Executive Summary: The Reading Problem Behind Every Slow Claims Department

Your claims department has a reading problem, not a judgment problem. An LLM insurance claims solution targets the exact bottleneck: the hours each adjuster spends manually reading documents before reaching a single coverage decision. Every incoming file arrives as a mass of unstructured data – scanned forms, hospital bills, repair estimates, and 120-page policy documents that no one has time to cross-reference under a growing caseload. Your most experienced adjusters now carry 150 to 200 open files, spending the majority of their working day on pre-work rather than judgment.

Modern AI reads every document, identifies relevant policy clauses, flags early fraud signals, and delivers a structured one-page brief to the adjuster in minutes. What currently takes two hours of manual pre-reading drops to a focused fifteen-minute review. At portfolio scale, that shift compounds into faster settlements, lower operating costs, and a customer experience that retains claimants rather than driving them to competitors. This is what a well-designed LLM insurance claims solution actually delivers – and why claims operations leaders are moving from cautious pilots to full-programme deployment.

1. Why Is Insurance Claims Processing Getting Harder to Scale Without AI?

Insurance claims operations face a compound pressure: rising claim volumes, a shrinking pool of experienced adjusters, and customer expectations that manual workflows simply cannot meet.

The Operational Reality Inside a Claims Department

Insurance carriers and third-party administrators process thousands of claims daily, each arriving as an unstructured bundle of documents. The claims lifecycle runs from First Notice of Loss (FNOL)The initial report filed by a policyholder notifying an insurer that a covered incident has occurred – the trigger that starts the claims process through triage, coverage verification, damage assessment, fraud review, reserve setting, and final settlement. Every step requires a human to read, interpret, and act on information spread across multiple sources and systems. As claim volumes grow with market expansion, extreme weather events, and regulatory complexity, the operational gap between demand and capacity widens consistently.

In practice, organisations deploying AI claims assistance typically encounter the same upstream problem: the workflow was never designed around the bottleneck. Accenture research across 120 claims executives and 900 underwriters found that up to 40% of underwriters’ time goes to non-core administrative activities – a figure that captures the bottleneck precisely. Manual claims processing treats every file as a blank page, regardless of whether the claim is a straightforward fender repair or a complex liability dispute. An adjuster opening a 40-file batch on a Monday morning faces the identical task for each one – read every document from scratch, locate the relevant policy section, check for fraud indicators, and form a judgment. Nothing in a traditional claims management system helps with that pre-work.

Key Pain Points This AI Solution Addresses

- Claims processing too slow, causing customer dissatisfaction and increasing carrier-switching rates among claimants who experience poor communication and extended timelines

- Adjusters overwhelmed with too many open claims, spending the majority of each working day on document reading rather than the coverage decisions their expertise is actually needed for

- Claims fraud going undetected until it is too late, because volume pressure prevents thorough cross-referencing of claim narratives against claimant history and prior submissions

- Manual document review delaying claim settlements by days or weeks on straightforward cases where the coverage determination is not genuinely complex

- Inconsistent claim reserve setting across the team, driven by individual interpretation without a shared information baseline, leading to reserve inadequacy and late adjustments

- High cost of claims operations with growing volumes, as headcount scales linearly with volume in a manual workflow but revenue does not

- Too many simple claims consuming unnecessary manual work, leaving complex, high-value cases under-resourced because adjuster capacity is distributed without regard to claim complexity

Why Manual and Legacy Claims Processing Falls Short

The contrast between manual and AI-assisted claims processing is not primarily one of speed – it is one of information quality at the point of decision. A human adjuster manually reading a 40-page demand package builds a mental model of the claim incrementally, often missing inconsistencies between documents reviewed at different times. An AI processes the full document set simultaneously, cross-referencing every claim detail against every other document in the file before surfacing a structured summary.

Legacy claims management systems compound this problem by creating “system hopping” – adjusters moving between disconnected platforms to gather information that should arrive pre-assembled. Coverage verification happens in one system. Claimant history lives in another. Fraud flags, if checked at all, require a separate query. The overhead of this fragmentation is invisible in any single transaction but enormous across thousands of claims per month.

Furthermore, traditional approaches scale linearly with volume. Doubling the claim count requires roughly doubling the adjuster headcount to maintain the same processing speed – a model that becomes economically unsustainable as claims inflation, litigation costs, and catastrophe event frequency all increase simultaneously. An AI insurance claims software layer breaks that linear relationship by absorbing the document-processing workload without proportional staffing cost.

2. What Makes an LLM Insurance Claims Solution Different from Traditional Claims Technology?

An LLM insurance claims solution replaces manual document reading with an AI layer that processes every claim document automatically and delivers structured intelligence to the adjuster before human review begins.

Traditional claims management systems store documents – they track status, route tasks, and maintain records, but they do not read or interpret content. The adjuster still does all of that manually. An LLM insurance claims solution adds an intelligence layer that reads every document in the file, matches claim details against policy language, scores fraud risk, and assembles the relevant information before the adjuster opens the case. The underlying capability is the combination of Large Language Models (LLMs)AI systems trained on vast text datasets that can read, understand, summarise, and reason about unstructured text – including insurance documents, policy language, and claim narratives with domain-specific context retrieval. The AI does not simply search for keywords – it reads documents the way an experienced adjuster would, understanding context, identifying relevant clauses, and recognising inconsistencies across multiple documents simultaneously.

