Executive Summary: Why AI Is Redefining How Lenders Assess Credit Risk

Your credit team reviewed the same document bundle three times this week – different analysts, three different risk conclusions on the same borrower. Meanwhile, the review queue keeps growing, faster competitors are approving SME loans in hours, and your compliance team is asking exactly what the model considered before that last declined application. An ai credit underwriting solution addresses all three pressures simultaneously – replacing fragmented manual review with a structured decision pipeline that ingests borrower documents, cross-validates data across multiple sources, scores risk across several dimensions, and generates plain-language explanations for every decision.

This is not a black-box scoring engine. The best implementations combine machine learning (ML)Statistical algorithms that learn patterns from historical data to make predictions on new, unseen inputs models, lender-defined policy rules, and explainability layers so every approval, decline, or escalation can be traced, audited, and defended before regulators. The result is faster decisions, greater consistency, and a credit operation that scales without proportional headcount growth.

1. Why Do Manual Underwriting Delays and Inconsistent Decisions Keep Getting Worse?

Manual underwriting fails at scale because document volume, inconsistency, and compliance pressure compound faster than any team can absorb. Adding more analysts slows the problem rather than solving it – because the bottleneck is not effort, it is the absence of a structured, repeatable decision process that produces the same conclusion for the same evidence every time.

In practice, organisations deploying this type of system typically encounter a specific version of this problem first: the same borrower file reviewed by different analysts on different days produces materially different risk conclusions. That inconsistency is not a training problem. It is a structural one – and an ai automated credit underwriting solution is designed to solve it at the process level, not the individual level.

Context: The Modern Credit Operations Environment

Credit teams at banks, NBFCs, and commercial lenders operate under pressure from three directions simultaneously. Loan volumes are growing across SME, retail, and commercial segments. Regulatory requirements around adverse action explanations, fairness monitoring, and audit readiness are tightening. And borrower data – spread across bureau records, bank statements, GST filings, tax returns, and uploaded documents – arrives fragmented, inconsistent, and in formats that resist standardisation. A McKinsey survey of senior credit risk executives across 24 major financial institutions found that 80% expected to implement at least one AI use case in credit operations within a year – reflecting how fast the gap between early movers and the rest is widening.

The consequence is predictable. Files accumulate, turnaround times lengthen, and experienced analysts spend most of their time on administrative extraction rather than actual risk judgment. Decision quality becomes a function of which analyst handles a file – not what the evidence actually says.

Key Pain Points This AI Solution Addresses

- Manual underwriting delays: Document-heavy applications require hours or days of analyst time for spreading, data extraction, and cross-checking – creating backlogs that cost lenders speed and borrower experience.

- Inconsistent credit decisions: Different analysts interpret the same evidence differently, producing variable risk conclusions that expose lenders to fairness risk and portfolio unpredictability.

- Poor borrower data quality: Borrower-submitted documents arrive in inconsistent formats with missing fields, illegible scans, and contradictory figures across sources – making reliable extraction a recurring problem.

- Lack of explainable AI decisions: Regulators and borrowers require specific, traceable reasons for adverse credit decisions. Systems that generate a score without a clear explanation trail fail this requirement entirely.

- Underwriting workflow bottlenecks: Policy eligibility checks, document completeness reviews, bureau queries, and risk scoring often run sequentially rather than in parallel – multiplying total decision time unnecessarily.

- Fraud and compliance risk: Manually reviewing documents for fraud signals, identity mismatches, and policy violations is time-consuming, inconsistent, and prone to gaps at high volume.

Why Traditional Approaches Fall Short

- Static scorecards cannot handle non-standard borrowers: Rule-based scorecard models struggle with thin-file borrowers, new businesses, or applicants whose risk profile sits outside the narrow bands the scorecard was built on. They also cannot adapt to portfolio shifts without manual recalibration.

- Manual spreading does not scale: Requiring analysts to manually extract, reconcile, and validate figures from multi-source document sets creates a hard capacity ceiling. Hiring more analysts adds cost but does not change the structural bottleneck.

- Legacy systems were not designed for AI: Most loan origination systems (LOS)Software platforms that manage the end-to-end process of receiving, processing, and approving loan applications were built for structured data inputs, not unstructured document processing or real-time ML scoring. Retrofitting them is slow and brittle.

- Siloed data produces incomplete borrower pictures: When bureau data, banking data, GST records, and application data live in separate systems with no reconciliation layer, each analyst builds a different version of the borrower’s financial reality.

- AI versus manual underwriting – what actually changes: Manual underwriting produces decisions in hours or days, with accuracy dependent on individual analyst experience. An ai driven credit underwriting solution processes the same evidence in minutes and applies identical policy rules every time – providing a consistent, auditable decision trail without replacing human judgment on genuinely complex cases.

