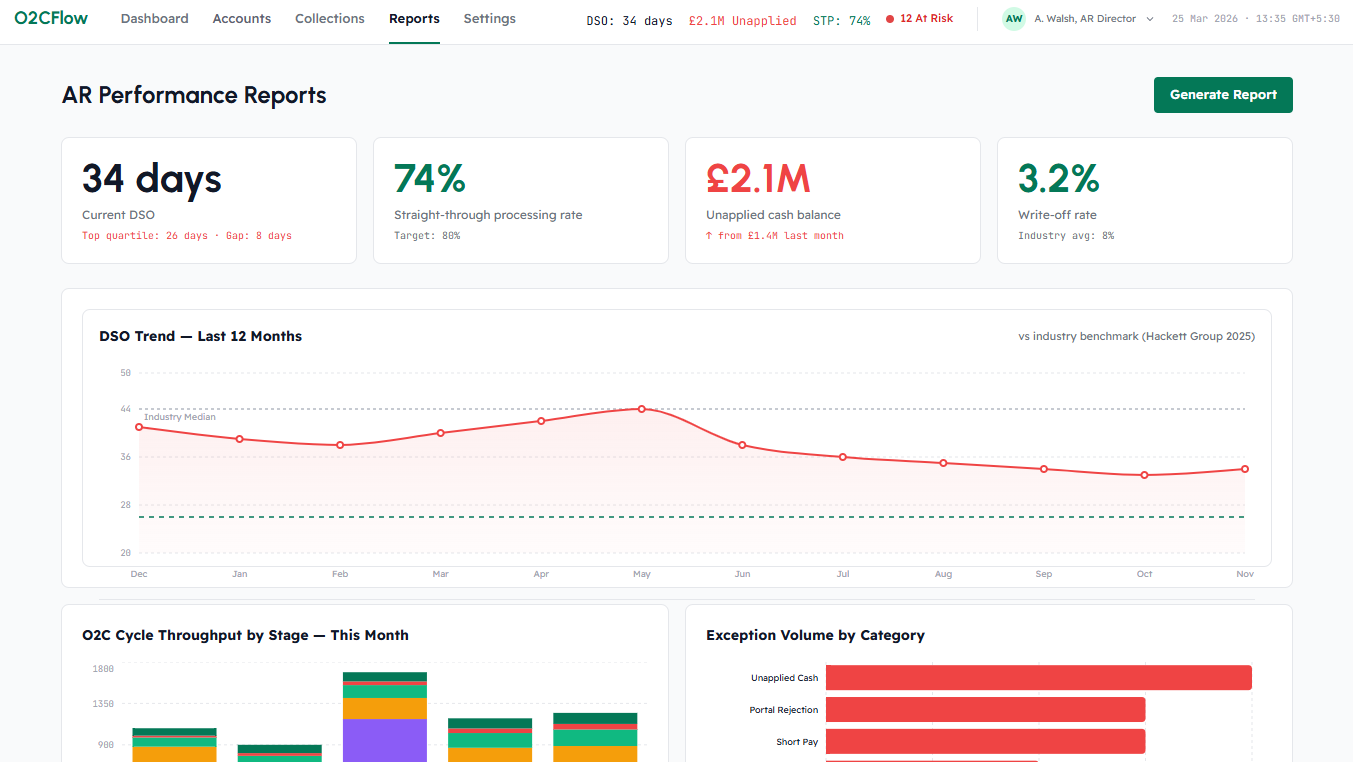

The Days Sales Outstanding (DSO)A measure of the average number of days a business takes to collect payment after a sale – a key indicator of AR efficiency and working capital health metric reflects how well this cycle runs. When matching is slow, exception handling lags, and collections follow-up is reactive, DSO rises. Cash sits unapplied in the bank – effectively frozen working capital. Order to Cash automation targets every stage of this cycle, not just the matching step.

Key Pain Points This AI Solution Addresses

- Unapplied cash and payment matching issues: Payments arrive without sufficient reference data, forcing analysts to search manually across open AR for the correct invoice. Backlogs of unmatched cash distort working capital visibility and delay order release for cleared accounts.

- Missing remittance data and reconciliation delays: Remittance advice arrives separately from payment – or not at all – making accurate cash application impossible without manual investigation across email inboxes, portals, and bank files simultaneously.

- Invoice disputes and deduction handling bottlenecks: Short-pays and deductions arrive with insufficient reason codes or supporting documentation. Without a centralised view, disputes sit unresolved for weeks because no single team member has the full picture in one place.

- Manual AP portal uploads and invoice status blind spots: Customer procurement portals require individually formatted invoice submissions. Rejection notifications often arrive late, leaving the AR team unaware of delivery failures until the account surfaces on the aging report – by which point payment is already delayed.

- ERP data entry errors and fragmented order workflows: Manual posting from mixed-format sources – lockboxes, email remittances, EDI, portals – introduces keying errors and inconsistent coding that creates audit risk and downstream reconciliation overhead every close cycle.

- Slow collections follow-up and poor cash flow visibility: Without a consolidated view of payment status, dispute state, portal approvals, and aging across accounts, collectors cannot prioritise outreach effectively. Follow-up effort distributes evenly across the ledger rather than concentrating on accounts where action has the highest yield.

Why Traditional Approaches Fall Short

Manual AR processes do not fail because AR professionals are under-qualified. They fail because the volume and variability of incoming data exceeds what human teams can process consistently at scale.

