Executive Summary

The Indian financial services sector is currently navigating a period of unprecedented complexity. We are witnessing a collision between two massive forces: the accelerating velocity of digital innovation (Fintech, UPI, Digital Lending) and the absolute rigidity of regulatory compliance. To maintain operational stability amidst this chaos, forward-thinking institutions are turning to an RBI Circular Search & Summarizer AI to bridge the gap. The Reserve Bank of India (RBI), in its mandate to safeguard financial stability, operates one of the most sophisticated and dynamic regulatory regimes in the world.

For Scheduled Commercial Banks (SCBs), NBFCs, and emerging Fintech players, this dynamic creates a formidable operational bottleneck. The “old way” of doing things—relying on teams of legal experts to manually monitor the RBI website every morning—is broken. It is too slow, too expensive, and statistically prone to critical human error. However, simply “digitizing” these documents is not enough. Generic AI tools fail because they lack the “legal logic” to understand how a 2025 amendment implicitly modifies a 2015 Master Direction without explicitly naming it.

This report provides an exhaustive, engineer-to-engineer technical analysis of the RBI Circular AI Summarizer by Softlabs Group. After rigorous evaluation, we advocate for a GraphRAG (Graph Retrieval-Augmented Generation) architecture. This is not a “magic box” for automated compliance, but a structured Decision Support System designed to act as a force multiplier for your compliance team. It offers multi-hop reasoning, audit trails, and implicit supersession detection, initially focused on high-impact regulatory domains like KYC/AML and Digital Lending.

1. The Compliance Crisis with RBI Circulars

1.1 The Volume and Velocity of Regulatory Change

Figure 2: The Magnitude of Regulatory Complexity

Figure 2: The Magnitude of Regulatory Complexity

To truly understand the necessity of an RBI Circular AI Summarizer, one must first appreciate the sheer scale of the regulatory environment. The RBI does not govern through static laws that remain unchanged for decades; it governs through dynamic instructions that cover every facet of banking operations. This ranges from the minutiae of Know Your Customer (KYC) video verification pixels to the macroscopic parameters of Capital Adequacy Ratios (CAR) and Liquidity Coverage Ratios (LCR).

The complexity is compounded by what we call “Regulatory Layering.” Over the past seven decades, the RBI has issued thousands of circulars. In a recent massive consolidation exercise, the regulator retired over 9,000 obsolete circulars. This fact alone highlights the immense difficulty of the landscape: if the regulator itself had to identify nearly 10,000 documents that were clogging the system, how can a human compliance officer be expected to distinguish between a valid instruction and a defunct one in real-time without the aid of a dedicated RBI circular analysis tool?

The velocity of change is equally daunting. In sectors like digital payments, guidelines can evolve monthly. A revised KYC rule is not merely a memo to be filed; it is a binding legal instruction that requires immediate changes to software code, operational workflows, and customer contracts. Missing a single update can render an entire onboarding process non-compliant overnight.