2. What Is an AI Credit Underwriting Solution?

An ai credit underwriting solution is a controlled decision pipeline that automates risk assessment, policy enforcement, and application routing – while preserving human oversight for complex or ambiguous cases rather than eliminating human judgment entirely. This is not a single AI model replacing an analyst. It is an end-to-end operating layer that handles the repetitive, data-intensive, and pattern-recognition tasks in underwriting so that humans focus exclusively on the judgment calls that genuinely require their expertise.

The right design treats underwriting as five interconnected problems: data ingestion, evidence validation, risk prediction, decision governance, and exception handling. Solutions that focus only on the scoring layer while ignoring ingestion quality and explanation depth consistently underdeliver in production. Clean decisions require clean data – and in lending, clean data is rarely automatic.

Vision and Objectives

- Reduce time-to-decision on standard applications by automating document extraction, spreading, reconciliation, and initial policy screening – the tasks that currently consume most analyst review time.

- Eliminate decision inconsistency by applying the same scoring logic, policy rules, and reason-code framework to every application regardless of submission channel or analyst assignment.

- Produce fully explainable credit decisions with specific factor-level reasons for every adverse action, traceable back to actual data points in the borrower’s file.

- Enable controlled auto-decisioning for high-confidence, low-complexity applications while routing genuinely ambiguous cases to human review with a structured evidence pack already prepared.

- Monitor portfolio performance continuously after booking – tracking score drift, early delinquency, and segment-level shifts – so decisioning logic adapts as the portfolio and economy change.

- Scale throughput without proportional headcount growth, allowing lending operations to handle volume increases through intelligent routing rather than additional analyst hiring.

3. How Does an AI Credit Underwriting Solution Work in Real Lending Environments?

Three real lending contexts show how an ai credit underwriting solution moves from concept to measurable operational impact across different institutions and borrower types.

Mid-Size Bank Managing High Commercial Loan Volume

Your credit department processes hundreds of commercial loan files every month, and each arrives in a different format – some structured, most not. Analysts spend the first hour of each review extracting figures that should already be structured. Data mismatches between financial statements and bank records surface only when a sharp reviewer catches them manually.

An ai driven credit underwriting solution automates document classification, extraction, and cross-source reconciliation before an analyst touches the file. Flagged mismatches arrive with source references attached, so analysts review specific anomalies rather than re-reading entire document stacks. Policy eligibility runs in parallel, eliminating a separate screening step. Decision turnaround time decreases, and the team shifts from administrative extraction to judgment-intensive review.

NBFC Processing SME Working-Capital Applications

Most of your SME applicants have incomplete bureau histories, so underwriters are building a risk picture from scratch on nearly every file. GST filings, bank statements, and tax returns arrive separately, covering different periods with no standard reconciliation. A single analyst spreads three or four files per day while volume keeps growing.

An ai credit underwriting solution for NBFCs extracts and reconciles data across all available sources. It builds a borrower profile with confidence scores assigned to each data point. When bureau data is thin, the system uses cash-flow patterns, GST filing consistency, and banking behavior as primary risk signals. Sufficient-evidence cases populate a structured review pack automatically. Data-gap cases escalate with a clear record of what is missing – so underwriters reach a decision faster even on incomplete files.

Commercial Lender Assessing Borrowers with Complex Group Structures

The borrower has four related entities, three of them active borrowers with other lenders – and your analyst just spent two days trying to map the group exposure. Pulling data across multiple filings, bureau records, and registry sources manually introduces errors and takes days. By the time the picture is assembled, the borrower’s financial position may have shifted.

An ai based credit underwriting solution consolidates entity-level and group-level data from bureau, registry, and third-party sources in a single enrichment pass. Related-party connections surface automatically. Group exposure, cross-default risk, and collateral overlap appear in one structured view. Credit analysts focus on interpreting the risk picture rather than assembling it – cutting both review time and exposure-mapping errors significantly.

Ready to explore what this solution looks like for your organisation?

Talk to Our AI Team4. How Does an AI Credit Underwriting Solution Process a Loan Application?

An ai powered credit underwriting solution does not run a borrower file through a single model. Instead, it moves the file through a series of specialised services – each solving one part of the evidence problem before the next step begins. Understanding this architecture helps lenders evaluate whether a proposed solution is genuinely robust or a single-model wrapper dressed up as a platform.