- Standard ERP matching requires clean reference data it rarely receives: When invoice references are missing, ambiguous, or split across sources, the ERP cannot match – creating a growing manual queue that compounds with every payment run.

- Rule-based bots break on real-world variability: Robotic Process Automation (RPA)Software that automates repetitive, rule-based digital tasks by mimicking user interactions with applications – effective for stable, structured processes but fragile when inputs vary works when inputs are structured and consistent. In O2C environments, remittance formats, portal layouts, and payment references vary constantly across customers – causing bots to fail silently or require continuous maintenance to remain functional.

- Spreadsheet-based exception tracking creates disconnected data silos: Teams often manage deductions, disputes, and collections follow-up in separate spreadsheets with no connection to live ERP data. This fragments visibility and makes it impossible to see the complete picture of any one account at any given moment.

- Manual collections lacks any prioritisation intelligence: Without a model ranking accounts by payment risk, dispute status, and promise-to-pay history, collectors work the same calling list regardless of which accounts need attention most urgently – spreading effort thinly rather than concentrating it where it moves cash.

- AI vs manual order-to-cash – the real difference: The fundamental gap is not speed – it is pattern recognition applied consistently across every transaction simultaneously. A manual team applies its best judgment case by case. An order to cash workflow automation system applies consistent matching logic across thousands of transactions while escalating only the cases that genuinely require human review.

2. What Is Order to Cash Automation – and What Problem Does It Actually Solve?

Order to Cash automation coordinates every stage of the receivables cycle – from invoice delivery through payment capture, matching, collections, and ERP posting – through a single intelligent platform.

It sits above the existing Enterprise Resource Planning (ERP)Core business software that manages financial transactions, accounting records, and operational data – the system of record for all posted financial activity system rather than replacing it. The ERP remains the system of record for all financial transactions. The O2C automation layer handles the upstream intelligence work: capturing remittances from every source, resolving payer identity, scoring match candidates, routing exceptions, and assembling deduction context – then feeding verified posting proposals back to the ERP.

This architecture matters because finance teams require a clear accountability boundary. The automation layer owns the matching and enrichment work. The ERP owns the accounting record. Human reviewers own the judgment calls where confidence is insufficient or commercial context is required. That division of responsibility is what makes an end-to-end order to cash automation solution credible in a regulated, audit-sensitive environment – and what distinguishes it from tools that claim full autonomy without the guardrails to support it.

Vision and Objectives

- Maximise straight-through processing for clean cases: For payments where reference data is complete and the match is unambiguous, process from payment receipt to ERP posting proposal without any human touch – freeing analyst capacity for work that actually requires judgment.

- Centralise exception handling for complex cases: For short-pays, disputes, deductions, missing remittances, and ambiguous references, route cases to the right queue with relevant context already assembled. Analysts resolve – they do not investigate from a blank screen.

- Improve real-time cash flow visibility: Give treasury, AR management, and finance leadership a consolidated view of unapplied cash, dispute status, portal approval state, and expected payment timing – not a report generated the following morning.

- Accelerate deductions and dispute resolution: Surface deduction reason codes, claim documentation, and customer history automatically so deductions teams respond faster with better-supported positions. Effective order to cash dispute management software starts here.

- Reduce DSO through intelligent collections prioritisation: Rank collector activity by payment risk, aging bucket, dispute state, and payment behaviour so follow-up effort concentrates where it has the highest probability of accelerating cash collection.

- Maintain full audit traceability: Log every automated action, confidence score, and human decision immutably – supporting internal audit, SOX compliance, and the ability to defend posting decisions under customer dispute or regulatory review.

3. What Does Order to Cash Automation Look Like Across Different Industries?

Order to Cash automation adapts to different industries but always follows the same core pattern: automate predictable work, surface complexity early, and resolve exceptions faster.

Manufacturing and CPG: Managing High-Volume Retail Deductions

Your largest retail accounts pay short every month with minimal remittance context. Your deductions team manually reconciles the difference across dozens of line items and multiple portals – and the backlog grows every cycle because new deductions arrive faster than old ones get resolved.

Manual processes fail here because deduction reason codes, supporting documents, and remittance details arrive through three separate channels with no connection to each other. Analysts spend their hours hunting, not resolving. An order to cash workflow automation system changes the inputs available at the point of review. It captures remittances from email and portals, extracts deduction codes automatically, links supporting documents to the relevant open invoice, and routes each case to the deductions queue with context already assembled.

The measurable outcome is shorter deduction cycle times and higher recovery rates – because the team resolves more cases per analyst per week when the investigation work is already complete.

SaaS and Technology: Closing the Month Without an Unapplied Cash Queue

Your subscription billing produces thousands of invoices each month. At month-end, the cash application report still shows a growing queue of unmatched payments that stretches the close timeline by two or three days.

The problem is scale combined with reference variability. Customers pay through multiple channels – bank transfer, card, ACH – and their payment descriptions often lack invoice numbers or use internal reference codes that do not align with the ERP’s format. Standard cash application automation software handles straightforward cases reliably. The difficulty is structural: according to the National Automated Clearing House Association, 71% of remittance information associated with electronic payments travels separately from the actual payment – meaning the data needed to complete a match routinely arrives after the payment itself, through a different channel entirely.

An AI-powered O2C layer applies machine learning (ML)A branch of AI where systems learn patterns from historical data to make predictions or scoring decisions – improving over time as more examples are processed to rank match candidates using amount, date proximity, customer payment history, and reference patterns. High-confidence matches process straight through. Ambiguous cases surface in a review queue with ranked suggestions and supporting evidence. The backlog that previously extended month-end close reduces to a manageable daily exception queue.