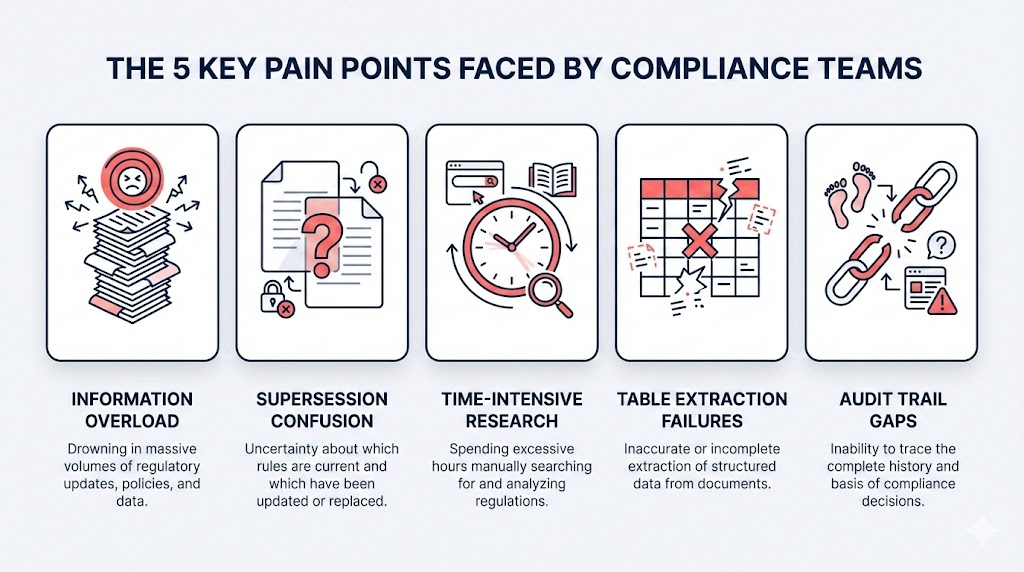

1.2 The “Supersession Trap”

The most dangerous aspect of compliance is determining validity. We call this the Supersession Trap. In the RBI ecosystem, a new circular often supersedes an older one without explicitly naming it in the title. This is where an AI-based RBI circular finder proves invaluable, as it can trace the lineage of a regulation. It might simply say “Modification to Para 2.1 of Master Direction on Credit Cards.”

Consider a human reader searching for “Credit Card Limits.” They might find the 2021 Master Direction because it is a large, comprehensive document with high keyword density. They might miss the small, 1-page notification from 2023 that changed the limit. If they apply the 2021 rule today, they are in direct violation of the law. This happens constantly in manual workflows because humans rely on memory and incomplete keyword searches.

Figure 3: Critical Challenges Faced by Compliance Teams

Figure 3: Critical Challenges Faced by Compliance Teams

1.3 The Economic and Reputational Cost of Failure

The consequences of failing to keep pace with this velocity are not theoretical. In FY 2024-25, the RBI imposed penalties totaling ₹54.78 crore across 353 regulated entities. But focusing on the fine amount is a mistake. The fine is just the “entry fee” to a crisis.

The real cost lies in Business Restrictions and Growth Freezes. In severe cases, the RBI may impose restrictions, such as stopping a bank from issuing new credit cards or onboarding new digital customers. For a growing bank, being banned from acquiring customers for 6 months is a catastrophic loss of market share. Deploying an RBI Circular AI Summarizer is a strategic defense against these costly remediation efforts, which often exceed the initial penalty by a factor of ten.

2. Why Standard Search Fails

Many “RegTech” tools today claim to use AI, but under the hood, they are often just glorified RBI Master Directions search tools or basic ChatGPT wrappers using standard Vector RAG. Our technical evaluation confirms that standard Vector RAG fails in banking for three specific, structural reasons that cannot be fixed by just “adding more data.”

Figure 4: Limitations of Generic AI in Banking

Figure 4: Limitations of Generic AI in Banking

2.1 Semantic Similarity ≠ Legal Validity

In vector search, text is converted into numbers (embeddings) based on meaning. Unfortunately, a superseded circular often looks identical to the valid one that replaced it. Both documents contain words like “KYC,” “Limit,” and “Customer Verification.” Unlike a specialized RBI Circular PDF summarizer, a standard vector search might retrieve the old, invalid rule because it has a higher keyword match or was clicked more often historically. It lacks the Structural Validity to understand that one rule has legally replaced the other. A high “similarity score” does not mean a “correct legal answer.”

2.2 No Temporal Logic

Standard search treats a 1999 document with the same relevance as a 2025 document. It lacks the logic to understand that time renders the former obsolete. If keyword density is high in the old document, the AI will confidently serve it as the answer, leading to dangerous hallucinations. A vector database does not inherently understand time; it only understands linguistic proximity.

2.3 The “Exception” Blind Spot

Financial rules are full of complex conditional logic. For example: “Risk weight is 35% EXCEPT for LTV > 80% unless borrower qualifies under PMAY.” Often, the main rule is on Page 5, but the exception is in a footnote on Page 6 or even in a different amendment circular. Standard text chunking breaks the logical connection between the rule and the exception. This leads to Exception Handling Failure, where the AI provides a general rule while missing the critical exception that applies to your specific case, leading to misreporting of risk.

3. Our RBI Circular AI Summarizer Architecture

Softlabs Group addresses these systemic failures with a purpose-built RBI circular explanation platform. We move beyond simple search to implement a GraphRAG (Graph Retrieval-Augmented Generation) architecture. This system models the legal relationships between documents, ensuring that “supersession” and “exceptions” are respected.