Data Acquisition: Multi-Source Borrower Information

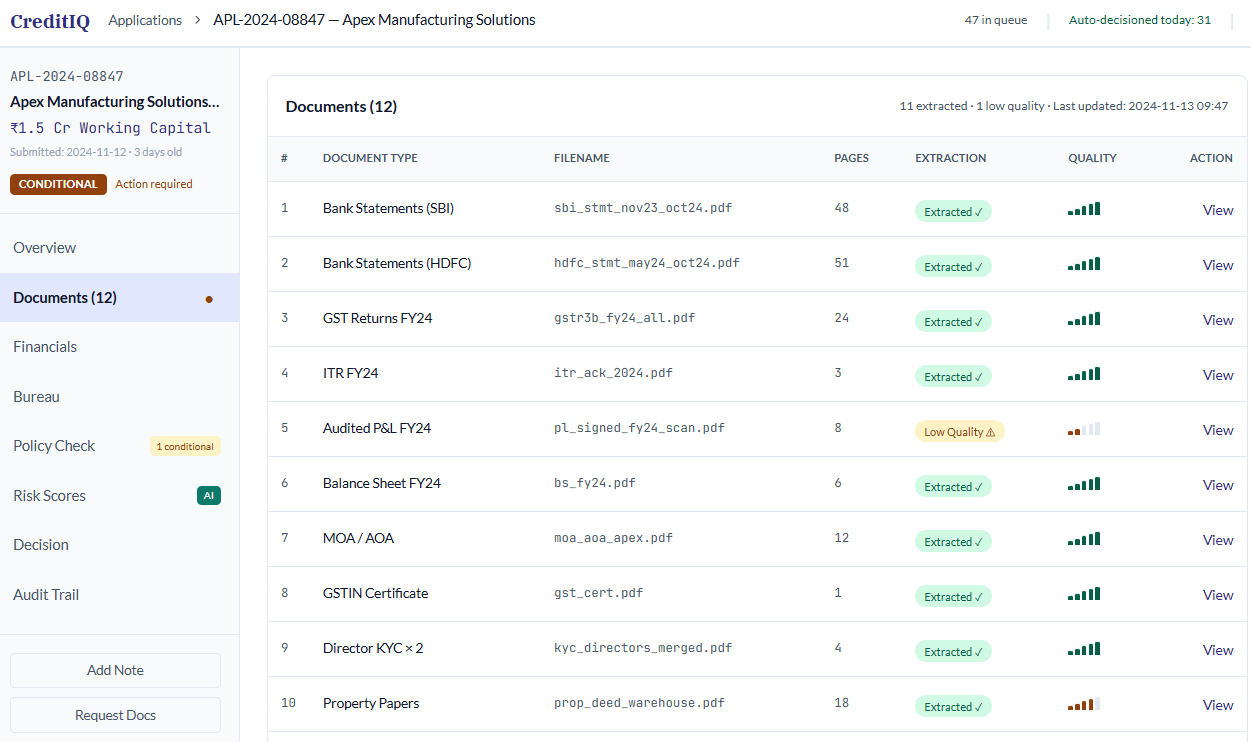

The system ingests borrower data from multiple channels simultaneously: direct borrower portal uploads, branch-submitted files, partner API feeds, email attachments, LOS sync, and bulk back-office imports. Input types include bank statements, GST returns, income tax returns, audited financial statements, KYC documents, collateral papers, and application forms. Every incoming file receives a unique case ID immediately, creating a traceable record before any processing begins.

The system also detects duplicate submissions, corrupted files, password-protected PDFs, and mixed-document bundles at this stage. Poor-quality inputs route to an operations queue rather than proceeding downstream – because material the system cannot reliably process should never silently influence a credit decision.

Teams that have worked through this integration consistently find that ingestion design – not model sophistication – determines whether the system actually works in production. A pipeline that accepts any input without validation propagates errors into every downstream step. Building ingestion as its own quality-controlled product surface is the difference between a system that reliably works and one that fails quietly at volume.

The AI Processing Pipeline

- Intake and Case Creation. The system creates a traceable case record the moment a file arrives – whether from a borrower portal, branch upload, LOS sync, or partner API. It runs document completeness checks and schema validation on structured fields immediately, flagging missing mandatory items before processing begins rather than after.

- Document Triage and Preprocessing. Every incoming file passes through preprocessing before optical character recognition (OCR)Technology that converts scanned document images into machine-readable text for further extraction and analysis begins. The system de-skews scans, corrects page orientation, and removes noise. It also splits multi-document bundles and classifies each file by type. Poor-quality files route to an operations queue for re-upload rather than passing degraded content downstream.

- OCR and Intelligent Extraction. Next, the system runs multi-engine OCR across every classified document, extracting fields, tables, and narrative text with source-linked traceability. Each extracted value maps back to its origin page and coordinates – because analysts and auditors need to verify where a figure came from, not just what value was extracted.