Wholesale Distribution: Navigating Portal-Heavy Procurement and Invoice Rejections

Your biggest wholesale customers submit through procurement portals, and invoice rejections arrive with error codes instead of explanations. Your team finds out days after the fact.

Portal-heavy procurement creates a specific operational problem: each customer portal uses different submission rules, validation logic, and escalation paths. A rejected invoice at portal stage means delayed payment – but without real-time status visibility, the AR team cannot act until the aging report flags it. By that point, payment is already 15 to 30 days late for an entirely correctable reason.

An ERP-integrated order to cash automation layer monitors portal submission status continuously. It surfaces rejection events in real time, extracts the error context, and routes the correction task to the right team member with invoice details already attached. Invoices that previously aged through oversight get resolved the same business day. Cash flow timing improves not because customers pay faster but because the AR team eliminates the avoidable delays on its own side of the process.

Ready to explore what this solution looks like for your organisation?

Talk to Our AI Team4. How Does an Order to Cash Automation System Actually Work?

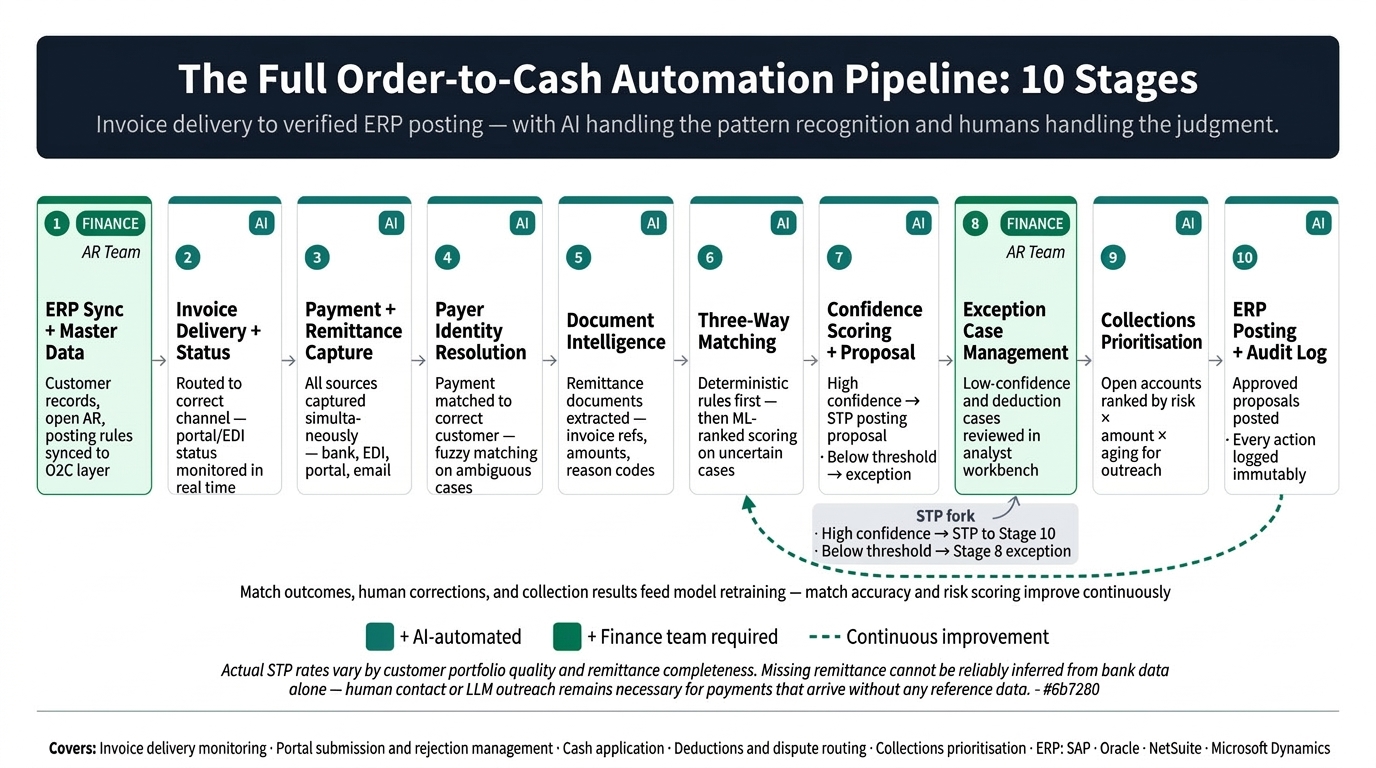

An Order to Cash automation system moves data through a sequence of connected layers – from payment capture through to ERP posting proposal – with human oversight built in at every point where confidence is insufficient or accounting risk is elevated.

A common pattern across real implementations of this solution is that the first measurable win comes not from AI matching logic but from centralised remittance capture. Bringing bank data, email attachments, portal extracts, and lockbox files into one structured environment reduces the time analysts spend hunting for payment context – before any machine learning model makes its first recommendation. That infrastructure improvement alone changes the daily experience of the AR team.