Figure 5: The Multi-Layered Technical Architecture

Figure 5: The Multi-Layered Technical Architecture

3.1 Layer 1: Intelligent Document Processing (IDP) with Computer Vision

The first challenge is data ingestion. We utilize advanced Computer Vision to handle the “Data Trap” of PDFs. Unlike standard OCR which simply extracts text line-by-line (often scrambling columns), our system uses Table Structure Recognition (TSR) models like Microsoft Azure Document Intelligence or AWS Textract. These models “look” at the document to identify grid lines and merged headers. This ensures that “Risk Weight 75%” stays linked to its correct column, preserving the numerical integrity of the data.

3.2 Layer 2: The Regulatory Knowledge Graph

This is the core innovation. Instead of storing documents as isolated files, we map the relationships between them in a Graph Database (Neo4j). We create a “Knowledge Graph” where every Circular is a Node, and relationships are Edges. This enables two critical capabilities:

- Implicit Supersession Detection: We map the SUPERSEDES edges. If Circular B replaces Circular A, the graph knows it. When you search, the system automatically checks the graph, sees that Circular A is linked to a “Superseded” status, and filters it out. You only ever see the valid law.

- Multi-Hop Reasoning: The system can “hop” across documents. To answer “What is the penalty for Tier-2 NBFCs violating CRILC reporting?”, it hops from the Penalty Section node to the NBFC Definition node to the Tier-2 Criteria node. It synthesizes a complete answer from three different documents, something standard search cannot do.

3.3 Layer 3: Private, Domain-Adapted LLMs

Financial institutions cannot upload sensitive data to public AI models like ChatGPT. Softlabs deploys open-weights models (like Llama 3 or Mistral) within the bank’s own secure cloud environment (VPC). This ensures Data Sovereignty—your internal policies and customer data never leave your firewall, meeting strict RBI data localization norms.

3.4 Phased Implementation Strategy: Domain-Focused Deployment

The Softlabs solution employs a focused-domain approach rather than attempting to model all 244+ RBI Master Directions simultaneously. This strategy balances technical feasibility with rapid ROI delivery.

Figure 6: The Domain-Focused Implementation Strategy

Figure 6: The Domain-Focused Implementation Strategy

Building knowledge graphs for 2-3 regulatory domains (KYC/AML, Digital Lending, Payment Systems) enables Technical Precision. We manage entity ontologies for 20-30 interconnected circulars per domain vs 5,000+ nodes across the entire RBI corpus. This allows domain experts to manually validate entity extraction and relationship mapping, ensuring Verifiable Accuracy.

Furthermore, focusing on high-impact areas like KYC/AML provides Proven ROI. Since KYC violations account for ₹10-50 crore in annual penalties, demonstrating prevention in this specific domain builds a clear business case for expansion.

4. The RBI Circular AI Summarizer Workflow

When implementing this RBI Circular Summarizer chatbot, we position the tool not as “Automated Compliance,” but as a “Compliance Copilot.” It assists officers by reducing research time by 80% and providing explainable reasoning. Below, you can see the system in action.

4.1 Scenario: The “Sudden Notification”

Let’s walk through a real-world scenario. It is Friday evening, 6:00 PM. The RBI issues a notification increasing the risk weight for unsecured consumer credit.

- Friday 6:05 PM: System ingests notification and flags potential impact.

- Friday 6:10 PM: AI generates preliminary analysis highlighting affected product categories (Personal Loans/Credit Cards) with confidence scores.

- Friday 6:30 PM: Compliance officer reviews AI recommendations and validates findings.

- Saturday 10:00 AM: After human verification, alert sent to CRO with AI-assisted impact assessment.

Note: The AI Copilot accelerates analysis, but regulatory decisions require human expert validation per RBI FREE AI Framework requirements.

4.2 Feature Spotlight: Searching & Summarizing

The platform isn’t just for complex queries; it’s also a powerful library. Users can search for specific circulars, use the tool as an RBI circular summary generator, and track amendments. See how the search functionality simplifies discovery below.

4.3 Strict Hallucination Control and Citation

In banking, trust is binary. An AI that makes up facts is a liability. Softlabs implements Strict Grounding with citation. Every sentence generated by the AI includes a deep link to the original PDF page.

Human-in-the-Loop Validation: For high-stakes compliance decisions, the system flags answers requiring expert review based on query complexity and confidence scores. This aligns with RBI’s FREE AI Framework mandating human oversight for material regulatory interpretations, positioning the solution as an expert augmentation tool rather than an autonomous decision-making system.