Vision and Objectives

- Reduce per-claim adjuster document review time from hours to minutes, freeing experienced staff for judgment rather than pre-work

- Process FNOL submissions and route claims automatically to the appropriate handling channel based on claim type, complexity, and estimated value

- Identify fraud signals across claim narratives, claimant history, and document inconsistencies before the file reaches an adjuster for review

- Deliver coverage verdicts with cited policy clauses, reducing interpretation errors and producing a consistent, auditable basis for every coverage decision

- Flag high-value and complex claims for specialist handling before resources are misallocated to cases that fall outside standard processing parameters

- Generate plain-English claim summaries that support regulatory explainability requirements for both approvals and denials, reducing grievance exposure

3. How Does This AI Solution Perform Across Different Insurance Contexts?

An insurance claims AI solution applies differently depending on claim type, volume profile, and operational context – but the core benefit is consistent: faster, better-informed adjuster decisions at lower per-claim cost.

Property and Casualty Carrier Managing a Catastrophe Event

When a major storm makes landfall in your coverage area, your FNOL queue does not grow gradually – it floods overnight. Traditional intake processes rely on phone agents manually logging each report into the claims management system, often capturing incomplete or inconsistent data under volume pressure. During peak events, adjusters receive claim batches without any pre-triage, forcing each one to be treated with equal urgency regardless of complexity or estimated loss value.

An AI first notice of loss platform captures structured data from every submission channel automatically – phone transcripts, web forms, and mobile photo uploads. The AI triages each claim within seconds, separating total losses from minor damage claims, and routes files to the appropriate handling team with an initial assessment already prepared. As a result, the highest-complexity files reach specialist adjusters within hours rather than days, and straightforward claims enter processing without manual queue management overhead.

Health TPA Processing High-Volume Reimbursement Claims

Your team opens 800 new health reimbursement claims every Monday morning, and every single one requires a policy match before anyone can act on it. Manual policy cross-referencing is the single largest time cost in health claims processing. Adjusters read claim narratives, locate the relevant policy section, verify sub-limits and exclusions, and make a coverage determination – all before any substantive work begins. At high volume, this pre-work creates a consistent backlog that pushes settlement timelines out by days on cases that are not genuinely complex.

An intelligent claims processing tool for insurance operations handles policy matching automatically using retrieval-augmented generation. The AI retrieves the specific policy clauses relevant to each incoming claim, assesses coverage against the claimed amount, and highlights any exclusion triggers – all before the adjuster sees the file. Adjusters arrive at the coverage decision with evidence already assembled, cutting per-claim review time significantly and allowing each team member to handle a materially higher daily caseload without corresponding accuracy loss.

Auto Insurer Addressing Adjuster Capacity and Burnout

Your most experienced auto claims adjuster manages 200 open files and has not cleared her queue in three months. Auto claims demand adjuster attention across the full lifecycle – from initial FNOL through damage assessment coordination, coverage verification, repair estimate review, and settlement negotiation. Each touchpoint requires the adjuster to re-read the file and rebuild context lost since the last action. The cognitive load compounds with every additional open file, driving the burnout and attrition that compounds the capacity problem further.

AI insurance claims software changes this by maintaining a continuously updated structured summary of every open file. When the adjuster returns to a claim, the AI presents a current status brief – not a document archive. Key pending items, relevant policy flags, and recommended next actions surface immediately, without any manual re-reading. Adjusters reclaim meaningful capacity for judgment and claimant communication.

Ready to explore what this solution looks like for your organisation?

Talk to Our AI Team4. How Does an LLM Insurance Claims Solution Actually Process a Claim?