- Cross-Source Reconciliation. Once extracted, the system builds a canonical borrower profile by comparing the same fact across multiple sources. It checks whether declared turnover broadly agrees with bank inflows and GST sales before accepting any single figure as reliable. Mismatches receive confidence scores and explicit flags rather than silent resolution – so analysts see exactly where the evidence conflicts.

- External Verification and Enrichment. The verification layer queries bureau data, banking APIs, fraud registries, identity verification services, and business registration databases to cross-validate extracted facts. Each data point receives a status: verified, inferred, conflicting, or missing. This prevents the system from relying solely on borrower-supplied data where external validation is available.

- Policy Engine Pre-Screening. Before any model runs, the policy engineA configurable rule-based system that applies lender-defined credit policies, eligibility criteria, and regulatory constraints before or after model scoring applies lender-defined rules to eliminate ineligible cases early. Banned industries, missing mandatory documents, exposure limit violations, and regulatory constraints are all checked here. The model never scores a case that should have been rejected at the policy level.

- Feature Engineering. Validated evidence transforms into underwriting features: cash-flow volatility, debt service coverage ratio (DSCR)A financial metric comparing available cash flow to total debt obligations – a core indicator of a borrower’s repayment capacity, receivable concentration, overdraft frequency, bureau repayment history, leverage ratios, and documentation completeness scores. These features feed the scoring models rather than raw extracted data, ensuring calibrated and consistent inputs.

- Multi-Model Risk Scoring. The system runs separate, calibrated models for default risk, fraud risk, income stability, and documentation anomaly risk rather than relying on one model to handle everything. Each model outputs a calibrated probability score. Separating these concerns produces more interpretable outputs and allows each model to be retrained independently as performance shifts.

- Decision Composition and Explanation. The decision composer combines model scores, policy results, and confidence levels into one actionable decision packet: approve, conditionally approve, reduce amount, request additional documents, escalate to analyst, or decline. For every non-approval, the explanation layerA system component that translates model factor contributions into specific, plain-language reason codes required by regulatory adverse action notice standards generates specific reason codes tied to actual negative factors in the borrower’s file – meeting the explainability requirements that regulators impose on lenders using AI in credit decisions.

- Post-Booking Monitoring and Feedback. After booking, the system tracks early delinquency, score drift, approval-rate shifts, and segment-level performance. Outcome data feeds back into threshold tuning, model retraining schedules, and policy review cycles – so decisioning logic adapts as the portfolio, borrower mix, and economic environment change over time.

Human-in-the-Loop: Where Human Judgment Still Matters

Effective ai credit underwriting solutions concentrate human effort where it genuinely adds value rather than removing humans from the process entirely. Human oversight remains essential in four areas:

- Exception and escalation review: Cases flagged as low-confidence, high-conflict, or outside standard policy parameters route to a human analyst with a structured evidence pack, flagged mismatches, and the model’s reasoning already prepared. The analyst reviews anomalies – not raw documents.

- Override with justification: Human analysts can override model recommendations when they identify qualitative factors the system cannot assess. Every override is logged with a reason code, creating a feedback loop that improves policy calibration and builds training data over time.

- Policy calibration and threshold setting: Credit risk managers set and adjust auto-decisioning thresholds, confidence cutoffs, and policy rules. The system executes within those boundaries – it does not set them independently.

- Fairness monitoring and bias review: Regular human review of approval rate distributions across demographic segments, geographies, and product types is essential for detecting model biasSystematic errors in model predictions that disadvantage certain groups – a critical compliance concern in regulated credit decisioning before it becomes a regulatory problem.

Output and Interaction: How Results Are Delivered

The analyst-facing workbench presents extracted data, source document references, cross-source mismatches, external verification results, model scores, factor-level reason codes, and a recommended action – all in one structured view. Analysts correct extraction errors, add qualitative notes, and submit overrides through the same interface.

Decision outcomes deliver to the LOS via API for seamless booking. Adverse action notices generate automatically with the specific reason codes required for regulatory compliance. Portfolio managers access real-time dashboards showing approval rates, manual review volumes, score distributions, and early-delinquency signals by segment, product, and channel.