5. Benefits & ROI of RBI Circular Summarizer

Implementing the RBI Circular AI Summarizer delivers value that transcends simple efficiency. It impacts the risk profile and strategic agility of the institution.

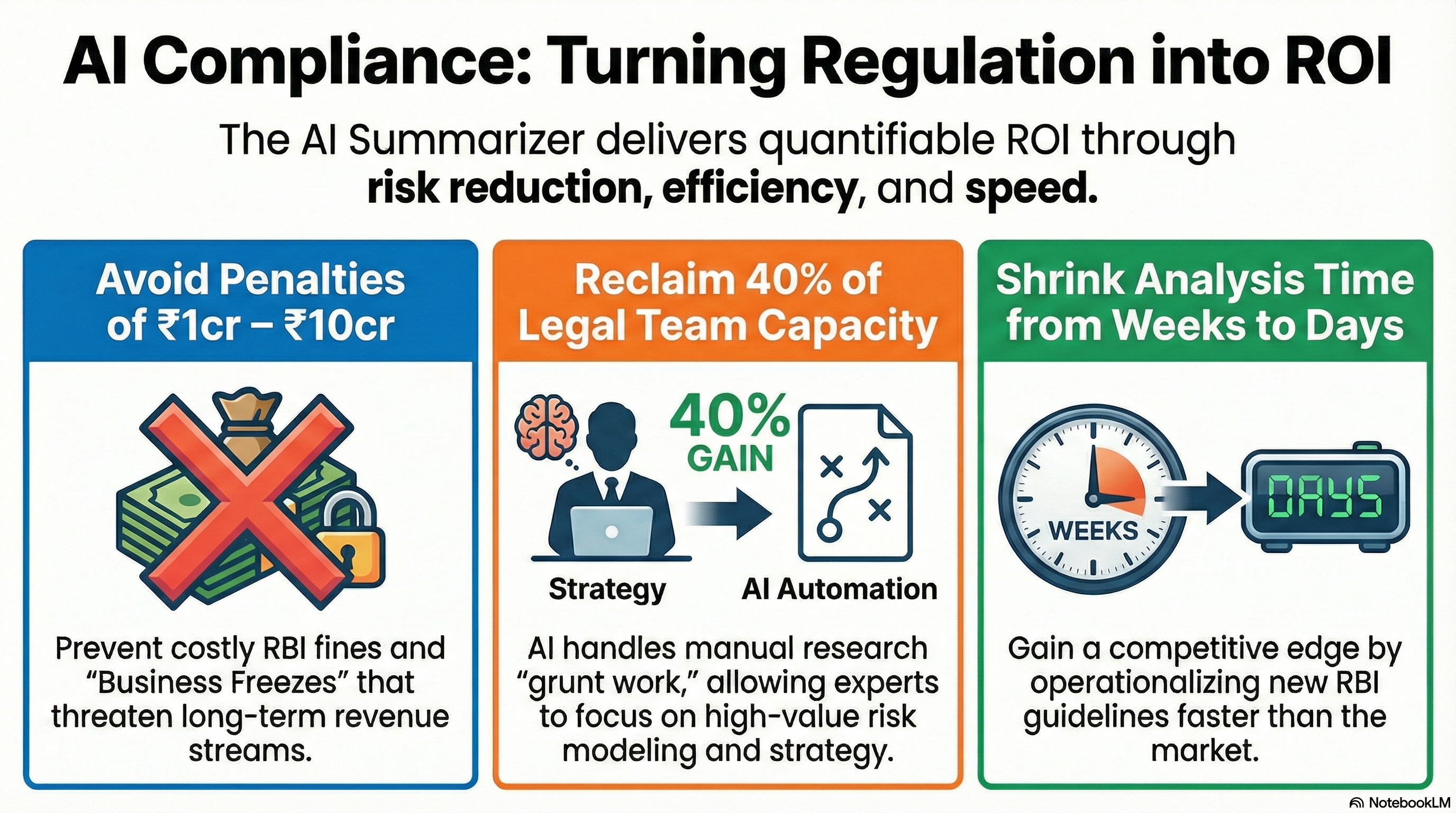

Figure 8: Strategic ROI of AI-Driven Compliance

Figure 8: Strategic ROI of AI-Driven Compliance

5.1 Quantifiable Risk Reduction

The most direct ROI comes from penalty avoidance. Avoiding a single major RBI penalty (which can range from ₹1 crore to ₹10 crore) often covers the cost of the system for several years. Furthermore, by preventing “Business Freezes” (such as embargoes on issuing new credit cards), the AI protects the bank’s license to operate and its long-term revenue streams.