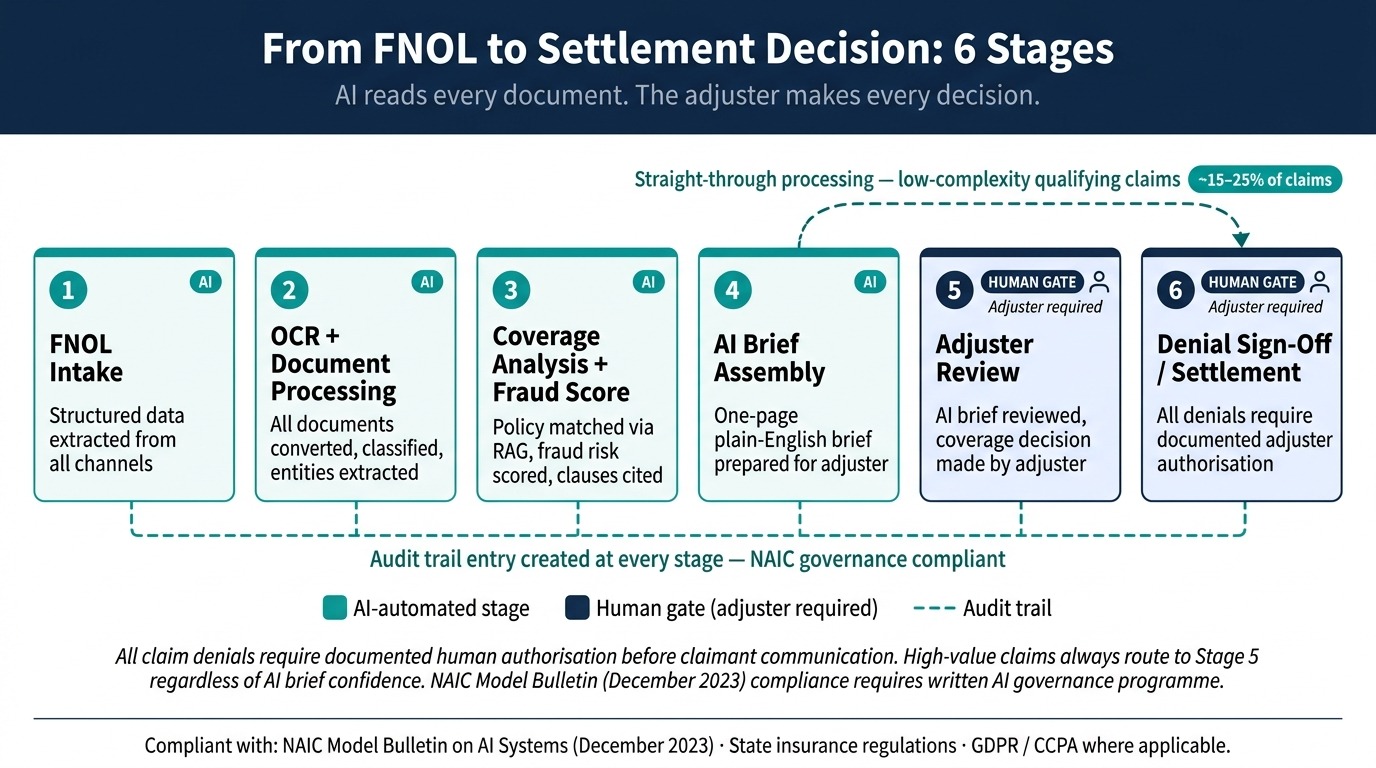

An LLM insurance claims solution runs each incoming claim through a sequential pipeline of specialised AI components, from document extraction through to a structured adjuster brief with a routing decision. The clearest way to understand what this actually does: every adjuster arrives at every file with a junior analyst who has already read everything, matched it against the policy, flagged the fraud signals, and prepared a one-page summary. The adjuster reviews and decides. The AI handled the two hours of pre-reading.

What implementation experience reveals that theoretical explanations often miss is the importance of keeping each stage in the pipeline discrete and auditable. When a claim fails to match expectations, the problem needs to be traceable to a specific pipeline stage – not hidden inside a single monolithic model. The architecture below reflects that principle, with each component handling one defined task and passing structured output to the next.

Data Acquisition: What Enters the System

The pipeline ingests claim data from multiple structured and unstructured sources. Document types include FNOL submission forms, police and incident reports, medical records and hospital bills, repair estimates and damage photographs, the original policy document and any endorsements, and third-party data feeds such as weather records for property events. Each source arrives in a different format – some as typed PDFs, others as handwritten scanned forms, images, or audio transcripts from phone-based FNOL calls. The first challenge the system addresses is converting this heterogeneous input into a consistent, machine-readable format.

The AI Processing Pipeline

- FNOL Intake and Structured Extraction. First, the system receives the claim submission through whichever channel the claimant used – web form, phone call transcript, mobile app upload, or email. Natural Language Processing (NLP)An AI discipline that enables computers to read, interpret, and extract meaning from human language in both written and spoken form extracts core structured fields from the unstructured submission text: claimant identity, incident date and location, reported cause of loss, and initial estimated damage amount. This structured record becomes the seed of the claim file that every subsequent stage appends to.

- OCR and Document Intelligence. Next, Optical Character Recognition (OCR)Technology that converts printed, handwritten, or scanned text from images and documents into machine-readable digital text processes every attached document – transforming scanned forms, hospital bills, repair estimates, and police reports into machine-readable text. The AI then applies document classification to identify what each extracted document is, and entity extraction to pull specific data points such as treatment codes, repair part numbers, and officer identifiers. The system handles documents in multiple languages and varying scan quality, flagging low-confidence extractions for human review rather than silently passing on uncertain data.

- Policy Coverage Analysis via Retrieval-Augmented Generation. Once the claim documents are structured, the pipeline performs coverage analysis. Retrieval-Augmented Generation (RAG)An AI technique that connects a language model to a searchable knowledge base so the model answers questions using retrieved, specific context rather than general training knowledge alone retrieves the relevant sections of the policyholder’s specific coverage document from a vector databaseA specialised database storing documents as mathematical representations, enabling semantic search – finding passages that are conceptually relevant rather than just keyword-matched. The LLM then reasons across the claim facts and the retrieved policy clauses, producing a structured coverage assessment – with the specific policy sections cited by page and clause number. Critically, the AI does not produce a final coverage decision here. It produces an evidence-assembled brief that tells the adjuster exactly which clauses apply, which exclusions are triggered, and where the policy language is genuinely ambiguous – so the adjuster makes the final call with every relevant reference already in front of them rather than having to locate it manually.

- Fraud Signal Detection. The system then runs the claim through a fraud screening layer. Rule-based checks identify common indicators: claims filed within the first weeks of a new policy, submission amounts inconsistent with the reported diagnosis or damage type, duplicate claimant or vehicle identifiers across multiple active claims, and timing inconsistencies between the reported incident and supporting documents. A machine learningA category of AI where algorithms learn patterns from historical data and use those patterns to make predictions on new inputs without being explicitly programmed for each scenario classifier scores each claim on a fraud probability scale based on patterns from historical claims data. High-scoring claims receive a flag with the specific indicators that triggered it.