Data Acquisition: Where the Information Comes From

The system connects to the ERP to receive customer master data, open AR balances, invoice details, payment terms, credit limits, deduction history, and posting rules. Payment signals arrive from bank statement files, lockbox feeds, ACH and wire notifications, card gateway transactions, and treasury management systems. Remittance advice – the data linking payments to specific invoices – comes from email inboxes, PDF attachments, spreadsheets, Electronic Data Interchange (EDI)A standardised electronic format for exchanging business documents such as invoices, purchase orders, and remittance data between organisations – commonly used in retail and manufacturing supply chains messages, AP portals, and scanned documents processed through document capture. Invoice delivery status comes from portal submission logs, email delivery confirmations, and EDI acknowledgement files.

The AI Processing Pipeline

- ERP Sync and Master Data Integration. First, the platform establishes a continuous or scheduled sync with the ERP. Customer master records, open invoices, payment terms, deduction history, and posting rules flow into the platform’s canonical data model. This master data forms the reference universe against which all incoming payment activity is matched.

- Invoice Delivery and Status Capture. Next, the platform routes outbound invoices through the correct delivery channel for each customer – email, EDI, AP portal submission, or direct API. It captures delivery status events – received, rejected, approved, disputed, scheduled for payment – storing each against the invoice record for real-time visibility.

- Multi-Source Payment and Remittance Capture. The system ingests payment signals and remittance advice simultaneously from all configured sources. Bank files, lockbox extracts, ACH notifications, and portal payment confirmations create payment records. Email inboxes, PDF attachments, spreadsheets, and EDI remittance messages create corresponding remittance records – each timestamped and linked to its source channel for audit traceability.

- Payer Identity Resolution. Once payment records are created, a payer resolution layer attempts to identify the paying entity. It first applies deterministic matching using bank account numbers, customer identifiers, and known payment references. For ambiguous cases, it applies fuzzy matching against customer aliases, historical payment patterns, and bank metadata to determine which customer account the payment belongs to.

- Document Intelligence Extraction. A document AIAI technology combining optical character recognition and machine learning to extract structured data from unstructured documents such as PDFs, spreadsheets, and scanned forms pipeline processes each remittance document to extract invoice numbers, PO references, dates, payment amounts, reason codes, deduction references, line-item details, and customer notes. Extraction models improve over time as the system learns each customer’s typical document structure and formatting patterns.

- Three-Way Matching Engine. The matching engine links the incoming payment to its remittance and to the correct open AR items in the ERP. It applies deterministic rules first – exact amount and reference matches. Where deterministic matching fails, it applies heuristic rules and then ML-based match scoringMachine learning models that assign a probability score to candidate payment-to-invoice match pairs based on amount, date, reference string, and historical customer payment behaviour to rank candidate matches by confidence.

- Confidence Scoring and Posting Proposal Generation. Every match candidate receives a confidence score reflecting the quality of the supporting evidence. High-confidence matches that meet configured policy thresholds generate automatic posting proposals delivered to the ERP. Matches below the threshold – or those involving short-pays, unusual deductions, or missing remittances – route to the exception queue instead of generating automatic proposals.

- Exception Routing and Case Management. The system opens a structured case for each low-confidence or policy-flagged item. Each case routes to the appropriate queue – cash application, deductions, collections, or customer service – based on reason, customer tier, amount, and business unit. The analyst reviewing the case sees the full customer context, payment evidence, remittance content, portal status, and a recommended next action – assembled before the case lands in the queue.

- Collections Prioritisation Engine. In parallel, a collections model ranks open accounts by risk, aging bucket, dispute status, portal approval state, promise-to-pay history, and payment behaviour patterns. Collectors see a prioritised worklist rather than a raw aging report – with the account context needed to engage each customer productively.

- ERP Posting and Audit Logging. Approved posting proposals – whether system-generated on high-confidence matches or human-reviewed on exceptions – flow back to the ERP as structured posting instructions. Every action, confidence score, human decision, and system recommendation writes to an immutable audit log supporting internal controls, SOX compliance, and customer dispute defence.

Human-in-the-Loop: Where Human Judgment Still Matters

Responsible O2C automation defines clearly what the system handles autonomously and what it escalates for human review. The goal is to eliminate human touches on predictable, mechanical work – not to remove human judgment from decisions with real financial or commercial consequences.

- Low-confidence matches always require human review: When match scoring falls below the configured policy threshold, the system does not generate a posting proposal. The analyst reviews the evidence, sees ranked match suggestions, and makes the final posting decision.

- Short-pays and deductions require human authorisation: A deduction or short-pay involves a commercial decision – accept, dispute, or escalate. The system surfaces the relevant evidence and suggests a course of action, but the decision to accept a deduction or raise a formal dispute belongs to the reviewer with commercial authority.

- High-value transactions trigger additional review gates: Configurable amount thresholds and customer tier rules require human sign-off on posting proposals above certain values – regardless of how high the confidence score is. Amount-based controls reflect accounting risk, not model uncertainty.

- Disputed invoices stay with the human team: Invoice disputes involving pricing differences, delivery discrepancies, or contractual interpretation require direct customer communication and commercial judgment. The system provides context and history; resolution remains a human responsibility throughout.

- Model outputs require periodic human validation: Matching logic, reason-code classification, and collections ranking models should undergo regular review by operations leads. Human corrections feed back into model improvement through structured feedback loops – with changes going through evaluation before altering live behaviour.

Output and Interaction: What the User Actually Sees

AR analysts work in a unified analyst workbench. For each exception case, they see the customer account timeline, open invoice list, payment evidence, remittance text, portal status, dispute history, and a ranked list of suggested actions. Analysts do not leave the workspace to consult the ERP, email inbox, or portal separately – the relevant context is already assembled.