5.2 Operational Efficiency

Manual compliance is labor-intensive. Legal teams spend up to 40% of their time researching regulatory history. This reduces research time significantly, allowing banks to deploy existing experts on high-value tasks like risk modeling and strategy, while the AI for RBI circular analysis handles the “grunt work” of tracking.

5.3 Strategic Agility: Regulatory Time-to-Market

In the Fintech era, speed is a competitive advantage. When the RBI releases new guidelines for a product (e.g., “Pre-Sanctioned Credit Lines on UPI”), the bank that understands and operationalizes these rules first captures the market. This solution helps in reducing regulatory analysis time from weeks to days, enabling faster product compliance assessments while maintaining required legal oversight.

6. Where to Start: Domain Scoping

A common mistake in RegTech is trying to solve everything at once. We recommend a phased approach, organizing compliance by specific domains. This ensures that the system remains accurate and manageable.

6.1 Recommended Domains for Phase 1

- KYC / AML: Highest penalty risk; frequent updates; clear entity types (Customer, ID, Verification). Ideal starting point.

- Digital Lending: Hot regulatory topic in 2025-26; recent rule changes. High business value for retail banking.

- Payment Systems: Rapidly evolving UPI/BNPL regulations. Essential for Fintech agility.

7. Deep Technical Analysis: GraphRAG vs. Vector RAG

To underscore the sophistication of our RBI circular analysis platform, we must delve deeper into the mechanics of GraphRAG versus standard approaches. This is the difference between a system that “guesses” and a system that “knows.”