- AI Claim Brief Generation. At this stage, the pipeline compiles all structured outputs – the coverage verdict, the fraud score with cited indicators, the extracted document summary, and any pending information requests – into a single structured one-page adjuster brief. The brief is written in plain English, not in system codes or policy section references. An adjuster reading the brief understands immediately what the claim involves, whether coverage applies and why, what fraud signals are present if any, and what the recommended next action is.

- Confidence-Gated Routing and Escalation. The system then evaluates whether the claim meets the criteria for straight-through processing or requires human escalation. Claims below a defined value threshold, with clear coverage, low fraud scores, and complete documentation route directly to an expedited settlement channel. Claims above value thresholds, with ambiguous coverage, elevated fraud scores, or incomplete documentation route to a human adjuster – with the AI brief already attached. The routing decision and its basis are logged in full, creating a complete audit trail for every claim regardless of its processing path.

Human-in-the-Loop: Where Human Judgment Still Matters

Human oversight is not an optional add-on in a well-designed LLM claims processing platform – it is a core design requirement. The AI prepares; the human decides. Specific scenarios always route to human review:

- All claim denials require human sign-off before the denial is communicated to the claimant, ensuring regulatory compliance and a defensible decision record

- High-value claims above a defined threshold are always reviewed by a senior adjuster, regardless of how clearly the AI has assessed the coverage and fraud picture

- Complex liability and litigation claims involve legal interpretation that the AI flags but does not attempt to resolve – these route to specialist handlers with the full AI dossier prepared

- Ambiguous coverage situations where the AI confidence score falls below the routing threshold generate an escalation with the specific uncertainty clearly described for the human reviewer

- Personal injury claims always involve human interaction with the claimant, where empathy and communication quality are as important as the technical coverage determination

This agentic AI architecture – where specialised agents handle discrete tasks and escalate intelligently – is what distinguishes a production-ready claims system from a demo. The human adjuster shifts from processor to reviewer, making decisions on AI-prepared information rather than assembling that information themselves.

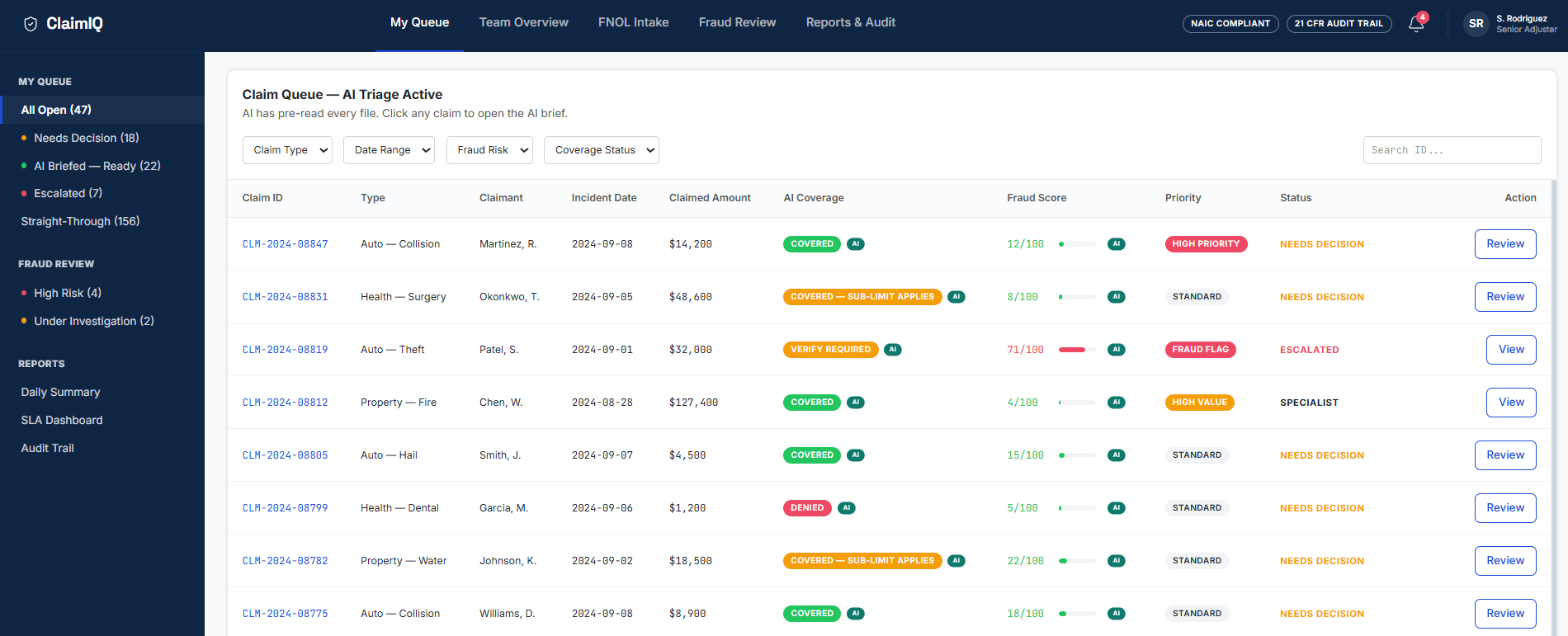

Output and Interaction: How Results Are Delivered

The adjuster-facing experience centres on the structured claim brief – a single document consolidating everything the AI has processed into a decision-ready format. The brief includes the coverage verdict with cited clauses, the fraud score with specific indicators, a summary of all attached documents, a list of any missing or low-confidence information, and the recommended next action. Dashboards display real-time queue status, claim age tracking, and routing decisions across the team. Where integrations connect to existing claims management systems, the AI brief populates directly into the adjuster’s existing workflow rather than requiring a separate interface.