Collections teams see a prioritised daily worklist ranked by urgency, with account summaries, communication history, and suggested contact scripts ready for review. Finance leaders access a real-time dashboard covering unapplied cash volume, exception queue status, DSO trends, deduction aging, and cash flow forecast inputs. Every view connects to the same underlying data – eliminating the reporting lag that spreadsheet-based operations create at every close.

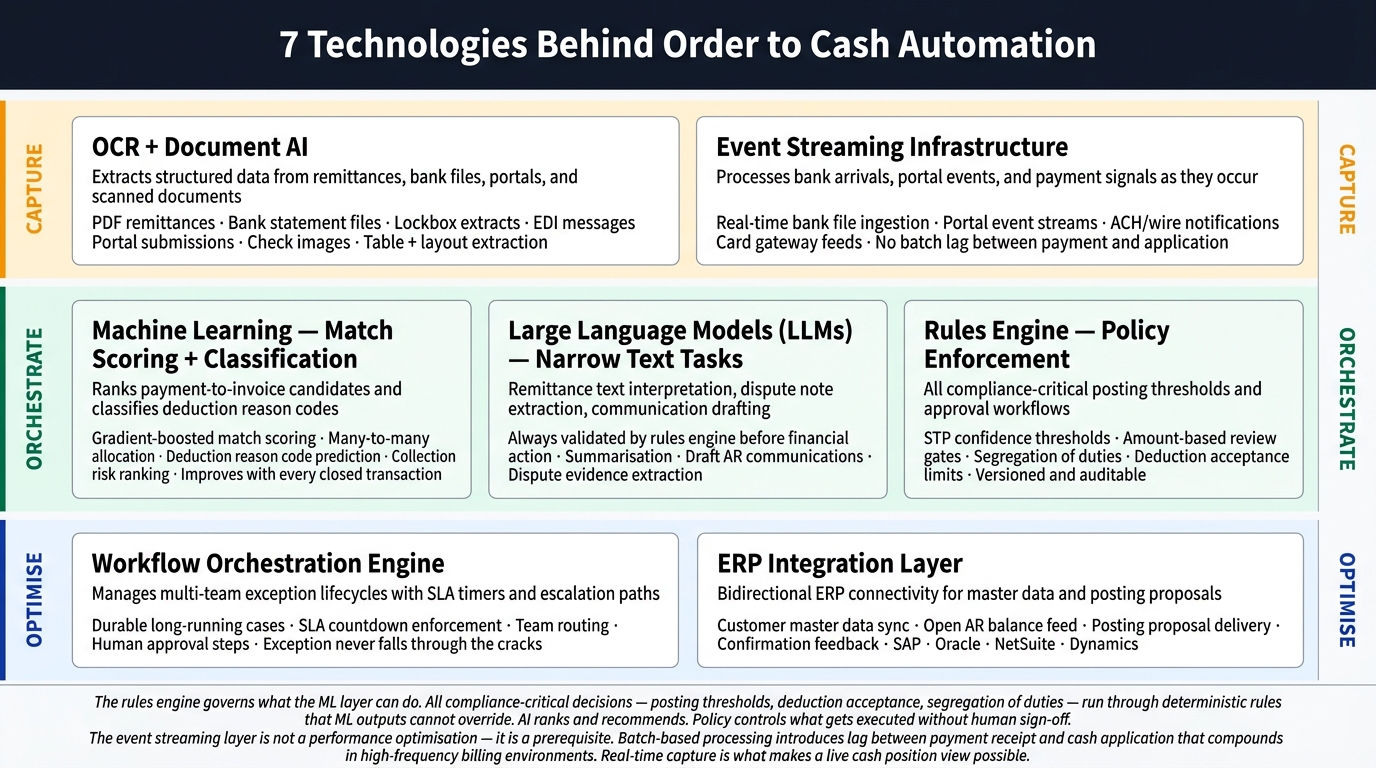

5. What Technologies Power an Order to Cash Automation Solution?

An Order to Cash automation software stack combines several distinct technology disciplines. No single capability delivers the full solution – the value comes from how these layers integrate and reinforce each other across the full receivables workflow.

- Optical Character Recognition (OCR)Technology that converts images of printed or handwritten text – including scanned documents and PDFs – into machine-readable text data, enabling downstream extraction and processing and document AI: Extracts structured data from PDFs, scanned remittances, check images, and portal-exported documents. Modern document AI combines OCR with layout understanding and table extraction – enabling reliable data capture from the semi-structured formats that pure text parsing cannot handle consistently.

- Machine learning for match scoring and classification: Gradient-boosted models and neural networks trained on historical transaction data assign probability scores to payment-to-invoice match candidates. These models also classify deduction reason codes, predict collection risk, and route exceptions by category – each with confidence scores that control the boundary between automated and human-reviewed decisions.

- Large Language Models (LLMs)AI models trained on large text datasets capable of understanding and generating human language – valuable for summarisation, note extraction, and draft communications in narrow, controlled applications for narrow text tasks: LLMs contribute usefully to email summarisation, dispute note extraction, draft customer communications, and remittance text interpretation. They are not used as autonomous decision-makers in financial posting workflows, because their outputs require deterministic validation before any accounting action occurs.

- Rules engine for policy enforcement: All compliance-critical decisions – posting thresholds, deduction acceptance limits, segregation of duties, and approval workflows – run through a deterministic rules engine. Configurable business policy always governs what the AI layer can and cannot do without human sign-off, preserving accounting controls regardless of model confidence.