5. What Technologies Power an AI Credit Underwriting Solution?

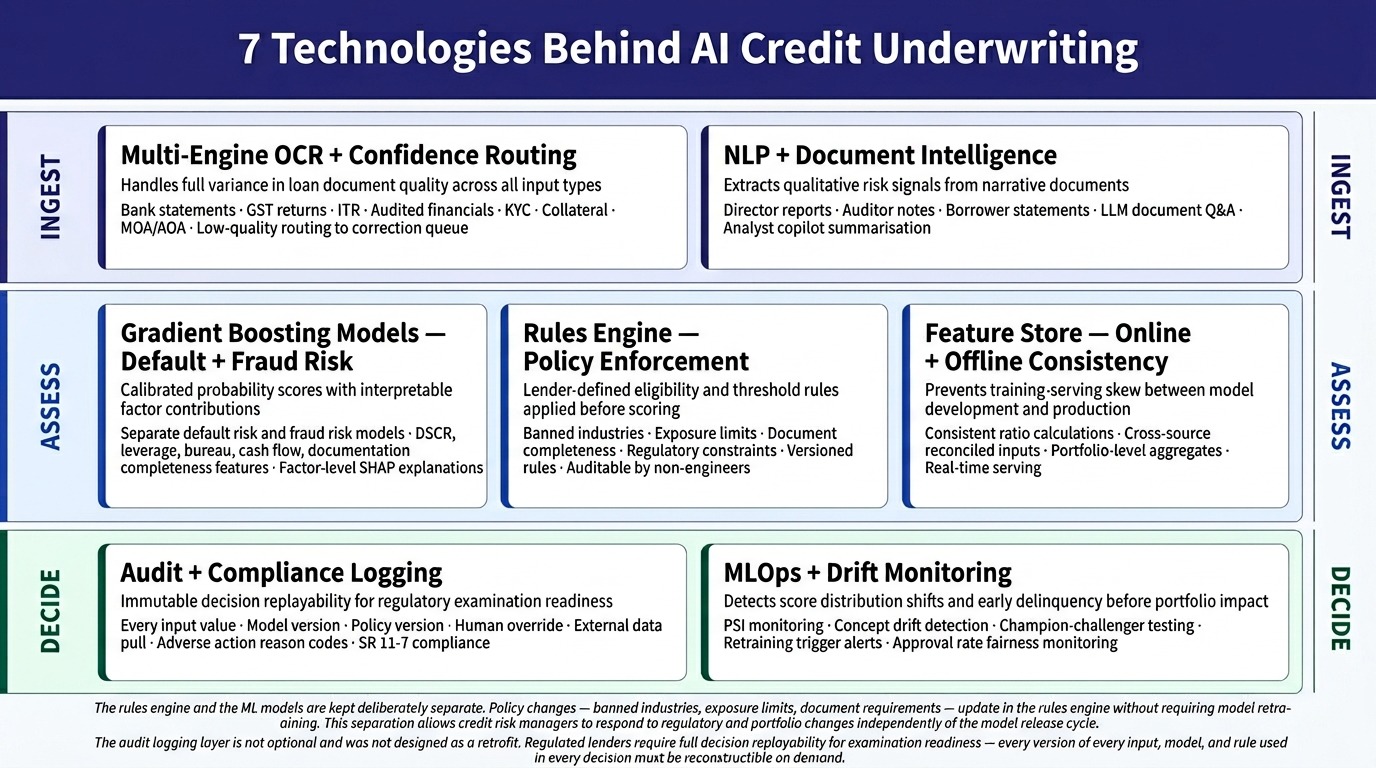

Seven core technologies power a robust ai credit underwriting solution – each solving a specific gap that simpler, single-model approaches leave open.

- Gradient boosting modelsEnsemble ML models that build sequential decision trees, widely used for tabular credit risk prediction due to their accuracy and interpretable feature contributions: Structured tabular credit data fits gradient boosting approaches better than generative models for risk scoring. These produce calibrated probability outputs with interpretable factor contributions – essential for explaining adverse action reasons to analysts and regulators. An ai driven credit underwriting solution typically deploys separate gradient boosting models for default risk and fraud risk rather than one unified model.

- Natural language processing (NLP)The AI discipline enabling computers to extract meaning from, and reason about, human language in unstructured text documents: NLP components extract narrative information from director reports, auditor notes, and borrower statements – capturing qualitative risk signals that structured fields miss entirely. Large language models support document summarisation, document Q&A, and analyst copilot functions but do not make final credit decisions in a well-designed system.

- Multi-engine OCR with confidence routing: Real-world loan document quality varies too widely for a single OCR engine to handle reliably. A robust solution routes low-confidence page extractions to alternate OCR configurations or human correction queues rather than passing degraded text downstream.

- Feature storeA centralised repository that manages engineered features for both model training and real-time scoring, ensuring consistent definitions between development and production: Consistent online and offline feature definitions prevent the training-serving skew that causes models to perform differently in production than they did during development – a common and costly failure mode in deployed credit AI.