5. What Technologies Power an LLM Insurance Claims Solution?

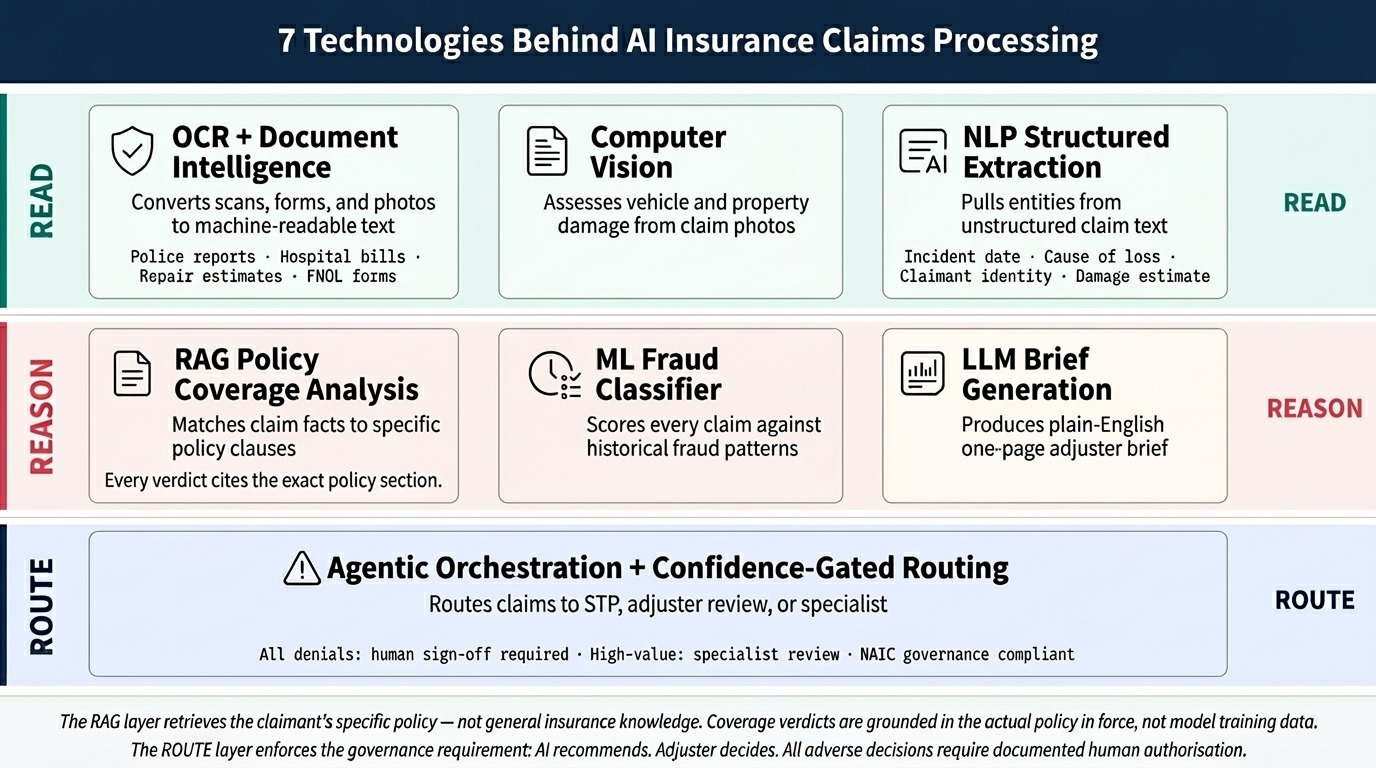

An LLM insurance claims solution combines several specialised AI technologies – and the architecture choice to use separate components rather than one large model is deliberate, not incidental.

A single LLM handling every task in the claims pipeline fails in production for a specific reason: when it gets something wrong, you cannot tell where the failure originated – in document extraction, in policy matching, or in the reasoning layer. Separate components fail visibly and fix cleanly. The LLM reads and summarises. A machine learning classifier scores fraud risk on structured signal patterns. Computer vision assesses damage images. An orchestration layer coordinates the handoffs and handles escalation logic. Each component does one thing it does reliably, and the overall system is as trustworthy as its weakest stage – which you can monitor and improve individually.

Hallucination risk – the concern that an LLM will generate plausible-sounding but incorrect policy language – is handled through grounded generation. The LLM does not reason from its training memory about what a policy might say. It retrieves the actual policy clauses from the RAG system and cites the specific source passage. If the retrieved content does not clearly answer the coverage question, the confidence score drops and the claim escalates to a human rather than the system guessing. The AI never invents a clause; it either finds the relevant text or flags that it could not.

- Large Language Models. The reading and summarisation layer – processes claim narratives, matches retrieved policy language against claim facts, and generates the plain-English adjuster brief. LLMs handle the unstructured text interpretation that rule-based systems cannot manage at the nuance level insurance language requires. They do not make final coverage decisions; they assemble the evidence that supports one.