- Workflow orchestrationSoftware infrastructure that manages and coordinates long-running business processes – ensuring each step executes in the correct sequence with proper state management, SLA tracking, and error handling for long-running processes: O2C exceptions often span days or weeks across multiple teams. A workflow orchestration layer manages state, SLA timers, escalation paths, and task assignments across the full exception lifecycle – ensuring no case falls through the cracks between teams.

- ERP integration layer: Bidirectional ERP connectivity – via APIs, flat file exchange, or integration middleware – keeps customer master data, open AR, and posting status in sync between systems. An ERP-integrated order to cash automation system augments existing ERP infrastructure rather than replacing it, protecting prior investment while adding intelligence above it.

- Event streaming infrastructureData infrastructure that processes continuous streams of business events in near real time – enabling immediate response to payment arrivals, portal status changes, and remittance signals without overnight batch delays for real-time processing: High-volume payment environments require infrastructure that processes bank file arrivals, portal events, and payment signals as they occur. Batch-based processing introduces lag between payment receipt and cash application that compounds in high-frequency billing environments.

6. What Results Does Order to Cash Automation Deliver for Finance Teams?

Order to Cash automation delivers measurable results at the process level – faster matching, shorter DSO, fewer write-offs, and better visibility – well before the impact appears in board-level financial reporting.

- Reduction in manual cash application effort: For payments where reference data is sufficient and matching is unambiguous, the system processes end-to-end without analyst involvement. Teams that previously dedicated significant daily hours to cash matching shift that capacity to higher-value exception work and direct customer engagement. This is the core outcome of effective cash application automation software.

- Faster Days Sales Outstanding: Centralised remittance capture and automated matching reduce the time between payment receipt and correct ERP posting. Orders release faster for customers with cleared payment status. DSO improvement directly reflects the reduction in lag across the AR process – from invoice delivery through to final posting.

- Shorter deduction and dispute cycle times: Automatically extracting deduction codes, linking supporting documents, and assembling customer context before the analyst sees the case removes the investigation phase entirely. Deductions teams spend time resolving cases rather than researching them. This is the core value proposition of order to cash dispute management software applied in a real production environment.

- Improved cash flow visibility for treasury and finance leadership: Real-time dashboards showing unapplied cash, exception queue status, portal approval states, and expected payment timing give treasury the data needed to manage short-term liquidity with greater accuracy. The lag between cash reality and reporting visibility shrinks from days to minutes.

- Reduced ERP posting errors: Automated posting proposals built on verified match evidence and structured data extraction carry fewer keying errors than manual entry from mixed-format sources. Posting quality improves alongside processing speed – reducing reconciliation overhead at every close.

- More effective collections through intelligent prioritisation: Collectors contact the right accounts at the right time because the system ranks outreach priority by payment risk, dispute status, and aging – not by invoice date alone. Follow-up effort concentrates where it has the highest probability of accelerating payment rather than distributing evenly across a raw aging list.

- Improved invoice acceptance rates through portal monitoring: Monitoring portal submission status and surfacing rejection reasons in real time reduces the number of invoices that age due to correctable submission errors. For businesses with significant portal-based customers, this improvement in first-pass acceptance rates has direct and measurable order to cash cash flow automation impact.

- Reduced write-off risk on unresolved deductions: Deductions that are never properly researched age into write-offs by default. An invoice-to-cash automation software approach that surfaces deduction cases promptly with assembled supporting data increases the proportion that teams actively dispute, negotiate, or recover – rather than quietly absorbing.

7. How Do You Build the Business Case for Order to Cash Automation?

Order to Cash automation ROI comes from reduced manual processing hours, lower Days Sales Outstanding, and fewer write-offs from unresolved disputes and deductions.

Teams that have worked through this integration consistently find that the business case anchors fastest on two metrics: DSO reduction and cash application labour cost. Both are measurable before deployment, carry clear post-implementation targets, and translate directly into working capital and efficiency numbers that CFOs and controllers recognise without translation. The challenge is building a credible before-and-after measurement framework rather than relying on industry benchmark claims that may not reflect the organisation’s specific portfolio mix.

The following metrics anchor the strongest business cases for an order to cash automation enterprise system evaluation:

- Cash application labour hours per transaction: Track the average analyst time required to match and post a payment today – including exception investigation time, not just the posting action itself. Post-implementation, compare against the same metric for human-reviewed cases and calculate the reduction in total team hours at equivalent payment volume.

- Days Sales Outstanding: Establish a 90-day rolling baseline before deployment. Measure DSO change at 90, 180, and 365 days post-deployment. To frame the opportunity: The Hackett Group’s 2025 Working Capital Survey found that accounts receivable now represents the largest component of excess working capital among the top 1,000 U.S. public companies – a $600 billion opportunity driven by an 18-day DSO gap between median and top-quartile performers. Closing even a portion of that gap through faster matching and collections has direct and measurable working capital impact.

- Deduction recovery rate: Measure the percentage of short-pays that the deductions team actively disputes versus writes off without investigation. A faster deduction pipeline with better-assembled evidence typically improves dispute win rates and reduces the proportion resolved through default write-off rather than active recovery.

- Invoice acceptance rate through AP portals: For businesses with significant portal-based customers, track the percentage of invoices accepted on first submission. Rejection correction cycles add 15 to 45 days to payment timing in many cases. Reducing rejections has direct and measurable cash flow timing impact independent of any change in customer payment behaviour.