- Rules engineA configurable system that applies explicit if-then credit policy logic, enabling eligibility rules to be updated by credit managers without requiring code changes: Credit policy changes frequently and must remain readable, testable, and auditable by non-engineers. A versioned rules engine decouples policy logic from model logic – allowing credit risk managers to update eligibility criteria independently of ML model releases.

- MLOps and drift monitoringPractices and tooling for deploying, monitoring, and maintaining ML models in production, including detecting when model performance degrades as input distributions shift: Credit decisioning models require regular monitoring for input distribution shifts, borrower mix changes, and early outcome deterioration. Population stability index (PSI)A metric used to detect whether a model’s input feature distribution has shifted significantly from the training population, signalling potential score degradation and concept drift metrics detect problems before they appear as portfolio losses.

- Audit and compliance logging: Every input value, model version, policy rule version, human override, and external data pull requires an immutable audit log. Regulated lenders need full decision replayability for examination readiness, and the system must support this from day one – not as a retrofit.

6. What Results Does an AI Credit Underwriting Solution Deliver?

Deploying an ai credit underwriting solution delivers improvements across processing speed, decision quality, compliance readiness, and portfolio risk visibility. Each benefit below connects directly to a specific pain point that manual workflows cannot resolve at scale.

- Significantly faster time-to-decision: Automating document extraction, spreading, reconciliation, and policy screening removes the most time-consuming manual steps from the analyst workflow. Standard applications that previously took hours or days progress to a decision-ready state in minutes.

- Consistent, audit-ready credit decisions: Every application receives the same scoring logic, policy enforcement, and reason-code framework regardless of submission channel or analyst assignment – directly addressing the inconsistent credit decisions that create fairness exposure and portfolio unpredictability.

- Reliable evidence even from poor-quality documents: The reconciliation and confidence-scoring approach handles poor borrower data quality by flagging conflicts rather than silently accepting unreliable inputs. Analysts see exactly where evidence is strong and where verification is needed.

- Regulatory compliance for adverse action explanations: Automatic generation of specific, factor-level reason codes for every non-approval directly solves the explainability problem – meeting regulatory requirements without additional manual effort from the credit team.

- Elimination of underwriting workflow bottlenecks: Parallel processing of document extraction, policy eligibility, and external verification removes the sequential bottlenecks that inflate decision cycle time in traditional manual workflows.

- Stronger fraud detection and compliance controls: Automated cross-checking against fraud registries, identity databases, bureau records, and behavioral signals detects fraud and compliance risk patterns that manual review misses at volume.

- Portfolio-level monitoring and early warning: Continuous post-booking monitoring of score drift, early delinquency, and segment-level performance gives credit risk teams early warning before individual loan problems become portfolio-level issues.

- Scalable operations without proportional cost growth: An ai automated credit underwriting solution routes only genuinely complex cases to human review, allowing lending volumes to grow without a corresponding increase in analyst headcount or review queue depth.

7. Is an AI Credit Underwriting Solution Worth the Investment?

An ai credit underwriting solution delivers measurable return across four key business metrics: application processing time, manual review volume, cost per credit decision, and analyst capacity per FTE. Building a credible internal business case means establishing baseline measurements on each of these before deployment and setting specific targets for post-go-live performance.

A common pattern across real implementations of this solution is that the first measurable return comes not from the AI model but from the document intelligence and spreading automation layer. This layer reduces analyst time per application significantly within the first months of deployment – well before full automated decisioning goes live. Phased planning is therefore not a delay; it is the approach that produces the most defensible ROI story.

Key Business Metrics and What to Measure

- Average time-to-decision per application: Measure current median and 90th-percentile turnaround times by product, channel, and application complexity. Track the same metrics post-deployment, segmented by auto-decided versus analyst-reviewed cases, to isolate where time savings are generated.

- Manual review rate: Calculate the percentage of total applications currently routed to human review. The goal is not zero – it is reducing manual review to genuinely complex or high-risk cases while auto-deciding straightforward, high-confidence files confidently.

- Analyst capacity – applications per FTE per day: Baseline the current number of applications each analyst completes daily, including all document handling tasks. Post-deployment, this metric should improve as analysts shift from extraction work to judgment-intensive review.

- Decision consistency score: Shadow-score a sample of historical decisions and measure the percentage that would receive the same outcome under the new system. Significant variance indicates the current process has inconsistency worth correcting – and provides a quantified pre-deployment baseline.

- Early delinquency rate on auto-approved cohorts: After controlled auto-decisioning goes live, track 30-day and 90-day delinquency rates on auto-approved loans against the benchmark rate on manually approved loans from the same period. This is the core credit quality proof point for the business case.