- Retrieval-Augmented Generation. Connects the LLM to the specific policy documents, claims guidelines, and regulatory references relevant to each claim. Without RAG, an LLM reasons from general training knowledge about what insurance policies typically say. With RAG, it reasons from the actual policy wording in force for the specific claimant – a distinction that matters enormously when coverage turns on exact clause language.

- Computer VisionAn AI technology enabling machines to interpret and analyse images and video – used in claims to assess damage from photographs of vehicles, property, or injury sites. Applied to damage photographs from auto and property claims, computer vision classifies damage severity, identifies affected components, and provides input to repair estimate validation. This is a deliberately separate component from the LLM layer – image analysis is a fundamentally different task from text reasoning and is handled by models trained specifically for it.

- Machine Learning Classifiers. Used specifically for fraud scoring on structured signal patterns – claim timing relative to policy start, amount-diagnosis consistency, claimant history flags, and network-level duplicate detection. ML classifiers handle pattern-based fraud indicators that no explicit rule fully captures, and they operate on structured features rather than raw text. This is intentionally separate from the LLM layer, which handles document reading rather than statistical pattern recognition.

- Agentic AI OrchestrationA framework where multiple specialised AI agents each handle a defined task and pass structured outputs to the next agent in a coordinated workflow. The layer that sequences and coordinates every component in the pipeline – managing the handoffs between intake, OCR, RAG coverage analysis, fraud detection, brief generation, and routing. Orchestration also handles the escalation logic: defining the conditions under which a claim routes to human review and what structured context accompanies that escalation.

- Vector Databases. Store policy documents, regulatory guidelines, and historical claims data as searchable semantic representations. This enables the RAG layer to retrieve policy clauses that are conceptually relevant to the specific claim situation – not just keyword-matched – which matters when policy language uses precise legal terminology that does not mirror how claimants describe incidents in FNOL submissions.

- OCR with Document Intelligence. Converts scanned forms, handwritten documents, and photographs of text into machine-readable format. Every downstream component depends on this layer’s accuracy – low-quality extraction at Stage 1 cascades as errors through every subsequent stage. High-accuracy OCR validated specifically on insurance document types is a non-negotiable foundation, not a commodity choice.

6. What Results Does AI Claims Processing Deliver for Insurance Operations?

AI claims processing delivers measurable improvements across adjuster capacity, settlement speed, fraud detection, cost per claim, and customer satisfaction – directly addressing the operational pain points that drive claims leakage and operating cost overruns.

- Significant reduction in per-claim adjuster review time. By eliminating manual document reading and policy cross-referencing, an AI insurance claims software layer compresses the pre-work phase from hours to minutes. Adjusters handle more files per day without any reduction in decision quality.

- Faster settlement timelines across the claims portfolio. When document assembly and coverage analysis happen in minutes rather than hours, the bottleneck shifts from information gathering to decision-making – where it should always have been. AI insurance claims platform implementations consistently demonstrate measurable cycle time reduction across the claims portfolio.

- Earlier and more consistent fraud detection. The AI screens every claim for fraud signals, not just the ones a time-pressured adjuster flags as suspicious. Coverage extends to the full claim population, and the flagging criteria apply consistently regardless of who is reviewing the file.

- Lower cost per claim through automation of document-intensive tasks. Bain & Company research projects that generative AI in P&C claims handling could reduce loss-adjusting expenses by 20% to 25% and reduce claims leakage by 30% to 50% – representing over $100 billion in potential value for insurers and customers globally.

- Reduced adjuster burnout. Clearing the manual document processing overhead from every case frees adjusters to do the work they were trained for. Teams report higher engagement when technology handles repetitive pre-work and humans handle decisions requiring professional judgment and claimant interaction.

- More consistent reserve setting across the team. When every adjuster reviews the same AI-assembled information baseline, coverage determinations and reserve estimates show less individual variation – reducing the late reserve adjustments that create financial volatility in claims portfolios.

- Improved customer experience and retention. Faster settlements and clearer communication directly address the primary driver of claimant dissatisfaction. The same Accenture research found that nearly 30% of policyholders switched carriers within two years specifically due to poor claims-handling experiences – making claims speed and transparency a direct retention lever, not just a service metric.

- Plain-English denial documentation meeting regulatory standards. When the AI generates denial reasoning in accessible language – citing specific policy clauses and explaining exclusions in plain terms rather than policy section codes – the carrier simultaneously improves compliance, reduces grievances, and demonstrates that AI decisions are explainable and auditable.

7. Is an LLM Insurance Claims Solution Worth the Investment?

A well-scoped LLM insurance claims solution delivers measurable financial returns – but the business case depends on targeting the right bottleneck first, not attempting to automate the entire claims lifecycle at once.

A common pattern across real implementations of this solution is that organisations capturing the fastest and most defensible ROI begin with one specific high-volume workflow – typically document processing and policy matching for a defined claim type – rather than pursuing enterprise-wide deployment from the outset. McKinsey’s research on AI in insurance documents that one major carrier cut liability assessment time for complex cases by 23 days, improved claims routing accuracy by 30%, and reduced customer complaints by 65% through a focused AI claims transformation.