- Exception-to-resolution cycle time: Measure from when an exception case opens to when it resolves and posts. This metric reflects the quality of the analyst workbench and exception routing – capturing the operational value of the platform beyond headline automation rate figures.

A realistic implementation timeline for a mid-size organisation is four to six months from contract to initial production. The first measurable business impact – in cash application volumes and exception queue size – typically appears within 60 to 90 days. Full deductions and collections capabilities usually reach operational maturity at the six to twelve month mark, because those workflows require customer-specific configuration and process change management alongside the technology deployment.

The business case for acting now rather than waiting rests on a specific and quantifiable reality: every quarter of delay is another quarter of DSO premium, deduction write-offs, and AR labour cost that the organisation continues to carry while competitors who have already deployed reduce theirs.

8. What Does Implementing Order to Cash Automation Actually Require?

Successful Order to Cash automation requires clean ERP master data, reliable remittance source connectivity, and a phased rollout that builds confidence before expanding automation thresholds progressively.

What implementation experience reveals that theoretical explanations often miss is the underestimated complexity of customer-specific exception logic. Each major account brings its own deduction codes, portal submission rules, short-pay tolerance policies, and dispute escalation paths. Configuring these correctly requires close collaboration between the implementation team, AR management, and key account contacts. Technology readiness matters – but operational readiness often determines whether a project achieves its target automation rate or plateaus at a much lower level.

- Master data quality is a prerequisite, not a deliverable: The matching engine’s accuracy depends entirely on the quality of ERP customer master records, open AR data, and invoice detail. Duplicate customer records, inconsistent naming conventions, and stale payment terms create matching failures that model tuning cannot compensate for. Data remediation before deployment is not optional.

- Remittance source coverage requires upfront integration effort: The platform’s value depends on how many of the organisation’s payment channels it actually covers. Incomplete coverage – missing a major customer’s portal or an important bank format – leaves exceptions in exactly the manual channels the deployment was meant to eliminate. Source coverage planning is a critical pre-deployment activity.

- ERP integration complexity varies significantly by system: Connecting to a modern cloud ERP via API is relatively straightforward. Legacy on-premise systems with limited API support require middleware, flat file exchange, or custom connectors – adding time and implementation cost. Enterprise AI development teams with ERP integration depth reduce this risk considerably compared to finance software vendors working outside their technical core.

- Confidence thresholds require tuning before full automation: Deploying at full automation on day one is an unnecessary risk. The standard responsible practice is a phased approach: begin with human review of all posting proposals, then expand automation progressively as confidence in the matching logic builds against the live data environment.

- Portal automation requires ongoing maintenance, not a one-time build: Customer AP portal layouts, submission requirements, and authentication rules change regularly. Portal integrations built at deployment drift out of sync over months as buyers update their systems. Organisations should budget for ongoing portal monitoring and maintenance as a recurring operational cost rather than a one-time project item.

- Compliance and data privacy obligations apply throughout: O2C platforms process customer financial data and banking information at scale. GDPR, data residency requirements, SOX internal controls, and segregation-of-duties rules govern every aspect of the platform’s operation. For organisations with strict data sovereignty requirements, private LLM development and on-premise deployment options deserve careful evaluation alongside cloud-based alternatives.

- Model outputs require continuous monitoring post-deployment: AI models trained on historical data can degrade when customer payment behaviour changes, new accounts join the portfolio, or ERP field structures change. Continuous monitoring of match rates, exception volumes, and human correction patterns is part of operating the platform correctly – not a post-implementation afterthought that gets deferred.

Where This Solution Has Real Limits

An honest assessment of any Order to Cash automation solution includes acknowledging where the technology has genuine boundaries. These limits do not prevent successful deployment – but they need to be scoped correctly at the outset.

- Missing remittance cannot be reliably inferred: When a customer pays without any remittance advice – no email, no portal attachment, no EDI file – the system cannot determine intended application from bank data alone. A human must contact the customer or make a judgment call. No current technology reliably constructs missing business context from partial evidence.

- Deductions often require commercial context that lives outside the system: Many deductions reflect customer pricing disputes, promotional claims, or contract interpretation differences. Resolving them requires communication with sales, customer success, or the customer directly – not data extraction alone. The system provides evidence and history; resolution remains a human commercial responsibility in most cases.

- LLM-based text interpretation requires deterministic guardrails: Using large language models to interpret remittance text or draft dispute communications adds value – but LLMs can misinterpret ambiguous language or produce plausible-sounding but incorrect extractions. Every LLM output in a financial workflow should go through deterministic validation or human review before the system acts on it.

- Real-world automation rates vary significantly by portfolio: Headline straight-through processing rates often reflect clean-data pilot environments. Actual automation rates in production depend heavily on remittance data quality, portal coverage completeness, and ERP master data accuracy across the live customer base. A realistic expectation for a mixed enterprise portfolio is high automation on the clean portion and structured exception handling on the rest – not uniformly high automation across all transaction types.

9. Which Organisations Benefit Most from an Order to Cash Automation Solution?

Order to Cash automation delivers highest value where invoice volumes are high, customer payment behaviour is variable, and the gap between payment receipt and correct ERP posting has measurable working capital consequences.

The primary decision-makers who champion these deployments are CFOs, controllers, VP Finance, and AR directors in mid-market and enterprise organisations. Daily users are cash application specialists, collections analysts, deductions managers, and shared services leads. Both groups benefit – one from the working capital and visibility outcomes, the other from the reduction in manual, repetitive processing work that currently consumes their capacity.