Realistic Implementation and Payback Timeline

For a mid-size lender, a phased deployment typically delivers initial value within three to five months through document intelligence and analyst workbench tools – the phases that remove the most manual effort before any automated decisioning goes live. Full pipeline deployment, including policy engine configuration, model training on historical outcome data, and controlled auto-decisioning, typically requires eight to twelve months.

For lenders already experiencing manual review backlogs, the case for acting now is straightforward. Every month of delay represents a measurable cost in analyst capacity, decision inconsistency, and competitive speed disadvantage against lenders who have already deployed.

8. What Does Implementing an AI Credit Underwriting Solution Actually Require?

What implementation experience reveals that theoretical explanations often miss is this: ingestion quality, reconciliation accuracy, and LOS integration complexity determine project success far more than any AI algorithm does. Lenders that enter deployment expecting to focus on AI algorithms consistently encounter the real work at the data layer first.

- Historical outcome data for model training: Supervised ML models for credit risk require labelled historical data – applications with known repayment outcomes. Lenders with less than two to three years of outcome data in a specific product segment need longer model development timelines. Alternative modelling approaches may also be required for thin-history portfolios.

- Data governance and privacy compliance: An ai credit underwriting solution for banks and regulated NBFCs must operate within strict data handling frameworks – including data residency requirements, borrower consent management, and regulatory data retention rules. For institutions with strict data sovereignty requirements, private LLM development approaches allow sensitive borrower data to remain entirely within the lender’s own infrastructure.

- LOS and core banking integration complexity: Integration with legacy loan origination systems frequently becomes the critical path in deployment. Most legacy LOS platforms were not designed for real-time API-based communication with ML scoring services. Integration timelines should be planned conservatively, with production integration tests beginning early in the project.

- Model maintenance and retraining cadence: Credit models require ongoing monitoring and periodic retraining as borrower populations, economic conditions, and product mixes shift – a requirement the Federal Reserve’s supervisory guidance on model risk management (SR 11-7) formalizes for regulated lending institutions. Budget and team allocation for model maintenance is a recurring operational cost – not a one-time project expense that ends at go-live.

- Change management for credit teams: Credit teams that understand how the system reaches its recommendations adopt the workflow more readily. Deliberate onboarding and clear explanation of model logic are not optional add-ons – they are the difference between a tool that gets used and one that gets circumvented.

- Champion-challenger testingA model deployment practice where a new challenger model runs in parallel on live traffic to compare performance against the current production model before replacing it: New models or threshold changes should always run in shadow mode against current production logic before replacing it. This prevents untested changes from affecting portfolio quality and provides the evidence base for model sign-off.

Where This Solution Has Real Limits

- Highly sophisticated fraudulent documents – for example, digitally altered bank statements with internally consistent formatting – remain challenging for extraction-based detection. Additional fraud verification APIs and manual spot-checking on high-value applications remain necessary at any deployment maturity level.

- New businesses with less than 12 to 18 months of verifiable operating history provide insufficient data for reliable ML-based risk scoring. These cases benefit from the structured evidence presentation the system provides, but they require human judgment for final decisions.

- Sudden macroeconomic regime shifts can cause model performance to degrade, since models trained on stable-period data cannot anticipate structural changes in borrower behavior. Active monitoring protocols and pre-agreed retraining triggers are essential – not optional contingency plans.

- Integration timelines with legacy core banking and LOS systems are frequently underestimated. A deployment that looks straightforward in a proof-of-concept environment can encounter significant delays when connecting to production systems with strict change management processes.

9. Who Gets the Most Value from an AI Credit Underwriting Solution?

Lenders with high-volume, document-heavy workflows and strict regulatory requirements gain the most from an ai credit underwriting solution. The solution scales well across institution types – from mid-size NBFCs running SME lending programs to large commercial banks managing diverse multi-product portfolios. However, certain operational profiles generate disproportionately strong returns.

- Banks processing commercial or retail loan volumes at scale: The best ai credit underwriting solution for banks combines multi-source document intelligence with policy enforcement and audit-ready explainability – addressing throughput and compliance requirements simultaneously.

- NBFCs and fintech lenders in SME and MSME segments: Lenders serving borrowers with thin bureau histories benefit from alternative data reconciliation and cash-flow-based risk signals rather than bureau-dependent scoring alone. An ai credit underwriting solution for NBFCs handles the data-gap problem structurally rather than defaulting to decline.

- Commercial lenders with complex group-structure borrowers: The solution for commercial lending adds the most value when group exposure mapping, related-party detection, and multi-entity reconciliation are current manual bottlenecks – cases where analyst time is consumed by assembly rather than judgment.