Key Business Metrics This Solution Affects

- Adjuster throughput per FTE. Measure the number of claims handled per adjuster per day before and after deployment. Even a 20% improvement in throughput significantly changes the staffing model at volume.

- Average claims cycle time. Track the number of days from FNOL submission to settlement decision across the claims portfolio. Reduction here improves customer experience scores and directly reduces the financial cost of outstanding claims.

- Claims leakage rate. Measure the difference between what is paid versus what the policy contract specifies. Consistent AI coverage analysis reduces leakage from both over-payment and under-payment, improving portfolio financial accuracy.

- Fraud detection rate on closed claims. Audit a sample of closed claims retrospectively against the AI fraud score at the time of processing. This establishes a baseline for how many fraud cases the system is identifying that manual review missed.

- Cost per claim processed. Calculate total claims operating costs divided by claim count across comparable periods. This is the most direct ROI metric and the most useful for executive and finance presentations during business case construction.

Realistic Implementation and Payback Timeline

A focused deployment targeting one claim type typically produces measurable operational improvements within three to six months of going live. The first gains appear in adjuster document review time, which is measurable from day one. For a mid-size insurer or TPA, a realistic full-programme payback runs twelve to eighteen months, depending on claim volume, implementation scope, and the degree to which existing workflows are redesigned alongside the technology.

Organisations that drop AI onto unchanged workflows – without standardising document intake processes and retraining adjuster roles around AI-prepared information – consistently achieve lower returns than those that treat technology and process change as a single initiative. The business case for acting now rather than waiting rests on a competitive reality: carriers deploying intelligent claims automation today are building data, workflow experience, and adjuster adoption that compound in value over time.

8. What Does Implementing an LLM Insurance Claims Solution Actually Require?

Implementing an LLM insurance claims solution requires addressing four foundational areas: data readiness, system integration, regulatory compliance, and change management – each of which is manageable with the right expertise and sequencing.

Teams that have worked through this integration consistently find that data readiness is the most underestimated requirement. Claims data fragmented across legacy systems with inconsistent formats, incomplete fields, and varying document quality needs standardisation before AI can process it reliably. The technology is ready for deployment; the data infrastructure often needs a preparation phase first.

- Document quality and OCR accuracy. The entire pipeline depends on the quality of document extraction in the first stage. Handwritten forms, low-resolution scans, and multilingual documents require specific OCR configuration and validation. A document quality assessment before deployment identifies where pre-processing support is needed.

- Legacy system integration complexity. Most insurance carriers operate claims management systems with limited or no modern API access. Connecting the AI pipeline to existing platforms may require middleware integration or automation bridges – both achievable, but requiring specific architecture planning upfront.

- Regulatory and data privacy compliance. Insurance claims data is among the most sensitive personal data categories in any jurisdiction. Data flows must be designed so that personally identifiable information does not leave the insurer’s secure environment. In the US, the NAIC Model Bulletin on the Use of Artificial Intelligence Systems by Insurers, adopted December 2023 and now in force or actively pursued in over 24 states, requires insurers to implement written AI governance programmes and demonstrate that AI-assisted decisions comply with all applicable insurance laws. In India, deployments must account for IRDAI’s guidelines on technology-driven insurance operations and India’s Digital Personal Data Protection Act 2023, which requires documented consent management, data minimisation, and audit trails for any system processing policyholder health or financial data. Where on-premises deployment is required, private LLM development within a controlled cloud environment – with PII anonymisation applied before any data reaches the model – satisfies most data localisation requirements across both jurisdictions. For BFSI institutions managing both insurance and banking operations, our RBI circular AI summarizer addresses the parallel RBI compliance monitoring challenge – automatically tracking new circulars and flagging policy gaps for banking-side teams alongside your IRDAI obligations.

- Model drift and ongoing maintenance. Claims patterns change over time – new fraud tactics, new policy language, new claim types. An AI model requires monitoring and periodic retraining to maintain accuracy as claim populations evolve. This is an operational commitment, not a one-time deployment cost.

- Adjuster training and adoption. Technology that adjusters do not trust or use correctly produces no ROI regardless of its technical quality. Structured change management – explaining what the AI does and does not decide, training adjusters on how to use the brief effectively, and creating feedback mechanisms for flagging AI errors – is essential.

- Scoping and phased rollout. Attempting to automate the full claims lifecycle across all claim types simultaneously dramatically increases implementation risk. Starting with one claim type and one workflow phase, measuring outcomes, then expanding is consistently the approach that produces successful deployments rather than expensive stalled pilots.

Where This Solution Has Real Limits

Honest assessment of where an LLM insurance claims solution performs less reliably is important for scoping realistic deployments and setting accurate expectations with stakeholders:

- Ambiguous policy language requires domain expertise, not just AI reasoning. Coverage decisions in genuinely ambiguous situations – where the policy clause is arguable, not clear – should always route to an experienced human adjuster rather than relying on AI output alone.

- AI adds cost when workflows are not standardised first. Industry analysis has documented cases where adding an AI layer to a poorly designed manual workflow increases the cost per claim rather than reducing it. Process design must precede technology deployment.

- Complex litigation and liability claims fall outside current automation scope. Claims involving personal injury, third-party liability, contested causation, or active litigation require human legal reasoning, empathy, and negotiation capability that current AI cannot replicate reliably.

- Fraud detection covers pattern-based signals, not criminal investigation. The AI fraud screening layer identifies statistical anomalies and document inconsistencies – not intent or criminal networks. Confirmed fraud investigation still requires human judgment, specialist fraud teams, and in many cases law enforcement engagement.