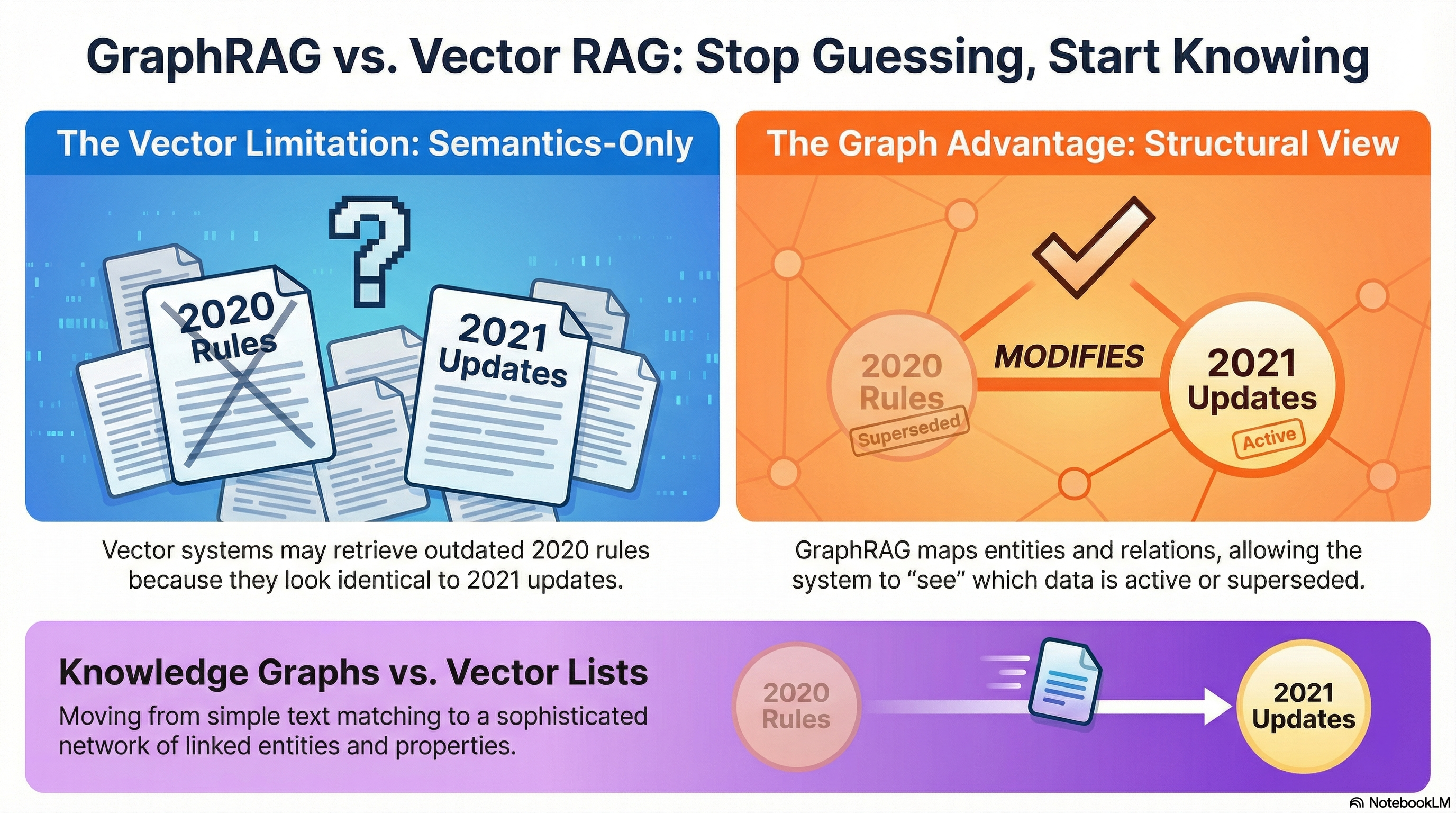

Figure 9: Visualizing the Structural Advantage of GraphRAG

Figure 9: Visualizing the Structural Advantage of GraphRAG

7.1 The Vector Limitation (The “Semantics-Only” View)

In standard RAG, text is converted to vectors.

- Text A (2020): “Limit for contactless transaction is ₹2000.”

- Text B (2021): “Limit for contactless transaction is enhanced to ₹5000.”

- Query: “What is the contactless limit?”

Vectorially, both texts are almost identical. They share the words “Limit,” “contactless,” “transaction.” A vector search might retrieve both, or worse, retrieve the 2020 rule if the query phrasing happens to match it better. The system has no way of knowing that 2021 replaces 2020.

7.2 The Knowledge Graph Advantage (The “Structural” View)

GraphRAG adds a structural layer.

- Entities: Transaction_Limit, ₹2000, ₹5000.

- Relations: Circular_2021 —-> Circular_2020.

- Properties: Circular_2020 has status Superseded.

When the query is processed, the system doesn’t just look for “contactless limit.” It looks for the active value associated with that entity. It traverses the MODIFIES edge, sees that Circular_2020 is inactive, and retrieves only Circular_2021.

8. Feasibility and Validation

8.1 Production Validation: Why This Approach Works

GraphRAG for regulatory compliance is not experimental. Bank of America deploys similar architectures for regulatory intelligence, MasterControl ships knowledge graph solutions for FDA compliance, and German financial institutions use hybrid RAG for AML regulations. This proves that the model works at an enterprise scale.

8.2 Accessible Technology Stack

The solution uses industry-standard tools rather than proprietary FAANG-exclusive technology:

- Neo4j: The world’s leading graph database (used by Fortune 500 companies).

- Open-weight LLMs: (Llama 3, Mistral) deployable in client infrastructure.

- Azure Document Intelligence / AWS Textract: For robust table extraction.

- LangChain/LlamaIndex: Frameworks with built-in GraphRAG support.

8.3 RBI FREE AI Framework Compliance

The architecture inherently supports RBI’s 2025 AI governance requirements through explainable reasoning via graph path visualization, data localization through on-premise/VPC deployment, and human oversight integration for material compliance decisions.

9. Conclusion

This RBI circular GenAI tool represents a strategic evolution in regulatory compliance—transitioning from manual, document-centric workflows to AI-assisted, graph-based intelligence. By focusing initial deployment on high-impact regulatory domains and maintaining human expert oversight, Softlabs Group offers banks a proven path to compliance efficiency while meeting RBI’s AI governance standards.

Recommended Starting Point: Financial institutions should prioritize 2-3 regulatory domains where compliance gaps pose immediate penalty risk (typically KYC/AML, Digital Lending, or Payment Systems). A focused pilot deployment enables verifiable accuracy and clear ROI before scaling.

Schedule Your Strategic Consultation