- Any lender facing regulatory examination readiness pressure: Institutions under review for adverse action compliance, fairness testing, or model risk management requirements benefit immediately from the explainability, audit logging, and monitoring capabilities the solution provides.

This solution is particularly valuable if your institution processes more than 200 applications per month per product, if your current manual review rate exceeds 40% of total applications, if you have experienced regulatory scrutiny around adverse action explanations, or if analyst capacity constraints are currently limiting lending volume growth. It is also well-suited to enterprise-scale AI development contexts where the underwriting system must integrate with multiple existing platforms and support several product types simultaneously.

10. Frequently Asked Questions About AI Credit Underwriting Solutions

These five questions address what lenders most frequently ask when evaluating an ai credit underwriting solution – from regulatory compliance to implementation scope.

What is the best AI credit underwriting solution for lenders trying to reduce manual review volume?

The best ai credit underwriting solution for lenders combines document intelligence, policy rule enforcement, and explainable risk scoring within a single controlled pipeline rather than treating them as separate systems. The goal is not full automation – it is confident automation for clean, high-confidence cases while routing ambiguous ones to analysts with a structured review pack already prepared. Lenders that achieve the strongest results typically start with one loan product segment, prove the pipeline on that cohort, and expand incrementally. A well-designed system reduces manual review queues by routing only genuinely complex cases to human reviewers rather than treating every application as a manual task by default.

How does an AI credit underwriting solution for banks handle adverse action compliance?

An ai credit underwriting solution for banks must generate specific, plain-language reasons for every adverse or modified credit decision – not vague references to model output. Regulatory frameworks require lenders to explain adverse actions in terms the borrower can understand and act on. A compliant system separates the explanation layer from the scoring layer, mapping model factor contributions to readable reason codes that auditors and regulators can trace back to actual data points in the borrower’s file. Full audit logs covering every input, model version, policy rule version, and human override are essential for examination readiness. Generic checklist-based adverse action notices are insufficient when AI models are involved in the decision.

Can an AI credit underwriting solution work for NBFCs dealing with thin-file or first-time borrowers?

Yes – but it requires the right design. An ai credit underwriting solution for NBFCs works best when it incorporates alternative data signals such as cash-flow patterns from bank statements, GST filing consistency, and business registry data alongside bureau scores, because thin-file borrowers lack deep bureau history. The system should treat missing bureau data as a signal to assess rather than a hard blocker that triggers automatic decline. A well-designed reconciliation layer presents available evidence clearly to the human reviewer, so that even data-light cases receive a structured, evidence-based assessment rather than a default rejection based on data absence alone.

How does an AI credit underwriting solution for SME loans speed up the decision process?

An ai credit underwriting solution for SME loans accelerates decisions by automating the most time-consuming manual tasks: extracting and spreading financial statements, reconciling bank statement data, cross-checking declared turnover against GST and banking records, and running initial policy eligibility screens. Instead of an analyst spending hours on data gathering, the system delivers a structured evidence pack within minutes. The analyst then focuses on judgment calls – assessing qualitative factors, reviewing flagged mismatches, and handling exceptions. This shift from full manual spreading to analyst-as-reviewer typically produces significant reductions in per-application decision time for standard SME applications without sacrificing decision quality.

What does implementing an AI credit underwriting solution for commercial lending actually require?

Implementation scope varies significantly by institution size, data availability, and integration complexity. A focused deployment covering document ingestion, financial spreading, and analyst workbench tools typically takes three to five months for a mid-size lender. Adding policy engine configuration, model training on historical outcome data, and controlled auto-decisioning extends the full pipeline to eight to twelve months. The primary time and cost drivers are data preparation quality, LOS integration depth, and compliance validation. Organisations that phase deployment – starting with analyst-assist tools before moving to automated decisioning – achieve faster initial value and carry lower deployment risk than those attempting a full-pipeline launch from day one.

Build This Solution With Softlabs Group

Softlabs Group builds custom ai credit underwriting solutions designed around each lender’s specific data environment, product portfolio, policy framework, and regulatory obligations. Our work spans the full pipeline – from document intelligence, multi-source reconciliation, and policy engine configuration through multi-model risk scoring, explainability layers, analyst workbench tools, and post-deployment monitoring. We treat each engagement as both an engineering and a domain challenge, because no two lending operations share the same document mix, borrower segment, or compliance context, and pre-packaged models do not adapt to yours.

Whether you are a bank, NBFC, commercial lender, or fintech lending operation evaluating an ai credit underwriting solution, the right first step is a structured conversation about your current data, volumes, LOS environment, and decision objectives. Contact us to discuss your specific requirements and explore what a custom solution looks like for your institution.