9. Which Insurance Operations Teams Benefit Most from This Solution?

This solution delivers its highest value to insurance carriers and TPAs managing claim volumes above the threshold where manual processing creates consistent backlogs – typically organisations handling more than 10,000 claims annually across any single claim type. An AI claims processing platform for large insurance companies applies most directly to P&C carriers managing high-frequency event-driven claims, health TPAs processing reimbursement at volume, and auto insurers managing vehicle damage and liability claims across a large book.

However, intelligent claims automation software for mid-size insurers is equally viable – and often produces faster ROI because mid-size organisations can move from pilot to production deployment more quickly than enterprises burdened by procurement and legacy integration complexity.

This Solution Is Particularly Valuable If…

- Your claims department regularly experiences backlogs where straightforward claims wait as long as complex ones, indicating volume has outpaced adjuster capacity for effective triage

- Your adjusters spend more than 60% of their time on document reading and information assembly rather than coverage decisions and claimant interaction

- Your team lacks consistent reserve setting across adjusters, with retrospective reserve adjustments appearing regularly in portfolio reviews

- Your fraud detection relies primarily on adjuster pattern recognition rather than systematic cross-referencing across the full claim population

- You operate a significant proportion of simple, low-complexity claims that currently consume the same per-claim adjuster time as complex cases

Roles that most directly benefit include Claims Operations Directors, VP of Claims, Chief Claims Officers, and Claims Technology leads – the decision-makers with both the operational context to recognise the bottleneck this solution addresses and the organisational authority to pilot and scale a technology deployment across the claims function.

10. Frequently Asked Questions About AI Insurance Claims Processing

How does an LLM insurance claims solution work for property and casualty insurers?

An LLM insurance claims solution for property and casualty insurers applies large language models to the document-heavy stages of the claims lifecycle – FNOL intake, policy coverage analysis, damage document review, and fraud screening. The system extracts structured data from unstructured documents like police reports, repair estimates, and weather records, then matches claim facts against the relevant policy sections using retrieval-augmented generation. For P&C carriers dealing with high catastrophe-event volumes, the AI triage layer routes claims by complexity and value before adjusters open a single file. The adjuster receives a structured brief rather than a document pile, making coverage decisions faster and more consistent across the team.

Can AI claims processing software actually reduce adjuster workload significantly?

Yes – but the reduction concentrates on specific parts of the adjuster’s role rather than the whole. AI insurance claims software eliminates the document reading, policy cross-referencing, and information assembly that research consistently identifies as consuming the majority of adjuster time before any substantive claims decision is made. The adjuster role shifts from information gatherer to decision-maker, which allows each adjuster to handle more files per day without a reduction in decision quality. The time savings are proportionally larger on high-volume, document-intensive claim types than on complex, judgment-intensive cases.

What does implementing automated claims adjudication software actually require?

Implementing automated claims adjudication software for P&C carriers requires four foundation elements: clean, accessible historical claims data; a defined integration path to existing claims management systems; regulatory compliance planning for how AI outputs are reviewed and documented; and structured change management to support adjuster adoption. The most consistently underestimated requirement is data readiness – claims data fragmented across legacy systems with inconsistent formats needs standardisation before AI can process it reliably. Most organisations with successful deployments start with one claim type or one phase of the claims lifecycle, prove measurable results, then expand.

Is an AI first notice of loss platform reliable enough for production insurance use?

An AI first notice of loss platform is production-ready for structured data extraction, initial triage, and routing decisions – but should not be positioned as making final coverage or payout decisions autonomously. The most reliable FNOL AI systems handle intake, document collection, initial complexity assessment, and routing to appropriate handling channels. Final decisions on coverage, payout amounts, or denials should always include human review as a governance layer, both for decision reliability and for regulatory compliance in jurisdictions requiring explainable AI decisions. Organisations that have deployed FNOL AI most successfully use it to eliminate manual queue management while keeping experienced adjusters focused on decisions that genuinely require their professional judgment.

How long does it take to see returns from an LLM claims solution for mid-size insurers?

Mid-size insurers typically begin seeing measurable operational improvements from an intelligent claims automation software deployment within three to six months when targeting one specific claim type or workflow stage. The fastest returns come from document intelligence and policy matching automation, where adjuster time savings are measurable from the first weeks of live deployment. A realistic full-programme payback for a well-scoped mid-size deployment runs twelve to eighteen months, depending on claim volume, implementation scope, and the degree to which operational workflows are redesigned alongside the technology rather than simply having AI added on top of existing processes.

Build This Solution With Softlabs Group

Softlabs Group builds custom AI claims solutions designed around your specific claims types, document environments, existing systems, and regulatory context – not off-the-shelf products configured to approximate your needs. Our approach begins with an honest assessment of where the processing bottleneck actually sits in your specific operation, followed by a focused first deployment that delivers measurable adjuster time savings before expanding to additional workflow stages or claim types. We work across the full technical stack: document intelligence, RAG-based policy analysis, fraud signal detection, agentic orchestration, and integration with your existing claims management platform.

Whether you are evaluating a first AI deployment in your claims function or looking to move an existing pilot to production scale, our team brings both the engineering capability and the domain understanding to close the gap between what the technology promises and what it delivers in a live insurance environment.