This solution is particularly valuable if:

- Your organisation processes hundreds or thousands of B2B payments per month across multiple channels and customer segments with varying remittance practices

- Your deductions and dispute backlog grows faster than your team can clear it each billing cycle

- Your AR team dedicates significant hours each week to investigating missing remittances or correcting ERP posting errors rather than resolving customer issues

- Your collections team works from a raw aging report without intelligent prioritisation, spreading follow-up effort evenly rather than concentrating it where it moves cash

Industries with strong fit include manufacturing, consumer goods, wholesale distribution, business services, SaaS and technology, healthcare distribution, and any sector where large retail or enterprise customers pay through AP portals with complex deduction and compliance requirements. For these environments, off-the-shelf ERP tools handle the clean cases but leave the 20 to 40 percent of complex transactions – the short-pays, portal rejections, and multi-invoice allocations – as entirely manual work.

A dedicated order to cash automation system built for this complexity handles that variability through configured rules and AI scoring rather than analyst effort. Organisations evaluating invoice-to-cash automation software should specifically assess how each solution handles exceptions and portal coverage – not just the automation rate on the easy cases. The value of an order to cash automation enterprise system shows most clearly in how it manages the complex transactions – the short-pays, deduction disputes, portal rejections, and multi-invoice allocations – not how efficiently it processes the ones that would have resolved themselves anyway.

10. Frequently Asked Questions About Order to Cash Automation

The most common questions about Order to Cash automation centre on three areas: automation scope, ERP integration requirements, and where human oversight still applies.

How does order to cash automation reduce manual cash application work?

Order to Cash automation reduces manual cash application by handling straight-through processing for payments where reference data is complete and the match is unambiguous. The system ingests remittance data from every source – email, bank files, portals, EDI – extracts invoice references automatically, and generates posting proposals for high-confidence matches without requiring analyst involvement. Analysts only see the exceptions: low-confidence matches, short-pays, and missing remittances that genuinely require human judgment. In practice, the team’s time shifts from mechanical matching to resolving the cases where their knowledge of the customer relationship and commercial context actually makes a difference.

What is the best order to cash automation software for ERP integration?

The best order to cash automation software for ERP integration connects to your specific ERP via a stable, bidirectional integration – not just a one-way data export. Key requirements include near-real-time sync of customer master data, open AR, and invoice status, plus structured posting proposal delivery back to the ERP without requiring manual rekeying. Modern cloud ERPs typically support API-based integration. Legacy on-premise systems may require middleware or flat file exchange. The integration architecture matters as much as the matching logic – a platform that performs well in isolation but posts incorrectly to the ERP creates more reconciliation problems than it solves.

What does an end-to-end order to cash automation solution actually include?

An end-to-end order to cash automation solution covers the full receivables cycle: invoice delivery and status tracking, multi-source payment and remittance capture, payer identity resolution, three-way matching, exception routing, deductions management, collections prioritisation, and ERP posting. End-to-end means the platform connects all of these stages rather than automating just one segment. A cash application point solution that ignores collections and deductions handles only a portion of the total problem. For enterprises with complex portfolios, an integrated approach reduces the overhead of managing multiple disconnected tools while providing a single visibility layer across all AR activity.

How does order to cash automation handle deductions and dispute resolution?

Order to Cash automation for deductions and dispute resolution works by assembling the relevant evidence before the analyst sees the case. The system extracts deduction reason codes from remittance documents, links supporting claims to the relevant invoices, retrieves the customer’s deduction history, and routes the case to the deductions queue with context already attached. The analyst resolves rather than investigates. For formal disputes, the system suggests likely reason codes and can draft initial dispute communications for review. However, the commercial decision – whether to accept, dispute, or escalate a deduction – remains with the human team, because it often involves factors outside any system’s data, such as sales relationship context or contract interpretation.

How does AI-powered order to cash automation improve payment reconciliation?

AI-powered order to cash automation improves payment reconciliation by applying machine learning to match payments to invoices even when reference data is incomplete or inconsistent. Traditional ERP cash application requires exact or near-exact reference matches. ML-based match scoring considers amount proximity, date patterns, customer payment history, partial reference strings, and payer behaviour to rank candidate matches by confidence – handling the ambiguous cases that ERP rules cannot resolve. The result is a higher proportion of payments matched correctly on first pass, a smaller exception queue, and faster reconciliation timelines. Confidence scoring also ensures that uncertain matches route to human review rather than posting incorrectly – maintaining accounting accuracy alongside speed.

Build This Solution With Softlabs Group

Softlabs Group builds custom AI development solutions for finance operations – including end-to-end Order to Cash automation systems tailored to your specific ERP, customer portfolio, payment channels, and exception handling requirements. Every system we build connects to your actual data sources, reflects your deduction policies and portal integrations, and includes the confidence controls and immutable audit logging that regulated finance environments require. We do not implement off-the-shelf platforms and apply general settings – we engineer against the specific workflow reality your AR and collections teams live with daily.

If your organisation processes significant B2B payment volumes and your AR team spends capacity on work that a well-designed system should handle, the conversation starts with understanding your current workflow – not with a product demo. Our team maps your data sources, exception patterns, and ERP integration requirements before recommending an architecture. That scoping work is what separates a system that delivers its target automation rate in production from one that performs in a pilot and disappoints at scale.